You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Alrajhi-0 Compressed.5133686765536793Document1 pageAlrajhi-0 Compressed.5133686765536793Abdul-rheeim Q OwiNo ratings yet

- 04 Atlassian 3 Statement Model CompletedDocument18 pages04 Atlassian 3 Statement Model CompletedYusuf RaharjaNo ratings yet

- JOLLIBEEDocument23 pagesJOLLIBEEVia B. Borrez50% (2)

- Hiab Crane Service ManualDocument16 pagesHiab Crane Service Manualjohan useche33% (3)

- 3rd Imitation Jewellery Show 2017Document12 pages3rd Imitation Jewellery Show 2017Charles Binu100% (1)

- Corporate HRD and Skills Development For Employment Scope and Strategies PDFDocument112 pagesCorporate HRD and Skills Development For Employment Scope and Strategies PDFCharles BinuNo ratings yet

- 7th Sugar Asia 2015Document11 pages7th Sugar Asia 2015Charles BinuNo ratings yet

- Framework For Case AnalysisDocument14 pagesFramework For Case AnalysisShruti DesaiNo ratings yet

- AST Job Description-MaterialsManagerDocument3 pagesAST Job Description-MaterialsManagerLaxmi SahaniNo ratings yet

- Fossil Fuels: Coal: HistoryDocument8 pagesFossil Fuels: Coal: HistoryCharles BinuNo ratings yet

- Sbi Associate - Po & Po (Rural Business) Exam Reasoning AbilityDocument40 pagesSbi Associate - Po & Po (Rural Business) Exam Reasoning AbilitymaheshNo ratings yet

- Coal Mining Methods - EMFI SummaryDocument0 pagesCoal Mining Methods - EMFI SummaryCharles BinuNo ratings yet

- Materials Management DepartmentDocument5 pagesMaterials Management DepartmentCharles BinuNo ratings yet

- MasterDocument24 pagesMasterAkshay MathurNo ratings yet

- Spss v19Document97 pagesSpss v19Charles BinuNo ratings yet

- LogisticsDocument6 pagesLogisticsp2atikNo ratings yet

- Peter BlauDocument14 pagesPeter BlauChristian MárquezNo ratings yet

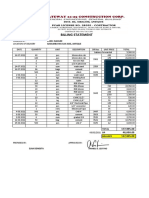

- Billing Statement: Engr. Elizalde Bagumbayan San Jose, AntiqueDocument1 pageBilling Statement: Engr. Elizalde Bagumbayan San Jose, AntiqueMark OlandresNo ratings yet

- PyreX Rebate FormDocument1 pagePyreX Rebate FormkhandegNo ratings yet

- IO Ethanol 2018 enDocument7 pagesIO Ethanol 2018 enPeter PandaNo ratings yet

- Gold in The Investment Portfolio: Frankfurt School - Working PaperDocument50 pagesGold in The Investment Portfolio: Frankfurt School - Working PaperSharvani ChadalawadaNo ratings yet

- Resilience: Healing The FracturesDocument68 pagesResilience: Healing The FracturesMargie OpayNo ratings yet

- Machines SDN BHD Reg. No:200601025413: InvoiceDocument1 pageMachines SDN BHD Reg. No:200601025413: InvoiceReyza FengeNo ratings yet

- Principles of EconomicsDocument20 pagesPrinciples of EconomicsRonald QuintoNo ratings yet

- El Astri CityDocument4 pagesEl Astri CityTipu100% (1)

- PNBMetlife Gauranteed Future PlanDocument4 pagesPNBMetlife Gauranteed Future PlanManager Pnb LucknowNo ratings yet

- Connecting Villages To Power GridDocument3 pagesConnecting Villages To Power GridTRANSCO CLSGNo ratings yet

- 19e Section6 LN Chapter07Document12 pages19e Section6 LN Chapter07benbenchen100% (3)

- FR Garment Processing Fty ListDocument11 pagesFR Garment Processing Fty ListHà TrầnNo ratings yet

- Spa Tleung 112016Document1 pageSpa Tleung 112016Denzel Edward CariagaNo ratings yet

- International Business - UoWL Copy 4Document19 pagesInternational Business - UoWL Copy 4MarianAdragaiNo ratings yet

- BeneficiaryDetailForSocialAuditReport PMAYG 3179001 2022-2023 PDFDocument5 pagesBeneficiaryDetailForSocialAuditReport PMAYG 3179001 2022-2023 PDFAmarchandra PrajapatiNo ratings yet

- En Banc Commissioner OF Internal Revenue, G. R. No. 163653Document12 pagesEn Banc Commissioner OF Internal Revenue, G. R. No. 163653ecinue guirreisaNo ratings yet

- The Simplified Invoice in SpainDocument2 pagesThe Simplified Invoice in SpainArcos & Lamers Asociados, law firm in Spain, accountants in MarbellaNo ratings yet

- Cbse Schools in Maharashtra by ProkeralaDocument56 pagesCbse Schools in Maharashtra by ProkeralaAshwiniNo ratings yet

- Value Added Tax: Commercial MathematicsDocument9 pagesValue Added Tax: Commercial MathematicsMridulNo ratings yet

- Currency OptionsDocument18 pagesCurrency OptionsSiddharth ChauhanNo ratings yet

- Abakada Guro Party-List Et. Al vs. Executive SecretaryDocument2 pagesAbakada Guro Party-List Et. Al vs. Executive SecretaryRaquel Doquenia100% (1)

- Audit Report Lag and The Effectiveness of Audit Committee Among Malaysian Listed CompaniesDocument12 pagesAudit Report Lag and The Effectiveness of Audit Committee Among Malaysian Listed Companiesxaxif8265100% (1)

- Law of Taxation II - Synopsis - Anugrah Joy - 2018003Document3 pagesLaw of Taxation II - Synopsis - Anugrah Joy - 2018003Anugrah JoyNo ratings yet

- JournalDocument3 pagesJournalAnonymous RPGElS100% (1)

- BMC Election Results 2007Document228 pagesBMC Election Results 2007Sudhir Dhoble50% (2)