You might also like

- Estate Tax Rates 2012Document1 pageEstate Tax Rates 2012Tax FoundationNo ratings yet

- A Perfect LifeDocument19 pagesA Perfect LifeAmal ChinthakaNo ratings yet

- Banks ComparisonDocument2 pagesBanks ComparisonZachary Jon EngelNo ratings yet

- 2013 Tax RatesDocument4 pages2013 Tax Ratesapi-241405153No ratings yet

- Pam 61 eDocument1 pagePam 61 eNaga RajNo ratings yet

- Expense BudgetDocument1 pageExpense Budgetapi-218669047No ratings yet

- Income Tax Rates PDFDocument1 pageIncome Tax Rates PDFAditi SharmaNo ratings yet

- Financial AnalysisDocument2 pagesFinancial Analysisvnguyen5651No ratings yet

- Budget Sheet ShareDocument5 pagesBudget Sheet Sharenonsense45No ratings yet

- Tax Audit Limit & Tax RatesDocument6 pagesTax Audit Limit & Tax RatesPhani SankaraNo ratings yet

- Preserve South RussellDocument2 pagesPreserve South RussellStephen J. Latkovic, Esq., CPANo ratings yet

- Eyes Wide Open: The Implications and Opportunities of The Current Tax Reform DebateDocument12 pagesEyes Wide Open: The Implications and Opportunities of The Current Tax Reform DebaterepsandylevinNo ratings yet

- Tax RatesDocument3 pagesTax RatesHaneef ShaikNo ratings yet

- Franchise Fact FileDocument5 pagesFranchise Fact FileJaewon ChoiNo ratings yet

- Oct 15Document1 pageOct 15api-286093121No ratings yet

- WN Interest Rates Tcm428 588513Document4 pagesWN Interest Rates Tcm428 588513firefxyNo ratings yet

- New Hire Benefits Summary: Medical Plan OptionsDocument3 pagesNew Hire Benefits Summary: Medical Plan OptionsRavi Prakash MayreddyNo ratings yet

- Jan 16Document1 pageJan 16api-286093121No ratings yet

- Collection State LawsDocument13 pagesCollection State LawsFreedomofMindNo ratings yet

- My Life in The FutureDocument14 pagesMy Life in The Futureapi-281762512No ratings yet

- Dec 15Document1 pageDec 15api-286093121No ratings yet

- California Cities and County Sales and Use Tax Rates 2012Document23 pagesCalifornia Cities and County Sales and Use Tax Rates 2012L. A. PatersonNo ratings yet

- Paul Simon Public Policy Institute Tax Poll: March 2015Document4 pagesPaul Simon Public Policy Institute Tax Poll: March 2015Reboot IllinoisNo ratings yet

- Canada Tax RatesDocument2 pagesCanada Tax RatesFilip CanoNo ratings yet

- Income Tax Rates For The Past 10 YearsDocument10 pagesIncome Tax Rates For The Past 10 YearsTarang DoshiNo ratings yet

- October, 2012: Propositions 30 & 38 in Context - California Funding For Public SchoolsDocument40 pagesOctober, 2012: Propositions 30 & 38 in Context - California Funding For Public Schoolsk12newsnetworkNo ratings yet

- Welcome PR 5.4Document4 pagesWelcome PR 5.4glasscityjungleNo ratings yet

- Millers' Tax Computati: Known ParametersDocument2 pagesMillers' Tax Computati: Known ParametersYadav_BaeNo ratings yet

- The Cost of BusinessDocument1 pageThe Cost of BusinessDrew HansenNo ratings yet

- Monthly Budget Justine LawrenceDocument6 pagesMonthly Budget Justine Lawrenceapi-277278641No ratings yet

- Denali Individual Dental All Other States - AETNADocument10 pagesDenali Individual Dental All Other States - AETNAJohn BerkowitzNo ratings yet

- Amended Belen Water and Sewer Rates OrdinanceDocument5 pagesAmended Belen Water and Sewer Rates OrdinanceVCNews-BulletinNo ratings yet

- Aetna 2014Document1 pageAetna 2014Vignesh EswaranNo ratings yet

- Zip Code Detailed Profile: Were You Denied A Mortgage?Document32 pagesZip Code Detailed Profile: Were You Denied A Mortgage?ashes_xNo ratings yet

- Surcharge: On Contributi Employee Use Business Proportion - 100% Cost X OperatingDocument4 pagesSurcharge: On Contributi Employee Use Business Proportion - 100% Cost X Operatinglouis_parker_5553No ratings yet

- Senator Heller 2014 Finance ReportDocument8 pagesSenator Heller 2014 Finance ReportLas Vegas Review-JournalNo ratings yet

- Facts and Figures 2012: Sales Tax Treatment of Groceries, Candy and Soda, As of January 1, 2012Document1 pageFacts and Figures 2012: Sales Tax Treatment of Groceries, Candy and Soda, As of January 1, 2012Tax FoundationNo ratings yet

- Budget JulyDocument27 pagesBudget Julyapi-235718346No ratings yet

- Budget 4Document14 pagesBudget 4api-235297320No ratings yet

- Income Tax Slabs 2007-08 To 2010-11Document4 pagesIncome Tax Slabs 2007-08 To 2010-11Manoj ThuthijaNo ratings yet

- Net Proceeds PDFDocument2 pagesNet Proceeds PDFTan Ming KwanNo ratings yet

- 2015 Brackets & Planning Limits (Janney)Document5 pages2015 Brackets & Planning Limits (Janney)John CortapassoNo ratings yet

- Mary Lawrence DisclosureDocument32 pagesMary Lawrence DisclosuredhmontgomeryNo ratings yet

- Annuity CommissionsDocument18 pagesAnnuity CommissionsScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- Determine The Donor's Tax Due On Each DonationDocument1 pageDetermine The Donor's Tax Due On Each DonationRobert Jayson UyNo ratings yet

- Donor'S Tax: BIR Form 1800Document4 pagesDonor'S Tax: BIR Form 1800JAYAR MENDZNo ratings yet

- Income TaxDocument5 pagesIncome TaxAshish NarulaNo ratings yet

- Lesson 14-Budget Planning WorksheetDocument6 pagesLesson 14-Budget Planning Worksheetapi-253889154No ratings yet

- Brokerage Margin Account and Interest Rates - TD AmeritradeDocument10 pagesBrokerage Margin Account and Interest Rates - TD AmeritradeNash Paul PolzlNo ratings yet

- Pay Calc 1Document3 pagesPay Calc 1Gobi ArumugamNo ratings yet

- Metabolic AcidosisDocument16 pagesMetabolic Acidosisloglesb1No ratings yet

- Income Tax Calculator 2013-14Document2 pagesIncome Tax Calculator 2013-14kirang gandhiNo ratings yet

- Budget 090403 Fact FictionDocument2 pagesBudget 090403 Fact FictionAlfonso RobinsonNo ratings yet

- Central New York School Boards Association Annual Legislative BreakfastDocument19 pagesCentral New York School Boards Association Annual Legislative BreakfastTime Warner Cable NewsNo ratings yet

- Income InequalityDocument36 pagesIncome InequalityKate CongerNo ratings yet

- 529credit SS1Document1 page529credit SS1loristurdevantNo ratings yet

- Income Tax Slab For Ay 11Document1 pageIncome Tax Slab For Ay 11mmmukhtarNo ratings yet

- Nov 15Document2 pagesNov 15api-286093121No ratings yet

- A Submission to the Government of Canada on the Subject of Poverty ReductionFrom EverandA Submission to the Government of Canada on the Subject of Poverty ReductionNo ratings yet

- For Single Military Women Only: 10 Easy-Breezy Retirement TipsFrom EverandFor Single Military Women Only: 10 Easy-Breezy Retirement TipsNo ratings yet

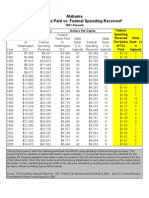

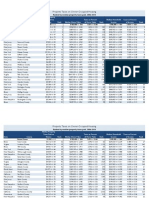

- Federal Taxes Paid Vs Federal Spending Received by States, 1981-2005Document51 pagesFederal Taxes Paid Vs Federal Spending Received by States, 1981-2005Javier Arvelo-Cruz-SantanaNo ratings yet

- Tax Foundation 2014 Annual ReportDocument32 pagesTax Foundation 2014 Annual ReportTax FoundationNo ratings yet

- Christmas Cheer Return: Filing StatusDocument2 pagesChristmas Cheer Return: Filing StatusTax FoundationNo ratings yet

- Facts & Figures 2015: How Does Your State Compare?Document55 pagesFacts & Figures 2015: How Does Your State Compare?Tax FoundationNo ratings yet

- Explainer: Nevada Governor Sandoval's Business License Fee Restructuring - Appendix ADocument10 pagesExplainer: Nevada Governor Sandoval's Business License Fee Restructuring - Appendix ATax FoundationNo ratings yet

- Facts and Figures - How Does Your State Compare? 2013 EditionDocument56 pagesFacts and Figures - How Does Your State Compare? 2013 EditionTax FoundationNo ratings yet

- Facts and Figures 2014Document55 pagesFacts and Figures 2014Tax FoundationNo ratings yet

- Facts and Figures 2013Document56 pagesFacts and Figures 2013Tax FoundationNo ratings yet

- Fed U.S. Federal Individual Income Tax Rates History, 1862-2013Document68 pagesFed U.S. Federal Individual Income Tax Rates History, 1862-2013Tax Foundation96% (23)

- How Is The Money Used? Federal and State Cases Distinguishing Taxes and FeesDocument98 pagesHow Is The Money Used? Federal and State Cases Distinguishing Taxes and FeesTax FoundationNo ratings yet

- Federal Individual Individual Income Tax Rate, Adjusted For InflationDocument66 pagesFederal Individual Individual Income Tax Rate, Adjusted For InflationTax Foundation100% (4)

- Tax Watch, Winter 2013Document28 pagesTax Watch, Winter 2013Tax FoundationNo ratings yet

- Powerpoint Presentation For "North Carolina Tax Reform Options: A Guide To Fair, Simple, Pro-Growth Reform"Document38 pagesPowerpoint Presentation For "North Carolina Tax Reform Options: A Guide To Fair, Simple, Pro-Growth Reform"Tax FoundationNo ratings yet

- Tax Watch Summer 2012Document24 pagesTax Watch Summer 2012Tax FoundationNo ratings yet

- Federal Income Tax Rates History, Nominal Dollars, 1913-2013Document66 pagesFederal Income Tax Rates History, Nominal Dollars, 1913-2013Tax Foundation100% (1)

- Fiscal Cliff MSA TableDocument11 pagesFiscal Cliff MSA TableTax FoundationNo ratings yet

- North Carolina Tax Reform Options: A Guide To Fair, Simple, Pro-Growth ReformDocument84 pagesNorth Carolina Tax Reform Options: A Guide To Fair, Simple, Pro-Growth ReformTax Foundation100% (1)

- Fiscal Cliff MSA TableDocument11 pagesFiscal Cliff MSA TableTax FoundationNo ratings yet

- Federal Individual Individual Income Tax Rate, Adjusted For InflationDocument66 pagesFederal Individual Individual Income Tax Rate, Adjusted For InflationTax Foundation100% (4)

- Scott Hodge, President Will Mcbride, Chief EconomistDocument20 pagesScott Hodge, President Will Mcbride, Chief EconomistTax FoundationNo ratings yet

- Proptax 08 10 TaxespaidDocument67 pagesProptax 08 10 TaxespaidTax FoundationNo ratings yet

- Proptax10 Taxes PaidDocument27 pagesProptax10 Taxes PaidTax FoundationNo ratings yet

- Property Taxes On Owner-Occupied HousingDocument28 pagesProperty Taxes On Owner-Occupied HousingTax FoundationNo ratings yet

- Proptax10 Home ValueDocument28 pagesProptax10 Home ValueTax FoundationNo ratings yet

- Proptax 06 10 IncomeDocument102 pagesProptax 06 10 IncomeTax FoundationNo ratings yet

- Proptax 06 10 TaxpaidDocument102 pagesProptax 06 10 TaxpaidTax FoundationNo ratings yet

- Proptax 08 10 IncomeDocument66 pagesProptax 08 10 IncomeTax FoundationNo ratings yet

- Proptax 06 10 HomevalueDocument102 pagesProptax 06 10 HomevalueTax FoundationNo ratings yet