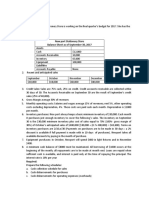

SHOP - The Credit Card You Pick Can Save You Money

SHOP - The Credit Card You Pick Can Save You Money

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Pre-Week Auditing Problems 2014Document41 pagesPre-Week Auditing Problems 2014Pat Closa80% (15)

- Joy Pathak - Credit SpreadsDocument21 pagesJoy Pathak - Credit Spreadspathak5100% (1)

- Legal Ethics.1Document139 pagesLegal Ethics.1Jesse RazonNo ratings yet

- Demonetization: Impact On Cashless Payemnt System: Manpreet KaurDocument6 pagesDemonetization: Impact On Cashless Payemnt System: Manpreet KaurKiran SoniNo ratings yet

- LN10Moffett38115 04 FMF LN10Document77 pagesLN10Moffett38115 04 FMF LN10Kwichobela BonaventureNo ratings yet

- 2020 W Island AveDocument42 pages2020 W Island Aveassistant_sccNo ratings yet

- Section 1 30 Minutes (20 Questions) : Gmat Math Problem SolvingDocument23 pagesSection 1 30 Minutes (20 Questions) : Gmat Math Problem Solvingajju1378No ratings yet

- NFPE MAVELIKARA POSTAL DIVISION - Twenty Useful Question Related With Leave - Study Material For Various Department ExaminationDocument8 pagesNFPE MAVELIKARA POSTAL DIVISION - Twenty Useful Question Related With Leave - Study Material For Various Department ExaminationVinay TyagiNo ratings yet

- Principles of Accounts 11Document47 pagesPrinciples of Accounts 11Godfrey LwandoNo ratings yet

- Yield Pledge Checking: Account Opening & UsageDocument2 pagesYield Pledge Checking: Account Opening & Usageshenzo_No ratings yet

- Ocm Distingwish BetweenDocument13 pagesOcm Distingwish BetweenRamnarayan DarakNo ratings yet

- Final Format For Credit MidtermDocument8 pagesFinal Format For Credit MidtermCloieRjNo ratings yet

- Sale and Agreement To SellDocument26 pagesSale and Agreement To SellTejas DesaiNo ratings yet

- NCC Bank ReportDocument65 pagesNCC Bank Reportইফতি ইসলামNo ratings yet

- Budget Practice QuestionsDocument8 pagesBudget Practice Questionsmohammad bilalNo ratings yet

- Allied Banking Corporation v. CIR (Exception To Requisite of Filing An Admin Protest Before Appeal To CTA)Document11 pagesAllied Banking Corporation v. CIR (Exception To Requisite of Filing An Admin Protest Before Appeal To CTA)kjhenyo218502No ratings yet

- PledgeDocument9 pagesPledgeLaarni AragonNo ratings yet

- 2012 Syllabus 11 AccountancyDocument4 pages2012 Syllabus 11 AccountancyYadira TerryNo ratings yet

- Chapter 4 and 5Document19 pagesChapter 4 and 5nyasha praise mafungaNo ratings yet

- Working Capital Estimation - Operating Cycle Method - EFinanceManagementDocument2 pagesWorking Capital Estimation - Operating Cycle Method - EFinanceManagementJuanCarlosRNo ratings yet

- Bank Interview QuestionsDocument2 pagesBank Interview QuestionsShathish GunasekaranNo ratings yet

- Askari Bank ProjectDocument32 pagesAskari Bank ProjectKhurshid MarwatNo ratings yet

- Budget Problem For Modular Group-1Document2 pagesBudget Problem For Modular Group-1Mohammed Saber Ibrahim Ramadan ITL World KSA0% (1)

- Chile: Negotiated M&A GuideDocument25 pagesChile: Negotiated M&A GuideMikailOpintoNo ratings yet

- L&T Long Term Infrastructure Bond Tranche 1 Application FormDocument8 pagesL&T Long Term Infrastructure Bond Tranche 1 Application FormPrajna CapitalNo ratings yet

- Credit DigestDocument1 pageCredit DigestBreth1979No ratings yet

- HVAT Reply No 2 To Emaar-MGFDocument3 pagesHVAT Reply No 2 To Emaar-MGFTejinderSingh159No ratings yet

- A Proposal For Partial Credit Guarantee Scheme in ComesaDocument19 pagesA Proposal For Partial Credit Guarantee Scheme in Comesacomesa cmiNo ratings yet

- What Are The Different Types of DebenturesDocument2 pagesWhat Are The Different Types of DebenturesUsman NadeemNo ratings yet

- Chapter 2 FranchisingDocument47 pagesChapter 2 FranchisingAtiQah NOtyhNo ratings yet

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Pre-Week Auditing Problems 2014Document41 pagesPre-Week Auditing Problems 2014Pat Closa80% (15)

- Joy Pathak - Credit SpreadsDocument21 pagesJoy Pathak - Credit Spreadspathak5100% (1)

- Legal Ethics.1Document139 pagesLegal Ethics.1Jesse RazonNo ratings yet

- Demonetization: Impact On Cashless Payemnt System: Manpreet KaurDocument6 pagesDemonetization: Impact On Cashless Payemnt System: Manpreet KaurKiran SoniNo ratings yet

- LN10Moffett38115 04 FMF LN10Document77 pagesLN10Moffett38115 04 FMF LN10Kwichobela BonaventureNo ratings yet

- 2020 W Island AveDocument42 pages2020 W Island Aveassistant_sccNo ratings yet

- Section 1 30 Minutes (20 Questions) : Gmat Math Problem SolvingDocument23 pagesSection 1 30 Minutes (20 Questions) : Gmat Math Problem Solvingajju1378No ratings yet

- NFPE MAVELIKARA POSTAL DIVISION - Twenty Useful Question Related With Leave - Study Material For Various Department ExaminationDocument8 pagesNFPE MAVELIKARA POSTAL DIVISION - Twenty Useful Question Related With Leave - Study Material For Various Department ExaminationVinay TyagiNo ratings yet

- Principles of Accounts 11Document47 pagesPrinciples of Accounts 11Godfrey LwandoNo ratings yet

- Yield Pledge Checking: Account Opening & UsageDocument2 pagesYield Pledge Checking: Account Opening & Usageshenzo_No ratings yet

- Ocm Distingwish BetweenDocument13 pagesOcm Distingwish BetweenRamnarayan DarakNo ratings yet

- Final Format For Credit MidtermDocument8 pagesFinal Format For Credit MidtermCloieRjNo ratings yet

- Sale and Agreement To SellDocument26 pagesSale and Agreement To SellTejas DesaiNo ratings yet

- NCC Bank ReportDocument65 pagesNCC Bank Reportইফতি ইসলামNo ratings yet

- Budget Practice QuestionsDocument8 pagesBudget Practice Questionsmohammad bilalNo ratings yet

- Allied Banking Corporation v. CIR (Exception To Requisite of Filing An Admin Protest Before Appeal To CTA)Document11 pagesAllied Banking Corporation v. CIR (Exception To Requisite of Filing An Admin Protest Before Appeal To CTA)kjhenyo218502No ratings yet

- PledgeDocument9 pagesPledgeLaarni AragonNo ratings yet

- 2012 Syllabus 11 AccountancyDocument4 pages2012 Syllabus 11 AccountancyYadira TerryNo ratings yet

- Chapter 4 and 5Document19 pagesChapter 4 and 5nyasha praise mafungaNo ratings yet

- Working Capital Estimation - Operating Cycle Method - EFinanceManagementDocument2 pagesWorking Capital Estimation - Operating Cycle Method - EFinanceManagementJuanCarlosRNo ratings yet

- Bank Interview QuestionsDocument2 pagesBank Interview QuestionsShathish GunasekaranNo ratings yet

- Askari Bank ProjectDocument32 pagesAskari Bank ProjectKhurshid MarwatNo ratings yet

- Budget Problem For Modular Group-1Document2 pagesBudget Problem For Modular Group-1Mohammed Saber Ibrahim Ramadan ITL World KSA0% (1)

- Chile: Negotiated M&A GuideDocument25 pagesChile: Negotiated M&A GuideMikailOpintoNo ratings yet

- L&T Long Term Infrastructure Bond Tranche 1 Application FormDocument8 pagesL&T Long Term Infrastructure Bond Tranche 1 Application FormPrajna CapitalNo ratings yet

- Credit DigestDocument1 pageCredit DigestBreth1979No ratings yet

- HVAT Reply No 2 To Emaar-MGFDocument3 pagesHVAT Reply No 2 To Emaar-MGFTejinderSingh159No ratings yet

- A Proposal For Partial Credit Guarantee Scheme in ComesaDocument19 pagesA Proposal For Partial Credit Guarantee Scheme in Comesacomesa cmiNo ratings yet

- What Are The Different Types of DebenturesDocument2 pagesWhat Are The Different Types of DebenturesUsman NadeemNo ratings yet

- Chapter 2 FranchisingDocument47 pagesChapter 2 FranchisingAtiQah NOtyhNo ratings yet