You might also like

- Hedge Fund StrategiesDocument3 pagesHedge Fund StrategiesJack Jacinto100% (1)

- Private Equity Cheat Sheet Bloomberg TerminalDocument1 pagePrivate Equity Cheat Sheet Bloomberg TerminalAmuyGnopNo ratings yet

- Hedge Fund Book V3Document197 pagesHedge Fund Book V3http://besthedgefund.blogspot.comNo ratings yet

- An Introduction To DTCC: Guide To Clearance & SettlementDocument36 pagesAn Introduction To DTCC: Guide To Clearance & Settlementmona2009pooja100% (3)

- Some Considerations in Setting Up A Hedge Fund - Client Introductory ArticleDocument26 pagesSome Considerations in Setting Up A Hedge Fund - Client Introductory ArticleDistressedDebtInvest100% (1)

- Kinder Morgan Summary AnalysisDocument2 pagesKinder Morgan Summary Analysisenergyanalyst100% (2)

- Securitization of Financial AssetsDocument14 pagesSecuritization of Financial AssetsHarpott Ghanta100% (2)

- Hedge Fund StructreDocument23 pagesHedge Fund Structrejos22231100% (2)

- Asset Securitisation..Document20 pagesAsset Securitisation..raj sharmaNo ratings yet

- (Cayman) Guide To Hedge Funds in The Cayman IslandsDocument29 pages(Cayman) Guide To Hedge Funds in The Cayman IslandsAlinRoscaNo ratings yet

- Mortgage Backed SecuritiesDocument40 pagesMortgage Backed Securitiesyohanmatale100% (2)

- Starting A Hedge FundDocument7 pagesStarting A Hedge FundTrey 'Sha' ChaversNo ratings yet

- Book-Keeping and Accounts Level 2 April 2012Document22 pagesBook-Keeping and Accounts Level 2 April 2012Cary LeeNo ratings yet

- The Oxford Handbook of Private EquityDocument769 pagesThe Oxford Handbook of Private EquityColin Daniel100% (9)

- SecuritizationDocument17 pagesSecuritizationkhus1985No ratings yet

- SecuritizationDocument146 pagesSecuritizationSaurabh ParasharNo ratings yet

- Mortgage Backed Securities PrimerDocument9 pagesMortgage Backed Securities Primerjohnsang50% (2)

- Secondary MarketDocument27 pagesSecondary MarketAmit BharwadNo ratings yet

- Private Equity Part 1Document5 pagesPrivate Equity Part 1Paolina NikolovaNo ratings yet

- Leixner (1999) Securitization of Financial Assets - An IntroductionDocument8 pagesLeixner (1999) Securitization of Financial Assets - An Introductionapi-3778585No ratings yet

- 10 Equity SecuritiesDocument25 pages10 Equity SecuritiesAmir AfzalNo ratings yet

- Corporate Bond Underwriting ProcessDocument27 pagesCorporate Bond Underwriting ProcessRich100% (2)

- Private Equity FundDocument19 pagesPrivate Equity FundClint AyersNo ratings yet

- Securitization of Life InsuranceDocument59 pagesSecuritization of Life Insurancemiroslav.visic8307100% (1)

- Lecture 2 Financial System and InstrumentsDocument44 pagesLecture 2 Financial System and InstrumentsLuisLoNo ratings yet

- CFA Level 1 FundamentalsDocument5 pagesCFA Level 1 Fundamentalskazimeister1No ratings yet

- LeveragedLoan PrimerDocument38 pagesLeveragedLoan PrimerMichael AlguNo ratings yet

- Loan SyndicationDocument4 pagesLoan SyndicationRalsha DinoopNo ratings yet

- An Introduction To Hedge Fund StrategiesDocument44 pagesAn Introduction To Hedge Fund StrategiesAdnan Perwaiz0% (1)

- SIE Learning Guide v08Document153 pagesSIE Learning Guide v08Angelo ImmacolatoNo ratings yet

- Mortgage and Asset Backed Securities Litigation HandbookDocument17 pagesMortgage and Asset Backed Securities Litigation HandbookDeontos100% (1)

- Bond BasicsDocument30 pagesBond Basicsravishankar1972No ratings yet

- Introduction To Collateralized Debt Obligations: Tavakoli Structured Finance, IncDocument6 pagesIntroduction To Collateralized Debt Obligations: Tavakoli Structured Finance, IncShanza ChNo ratings yet

- Model Guide To Securitisation Techniques: Slaughter and MayDocument42 pagesModel Guide To Securitisation Techniques: Slaughter and May111No ratings yet

- Debt InstrumentDocument5 pagesDebt InstrumentDhaval JoshiNo ratings yet

- Bonds: Types, Trading & SettlementDocument52 pagesBonds: Types, Trading & SettlementraviNo ratings yet

- Investment Fund Leagle DocumentsDocument6 pagesInvestment Fund Leagle Documentspradeebha100% (1)

- Quick FactsDocument30 pagesQuick FactsWilliam James100% (2)

- Asset-Backed Commercial PaperDocument4 pagesAsset-Backed Commercial PaperdescataNo ratings yet

- Asset Swaps: Not For Onward DistributionDocument23 pagesAsset Swaps: Not For Onward Distributionjohan oldmanNo ratings yet

- Private Revolving SecuritisationsDocument10 pagesPrivate Revolving SecuritisationsDavid CartellaNo ratings yet

- Insider Investment GuideDocument273 pagesInsider Investment GuideFhélixAbel LoyaNo ratings yet

- Securitization of DebtDocument52 pagesSecuritization of Debtnjsnghl100% (1)

- Securities Lending Times Issue 237Document66 pagesSecurities Lending Times Issue 237Securities Lending TimesNo ratings yet

- Securitization For DummiesDocument5 pagesSecuritization For DummiesHarpott GhantaNo ratings yet

- A Special Purpose EntityDocument3 pagesA Special Purpose Entitynayem_85No ratings yet

- Syndicated Loan MarketDocument56 pagesSyndicated Loan MarketYolanda Glover100% (1)

- Depository SystemDocument38 pagesDepository SystemTarun SehgalNo ratings yet

- Curacao FoundationsDocument32 pagesCuracao Foundationsreuvek6957No ratings yet

- SecuritizationDocument12 pagesSecuritizationNit VictorNo ratings yet

- SecuritizationDocument34 pagesSecuritizationshubh duggalNo ratings yet

- Asset Backed Securitization in BangladeshDocument22 pagesAsset Backed Securitization in BangladeshA_D_I_BNo ratings yet

- Asset-backed Securitization and the Financial Crisis: The Product and Market Functions of Asset-backed Securitization: Retrospect and ProspectFrom EverandAsset-backed Securitization and the Financial Crisis: The Product and Market Functions of Asset-backed Securitization: Retrospect and ProspectNo ratings yet

- Debentures and BondsDocument13 pagesDebentures and BondsLakhan KodiyatarNo ratings yet

- OP Hedge FundDocument278 pagesOP Hedge FundCheeseong LimNo ratings yet

- ABCs of ABCP, 2009Document42 pagesABCs of ABCP, 2009ed_nycNo ratings yet

- A Primer On Whole Business SecuritizationDocument13 pagesA Primer On Whole Business SecuritizationSam TickerNo ratings yet

- Interview Constance BrownDocument7 pagesInterview Constance Brownmarnevivek50% (2)

- Wooden Furniture ManufacturingDocument27 pagesWooden Furniture ManufacturingOsmanMehmood100% (1)

- Balance Sheet OptimizationDocument32 pagesBalance Sheet OptimizationImranullah KhanNo ratings yet

- Primer On Securitization 2019Document36 pagesPrimer On Securitization 2019Anonymous tgYyno0w6No ratings yet

- Investment Analysis and Portfolio ManagementDocument53 pagesInvestment Analysis and Portfolio Managementjoydippagla33% (3)

- Comparative Study of Brokerage Plans of Religare Securities Ltd. With Various Brokerage Firms-1Document83 pagesComparative Study of Brokerage Plans of Religare Securities Ltd. With Various Brokerage Firms-1vibhatiwari31No ratings yet

- Debt InstrumentsDocument14 pagesDebt InstrumentsAnubhav GoelNo ratings yet

- Introduction To Investment BankingDocument45 pagesIntroduction To Investment BankingNgọc Phan Thị BíchNo ratings yet

- CH 22Document12 pagesCH 22williamnyxNo ratings yet

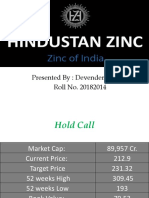

- Hindustan ZincDocument8 pagesHindustan ZincDevender SharmaNo ratings yet

- Translation ExposureDocument12 pagesTranslation Exposureirfan7867809No ratings yet

- An Extensive Exploration of Theories of Foreign Direct InvestmentDocument7 pagesAn Extensive Exploration of Theories of Foreign Direct InvestmentAnonymous 30DS0WzNo ratings yet

- How To Read A Balance SheetDocument17 pagesHow To Read A Balance Sheetismun nadhifahNo ratings yet

- 01 - Preweek Lecture and ProblemsDocument15 pages01 - Preweek Lecture and ProblemsMelody GumbaNo ratings yet

- Cpar - Ap 09.15.13Document18 pagesCpar - Ap 09.15.13KamilleNo ratings yet

- Drillers and Dealers June 2012Document47 pagesDrillers and Dealers June 2012ross_s_campbellNo ratings yet

- Research Project ReportDocument59 pagesResearch Project ReportChitraNandolaNo ratings yet

- Capm 2004 ADocument35 pagesCapm 2004 Aobaidsimon123No ratings yet

- Session 2 VisionDocument34 pagesSession 2 VisionAftab HossainNo ratings yet

- Touradji Capital v. Gentry Beach and Robert VolleroDocument55 pagesTouradji Capital v. Gentry Beach and Robert Vollerobess6159No ratings yet

- FPI-Financial Performance IndicatorsDocument11 pagesFPI-Financial Performance IndicatorselizasavNo ratings yet

- La Programación Completa Del "Mini Davos"Document19 pagesLa Programación Completa Del "Mini Davos"Cronista.com0% (1)

- LKAS 21 - The Effects of Changes in Foreign Exchange Rates - 1496306302 - LKAS 21 - The Effects of Changes in Foreign Exchange Rates PDFDocument20 pagesLKAS 21 - The Effects of Changes in Foreign Exchange Rates - 1496306302 - LKAS 21 - The Effects of Changes in Foreign Exchange Rates PDFAudithya KahawattaNo ratings yet

- ADM 2350A Formula SheetDocument12 pagesADM 2350A Formula SheetJoeNo ratings yet

- Liquidation of A Partnership: Ace Company Balance Sheet April 15, 2003 Assets Liabilities and Partners' EquityDocument4 pagesLiquidation of A Partnership: Ace Company Balance Sheet April 15, 2003 Assets Liabilities and Partners' EquityMohammad UmairNo ratings yet

- Icfai P.A. IiDocument11 pagesIcfai P.A. Iiapi-3757629No ratings yet

- C6 Lecture NotesDocument2 pagesC6 Lecture NotesJonathan NavalloNo ratings yet

- Kpi Dashboard TemplateDocument15 pagesKpi Dashboard TemplatesarahNo ratings yet

- Topic 2 - Business CombinationsDocument32 pagesTopic 2 - Business Combinationshayat_illusionNo ratings yet

- CIBC: Demographics and SMEsDocument3 pagesCIBC: Demographics and SMEsEquicapita Income TrustNo ratings yet

- 1 182Document182 pages1 182Allison SnipesNo ratings yet