You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- 12 and 16v92 Ta Spec SheetDocument4 pages12 and 16v92 Ta Spec SheetBrandon Atz67% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- TextbookIBCurrent (Good Book)Document226 pagesTextbookIBCurrent (Good Book)Tanmay KaperNo ratings yet

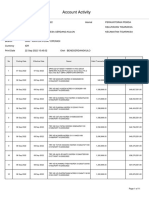

- Account ActivityDocument11 pagesAccount ActivityIrone Akatshuki LeaderNo ratings yet

- IntubationDocument4 pagesIntubationΚατερίνα ΣιάλουNo ratings yet

- Nickdj - Co.Uk: Technicolor Tg588V V2 - Manual ConfigurationDocument5 pagesNickdj - Co.Uk: Technicolor Tg588V V2 - Manual ConfigurationSKNo ratings yet

- Answer: Philippine National Police National Capital Region Police OfficeDocument3 pagesAnswer: Philippine National Police National Capital Region Police OfficeReginaldo Bucu100% (1)

- Compound Interest CalculationDocument2 pagesCompound Interest Calculationbilalak1990No ratings yet

- SP184 - 00A Electrical FeaturesDocument21 pagesSP184 - 00A Electrical FeaturesN'GUESSANNo ratings yet

- Consumer Behavior and Electronic CommerceDocument33 pagesConsumer Behavior and Electronic Commerceasma246No ratings yet

- Data Sheet: PNP Darlington TransistorDocument7 pagesData Sheet: PNP Darlington TransistorJose Norton DoriaNo ratings yet

- MadTech - A Revolution Between Martech and AdtechDocument7 pagesMadTech - A Revolution Between Martech and AdtechDigitalkites OfficialNo ratings yet

- HX DimensionsDocument1 pageHX DimensionsMarquinho LsNo ratings yet

- PAE 3 LectureDocument5 pagesPAE 3 LectureVenice FranciscoNo ratings yet

- Modeling LerengDocument1 pageModeling LerengdyingasNo ratings yet

- Installing Electrical Protection: Electrical Installation and Maintenance Grade 12Document54 pagesInstalling Electrical Protection: Electrical Installation and Maintenance Grade 12Jabie M100% (1)

- BR 14 01 ENG Fusion4 MSC L BrochureDocument8 pagesBR 14 01 ENG Fusion4 MSC L BrochureJavier Alejandro QuingaNo ratings yet

- ISO Management SystemsDocument31 pagesISO Management SystemsLucianMateescu100% (1)

- E22-400M22S Usermanual EN v1.4-3Document13 pagesE22-400M22S Usermanual EN v1.4-3bahaNo ratings yet

- Islam & Capitalism: Dr. Muhammad Hamid UllahDocument27 pagesIslam & Capitalism: Dr. Muhammad Hamid UllahMayankSehgalNo ratings yet

- San Miguel Properties Phils Inc Vs HuangDocument2 pagesSan Miguel Properties Phils Inc Vs Huang000012No ratings yet

- Veenus Medi Lab Panadura - BC 10Document7 pagesVeenus Medi Lab Panadura - BC 10Nirmani HansiniNo ratings yet

- Erf FormDocument2 pagesErf Formmark primo m. sisonNo ratings yet

- Organizational Behaviour by DR Janmejay Senapati 09a447Document853 pagesOrganizational Behaviour by DR Janmejay Senapati 09a447deepaksinghalNo ratings yet

- Ergese of EthiopiaDocument62 pagesErgese of Ethiopiasamuel petrosNo ratings yet

- Comprag - Catalog Compressed Air PreparationDocument24 pagesComprag - Catalog Compressed Air PreparationaferreiraeoliveirabarcelosNo ratings yet

- IBO 3 - 10yearsDocument28 pagesIBO 3 - 10yearsManuNo ratings yet

- 950400man Download-Instructions 14087revaDocument8 pages950400man Download-Instructions 14087revaRenato SilvaNo ratings yet

- Title of Project: Envr 504 Research Project ProposalDocument3 pagesTitle of Project: Envr 504 Research Project ProposalMisha HaroonNo ratings yet

- JPT 2018-08Document92 pagesJPT 2018-08NadirNo ratings yet

- Twin Vs SingleDocument7 pagesTwin Vs SingleDoug GouldNo ratings yet