You might also like

- MBA 2010 Legal Issues Conference: Regulatory Panel 1: Deep-Dive Challenges Presented by The New RESPA RuleDocument53 pagesMBA 2010 Legal Issues Conference: Regulatory Panel 1: Deep-Dive Challenges Presented by The New RESPA RuleCairo AnubissNo ratings yet

- Truth in Lending Act 101: By: Suzanne Garwood Venable 202-344-8046Document28 pagesTruth in Lending Act 101: By: Suzanne Garwood Venable 202-344-8046Cairo AnubissNo ratings yet

- FHA, RESPA and Know Before You Owe: Background and Recent DevelopmentsDocument39 pagesFHA, RESPA and Know Before You Owe: Background and Recent DevelopmentsCairo AnubissNo ratings yet

- Mba L I R C: Egal Ssues and Egulatory OmplianceDocument39 pagesMba L I R C: Egal Ssues and Egulatory OmplianceCairo AnubissNo ratings yet

- COVID19 Impact On ConstructionDocument83 pagesCOVID19 Impact On ConstructionVEERKUMAR GNDECNo ratings yet

- Loan Modifications - Workout Plans and ModificationDocument43 pagesLoan Modifications - Workout Plans and ModificationSudershan ThaibaNo ratings yet

- Bulletin: NUMBER: 2012-27 TO: Freddie Mac Servicers SubjectsDocument5 pagesBulletin: NUMBER: 2012-27 TO: Freddie Mac Servicers SubjectsDinSFLANo ratings yet

- Claims Against Industry Partners and Other Players: Litigation Session Forum Session 3Document33 pagesClaims Against Industry Partners and Other Players: Litigation Session Forum Session 3Cairo AnubissNo ratings yet

- MBA Regulatory Compliance Conference Renaissance Washington DC Downtown Hotel Washington, D.C. September 25, 2011 Workshop 2: Quick Guide To TilaDocument56 pagesMBA Regulatory Compliance Conference Renaissance Washington DC Downtown Hotel Washington, D.C. September 25, 2011 Workshop 2: Quick Guide To TilaCairo AnubissNo ratings yet

- Truth in Lending Act For Mortgage Lending: Presented April 8, 2010 Marjorie A. Corwin, EsquireDocument80 pagesTruth in Lending Act For Mortgage Lending: Presented April 8, 2010 Marjorie A. Corwin, EsquiremzieloNo ratings yet

- CHARGESDocument60 pagesCHARGESW. Kevin MichukiNo ratings yet

- Trusts Act 2019 - InformationDocument10 pagesTrusts Act 2019 - InformationGibson SheatNo ratings yet

- R.A._3765_Truth_in_Lending_Act_.pdfDocument5 pagesR.A._3765_Truth_in_Lending_Act_.pdfsunthatburns00No ratings yet

- H LoanDocument136 pagesH LoanElango PaulchamyNo ratings yet

- Fundamentals of Bookkeeping: Ucpb Savings Bank Operations DivisionDocument71 pagesFundamentals of Bookkeeping: Ucpb Savings Bank Operations DivisionJames ToNo ratings yet

- New Guidelines - Collateral RegistryDocument10 pagesNew Guidelines - Collateral RegistryAkwasiOsseiNkrumahNo ratings yet

- Federal Developments in Loan Originator CompensationDocument15 pagesFederal Developments in Loan Originator CompensationCairo AnubissNo ratings yet

- Presentation Implications Federal Right of Rescission PDFDocument40 pagesPresentation Implications Federal Right of Rescission PDFBleak NarrativesNo ratings yet

- SBA Updates Lending SOPDocument5 pagesSBA Updates Lending SOPFierDaus MfmmNo ratings yet

- Day2 Sp3 1 ICGFMJaneRidleyMay2014 enDocument21 pagesDay2 Sp3 1 ICGFMJaneRidleyMay2014 enInternational Consortium on Governmental Financial ManagementNo ratings yet

- City of Miami: Small Business Emergency Loan ProgramDocument5 pagesCity of Miami: Small Business Emergency Loan Programal_crespoNo ratings yet

- WITS Presentation - Avitha Nofal 11 November 2021Document29 pagesWITS Presentation - Avitha Nofal 11 November 2021aviNo ratings yet

- Accounting Standards SummaryDocument6 pagesAccounting Standards SummarychawlasrishtiNo ratings yet

- Northwood/Pleasant City Community Redevelopment AgencyDocument8 pagesNorthwood/Pleasant City Community Redevelopment Agencyjerricc8100% (2)

- Workshop On Mergers & Acquisitions: Mohit SarafDocument46 pagesWorkshop On Mergers & Acquisitions: Mohit SarafvarunneedsNo ratings yet

- Ch13IFRS 8e PP SlidesDocument82 pagesCh13IFRS 8e PP SlidesMariem AzzabiNo ratings yet

- Latham and Watkins - Tender Offers - October 2015Document24 pagesLatham and Watkins - Tender Offers - October 2015KarenNo ratings yet

- The Safe Mortgage Loan Originator National Exam Study Guide Second Edition 2nd Edition Ebook PDFDocument62 pagesThe Safe Mortgage Loan Originator National Exam Study Guide Second Edition 2nd Edition Ebook PDFalec.black13997% (32)

- LMI GuideDocument31 pagesLMI GuideSamir ChitkaraNo ratings yet

- Audit Consideration - Construction & Real StateDocument6 pagesAudit Consideration - Construction & Real StateAngelica BuenaventuraNo ratings yet

- How To Cancel A MortgageDocument23 pagesHow To Cancel A MortgageCairo Anubiss100% (1)

- ASU REA 411 - Recording and Title InsuranceDocument18 pagesASU REA 411 - Recording and Title InsuranceChih-Wei YangNo ratings yet

- Surety Bond Basics PresentationDocument23 pagesSurety Bond Basics PresentationGrant W DavisNo ratings yet

- Financial Guarantees: Department of Development and Environmental Services (DDES)Document10 pagesFinancial Guarantees: Department of Development and Environmental Services (DDES)Naveen KumarNo ratings yet

- Servicing Overview and Recent Regulatory Developments: Krista Cooley K&L Gates LLP 202-778-9257Document25 pagesServicing Overview and Recent Regulatory Developments: Krista Cooley K&L Gates LLP 202-778-9257Cairo AnubissNo ratings yet

- Program: Home Affordable Foreclosure AlternativesDocument5 pagesProgram: Home Affordable Foreclosure AlternativesJim LouisNo ratings yet

- MBA Regulatory Compliance Conference 2011 Litigation Forum - Session 4: EnforcementDocument24 pagesMBA Regulatory Compliance Conference 2011 Litigation Forum - Session 4: EnforcementCairo AnubissNo ratings yet

- NPA Management and Recovery Strategies: K K JindalDocument47 pagesNPA Management and Recovery Strategies: K K Jindalbansi2kkNo ratings yet

- 13Document63 pages13amysilverbergNo ratings yet

- Small Business Title COVID Package Section-By-Section 12.21.20Document10 pagesSmall Business Title COVID Package Section-By-Section 12.21.20Chad UrdahlNo ratings yet

- Lecture 8 - LiquidationDocument30 pagesLecture 8 - LiquidationSaurabh AroraNo ratings yet

- Defeasance and Your Deal PDFDocument8 pagesDefeasance and Your Deal PDFcleveland123100% (2)

- Webinar I HUD Early Delinquency Activities and Loss Mitigation Program Overview - ParticipantDocument37 pagesWebinar I HUD Early Delinquency Activities and Loss Mitigation Program Overview - ParticipantkwillsonNo ratings yet

- Management OF Non-Performing AssetsDocument31 pagesManagement OF Non-Performing AssetsPrashant RaiNo ratings yet

- Top 10 Foreclosure/Bankruptcy Servicing Issues: (Letterman Style)Document20 pagesTop 10 Foreclosure/Bankruptcy Servicing Issues: (Letterman Style)Cairo AnubissNo ratings yet

- Rent Control Fact SheetDocument7 pagesRent Control Fact SheetSteve LinNo ratings yet

- Servicing Regulation by Enforcement Action:: Understanding The New "Rules" and How To ComplyDocument25 pagesServicing Regulation by Enforcement Action:: Understanding The New "Rules" and How To ComplyCairo AnubissNo ratings yet

- 26contract & Construction ManagementDocument49 pages26contract & Construction ManagementManishParateNo ratings yet

- Chapter One: The Principles of Lending and Lending BasicsDocument23 pagesChapter One: The Principles of Lending and Lending BasicsSamuel サム VargheseNo ratings yet

- Capital Reconstruction-NoteDocument29 pagesCapital Reconstruction-NoteeoafriyieNo ratings yet

- Mortgage Fraud Recoupment:: Procedural Requirements and Issues Relating To Insurance, Bonds & Contractual IndemnitiesDocument18 pagesMortgage Fraud Recoupment:: Procedural Requirements and Issues Relating To Insurance, Bonds & Contractual IndemnitiesCairo AnubissNo ratings yet

- Short Sale Seminar Bakersfield, CADocument22 pagesShort Sale Seminar Bakersfield, CAMiguel GarciaNo ratings yet

- 1.1 Current LiabilitiesDocument13 pages1.1 Current Liabilitieskik leeNo ratings yet

- Alphabet Soup:: Hmda and Fcra/Fact ActDocument20 pagesAlphabet Soup:: Hmda and Fcra/Fact ActCairo AnubissNo ratings yet

- MBA's 2010 Legal Issues and Regulatory Compliance Conference Hotel Del Coronado San Diego, CADocument46 pagesMBA's 2010 Legal Issues and Regulatory Compliance Conference Hotel Del Coronado San Diego, CACairo AnubissNo ratings yet

- 13 Debt PolicyDocument7 pages13 Debt Policy1t4No ratings yet

- Housing Bond Basics: A Developer's PerspectiveDocument37 pagesHousing Bond Basics: A Developer's PerspectiveSrikanth VukkaNo ratings yet

- Summary of Mortgage Related Provisions of The Dodd-Frank Wall Street Reform and Consumer Protection ActDocument16 pagesSummary of Mortgage Related Provisions of The Dodd-Frank Wall Street Reform and Consumer Protection ActPaula HillockNo ratings yet

- M&A Disputes: A Professional Guide to Accounting ArbitrationsFrom EverandM&A Disputes: A Professional Guide to Accounting ArbitrationsNo ratings yet

- 5 Ways To Cash in On Notes. Just Click HEREDocument22 pages5 Ways To Cash in On Notes. Just Click HERERicharnellia-RichieRichBattiest-CollinsNo ratings yet

- Vazquez v. Deutsche Bank National Trust CompanyDocument5 pagesVazquez v. Deutsche Bank National Trust CompanyRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- SZYMONIAK NOT THE ORIGINAL SOURCE! DID SHE SCREW-OVER MANY OTHERS? FALSE CLAIMS ACT USED IN THIS NEWLY UNSEALED COMPLAINT--LYNN SZYMONIAK, THE FEDERAL GOVERNMENT AND MANY STATE GOVERNMENTS-AUGUST 2013- NAMES ALL THE BIG TIME BANKS---BUT STILL NO RELIEF FOR HOMEOWNERS FIGHTING FOR THEIR HOMES---NO CHAIN OF TITLEDocument145 pagesSZYMONIAK NOT THE ORIGINAL SOURCE! DID SHE SCREW-OVER MANY OTHERS? FALSE CLAIMS ACT USED IN THIS NEWLY UNSEALED COMPLAINT--LYNN SZYMONIAK, THE FEDERAL GOVERNMENT AND MANY STATE GOVERNMENTS-AUGUST 2013- NAMES ALL THE BIG TIME BANKS---BUT STILL NO RELIEF FOR HOMEOWNERS FIGHTING FOR THEIR HOMES---NO CHAIN OF TITLE83jjmackNo ratings yet

- In Re Tiffany M. KritharakisDocument12 pagesIn Re Tiffany M. KritharakisRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- Ohio Court Affirms Deutsche Bank's Foreclosure JudgmentDocument38 pagesOhio Court Affirms Deutsche Bank's Foreclosure JudgmentRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- FDCPA Case Law CitationsDocument18 pagesFDCPA Case Law CitationsCFLA, IncNo ratings yet

- How To Succeed As A Note BrokerDocument5 pagesHow To Succeed As A Note BrokerRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- 5th Cir. CT - Appeal - FDCPA Louisiana PDFDocument27 pages5th Cir. CT - Appeal - FDCPA Louisiana PDFRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- Osceola-Possible Fraud ForeclosuresDocument15 pagesOsceola-Possible Fraud ForeclosuresRicharnellia-RichieRichBattiest-Collins100% (1)

- Notice of Default Discharge of Obligation Demand For Re Conveyance To Donna Carpenter For First American Title Inter Lac Hen LNDocument4 pagesNotice of Default Discharge of Obligation Demand For Re Conveyance To Donna Carpenter For First American Title Inter Lac Hen LNPieter Panne100% (5)

- Federal Judge Cautiously Finds Against Bank On Foreclosure Advertisement 3 12Document9 pagesFederal Judge Cautiously Finds Against Bank On Foreclosure Advertisement 3 12Richarnellia-RichieRichBattiest-CollinsNo ratings yet

- How To Write and Market Your BookDocument52 pagesHow To Write and Market Your BookRicharnellia-RichieRichBattiest-Collins100% (1)

- Civil Procedure - Annulment of Executory Proceedings After SaleDocument9 pagesCivil Procedure - Annulment of Executory Proceedings After SaleRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- Notice of Default Discharge of Obligation Demand For Re Conveyance To Donna Carpenter For First American Title Inter Lac Hen LNDocument4 pagesNotice of Default Discharge of Obligation Demand For Re Conveyance To Donna Carpenter For First American Title Inter Lac Hen LNPieter Panne100% (5)

- Wrong Plaintiff Wrong Defendant Beware A Motion For Sanctions 8 08Document7 pagesWrong Plaintiff Wrong Defendant Beware A Motion For Sanctions 8 08Richarnellia-RichieRichBattiest-CollinsNo ratings yet

- Yarney V Ocwen USD VA FDCPA Breach ContractDocument17 pagesYarney V Ocwen USD VA FDCPA Breach ContractMike_Dillon100% (1)

- Sample Query Letter Non FictionDocument1 pageSample Query Letter Non FictionRicharnellia-RichieRichBattiest-Collins100% (1)

- Writing Effectively and PowerfullyDocument38 pagesWriting Effectively and PowerfullynunaazulNo ratings yet

- Report Servicers ModifyDocument60 pagesReport Servicers ModifyTammy SallamNo ratings yet

- P-47 WN Template Writing - HandoutDocument12 pagesP-47 WN Template Writing - HandoutRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- Is Mers in Your MortgageDocument9 pagesIs Mers in Your MortgageRicharnellia-RichieRichBattiest-Collins67% (3)

- Thesis TopicFile 38Document1 pageThesis TopicFile 38Richarnellia-RichieRichBattiest-CollinsNo ratings yet

- P-47 WN-Book Writing Layout TemplateDocument34 pagesP-47 WN-Book Writing Layout TemplateSharon B. James100% (1)

- Foreclosing Modifications - How Servicer Incentives Discourage Loan ModificationsDocument86 pagesForeclosing Modifications - How Servicer Incentives Discourage Loan ModificationsRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- Subprime Standardization How Rating Agencies Allow Predatory Lending To Flourish in The Secondary Mortgage MarketDocument82 pagesSubprime Standardization How Rating Agencies Allow Predatory Lending To Flourish in The Secondary Mortgage MarketForeclosure FraudNo ratings yet

- Truth in Lending Act (Regulation Z) 2012 - National Consumer Advocates - Reverse Mortgages.Document10 pagesTruth in Lending Act (Regulation Z) 2012 - National Consumer Advocates - Reverse Mortgages.Richarnellia-RichieRichBattiest-CollinsNo ratings yet

- Humpty Dumpty and The Foreclosure Crisis - Braucher On HampDocument62 pagesHumpty Dumpty and The Foreclosure Crisis - Braucher On HampRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- The Florida Foreclosure Judge's Bench BookDocument53 pagesThe Florida Foreclosure Judge's Bench BookForeclosure Fraud100% (4)

- Property Title Trouble in Non-Judicial Foreclosure States - The Ibanez Time BombDocument81 pagesProperty Title Trouble in Non-Judicial Foreclosure States - The Ibanez Time BombRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- Truth in Lending (TILA) Rules For Closed End - National Consumer AdvocatesDocument229 pagesTruth in Lending (TILA) Rules For Closed End - National Consumer AdvocatesRicharnellia-RichieRichBattiest-CollinsNo ratings yet

- Time and Action PlanDocument6 pagesTime and Action PlanSadhana YadavNo ratings yet

- Assignment-5 BL (Partnership Act)Document7 pagesAssignment-5 BL (Partnership Act)Ganesh SobanapuramNo ratings yet

- Diva Arbitrage Fund PresentationDocument65 pagesDiva Arbitrage Fund Presentationchuff6675No ratings yet

- Tabangao Shell Refinery Employees Association v. Pilipinas Shell Petroleum CorporationDocument26 pagesTabangao Shell Refinery Employees Association v. Pilipinas Shell Petroleum CorporationAnnie Herrera-LimNo ratings yet

- L.1021 - Extended Producer Responsibility - Guidelines For Sustainable E-Waste ManagementDocument44 pagesL.1021 - Extended Producer Responsibility - Guidelines For Sustainable E-Waste Managementmariiusssica2008No ratings yet

- 12 - Conclusion and Suggestion PDFDocument13 pages12 - Conclusion and Suggestion PDFAnneshaNo ratings yet

- Project Quality Plan - 039700 REV D ONLY (5868)Document42 pagesProject Quality Plan - 039700 REV D ONLY (5868)JaseelKanhirathinkal100% (1)

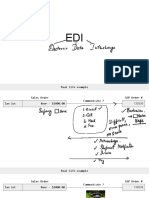

- EDI: The Foundation of Digital Business IntegrationDocument61 pagesEDI: The Foundation of Digital Business IntegrationYasmine ArabNo ratings yet

- Post Adjusting Entries to T AccountsDocument13 pagesPost Adjusting Entries to T Accountsklm klmNo ratings yet

- The Family Finance WorkshopDocument40 pagesThe Family Finance WorkshopPierre PucheuNo ratings yet

- Atty. Orocio vs. Angulan Et Al - G.R. No. 179892-93 - January 30, 2009Document17 pagesAtty. Orocio vs. Angulan Et Al - G.R. No. 179892-93 - January 30, 2009Nikki BinsinNo ratings yet

- Muhammad Hassan Muhammad Hassan: ObjectiveDocument2 pagesMuhammad Hassan Muhammad Hassan: ObjectiveMohammad Hassan GhumroNo ratings yet

- 3 PDFDocument9 pages3 PDFSanjeev PradhanNo ratings yet

- Project Report on the History of Emirates AirlineDocument38 pagesProject Report on the History of Emirates AirlineAmit Choudhary100% (1)

- Emerson Electric's Strategic Planning and Performance OptimizationDocument3 pagesEmerson Electric's Strategic Planning and Performance OptimizationSilver BulletNo ratings yet

- PC1 JozaraDocument40 pagesPC1 JozaraFarhat Durrani0% (1)

- HVS - HVS-Anarock-India-Hospitality-Industry-Review-2018Document18 pagesHVS - HVS-Anarock-India-Hospitality-Industry-Review-2018Vinod PatelNo ratings yet

- Chime Bank Statement NirtDocument3 pagesChime Bank Statement Nirtfehijan689No ratings yet

- Rupee Appreciation & Its Impact On Indian EconomyDocument20 pagesRupee Appreciation & Its Impact On Indian EconomyShweta Gopika ChopraNo ratings yet

- ASMM 8.2 - OverviewDocument50 pagesASMM 8.2 - OverviewShweta Dubey SinghNo ratings yet

- Class XI Accountancy Project 2021 - 22Document14 pagesClass XI Accountancy Project 2021 - 22ethan playz81% (63)

- Facility LocationDocument56 pagesFacility Locationanon-930959100% (7)

- Flight Ticket - Rajkot To Mumbai: Fare Rules & BaggageDocument2 pagesFlight Ticket - Rajkot To Mumbai: Fare Rules & BaggageguptamukeshNo ratings yet

- Chapter 5Document67 pagesChapter 5saad107No ratings yet

- What Are The Ethical and Privacy Issues That Harrah's Should Be Concerned AboutDocument5 pagesWhat Are The Ethical and Privacy Issues That Harrah's Should Be Concerned AboutVarun BangotraNo ratings yet

- Nishant Bhaskar PortfolioDocument9 pagesNishant Bhaskar PortfolioN. BhaskarNo ratings yet

- Amalgamation ChecklistDocument101 pagesAmalgamation ChecklistSabeena KhanNo ratings yet

- Solomon Corporation Acquires South Dakota Transformer Repair Facility From A-LineDocument2 pagesSolomon Corporation Acquires South Dakota Transformer Repair Facility From A-LinePR.comNo ratings yet

- Flirtonomics - For Immediate ReleaseDocument1 pageFlirtonomics - For Immediate ReleaseMarc CampmanNo ratings yet

- Tutorial - Demand & SupplyDocument3 pagesTutorial - Demand & SupplyYee Sin MeiNo ratings yet