You might also like

- DIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)From EverandDIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)No ratings yet

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingFrom EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingNo ratings yet

- Portfolio Management - Part 2: Portfolio Management, #2From EverandPortfolio Management - Part 2: Portfolio Management, #2Rating: 5 out of 5 stars5/5 (9)

- Mastering the Markets: Advanced Trading Strategies for Success and Ethical Trading PracticesFrom EverandMastering the Markets: Advanced Trading Strategies for Success and Ethical Trading PracticesNo ratings yet

- ANALYSIS OF SPECIFIC EQUITY SHARES IN STOCK NSEDocument71 pagesANALYSIS OF SPECIFIC EQUITY SHARES IN STOCK NSERajesh BathulaNo ratings yet

- A Study On Equity Analysis With Respect To Banking Sector at INDIABULLSDocument20 pagesA Study On Equity Analysis With Respect To Banking Sector at INDIABULLSNationalinstituteDsnr0% (1)

- Index Funds: A Beginner's Guide to Build Wealth Through Diversified ETFs and Low-Cost Passive Investments for Long-Term Financial Security with Minimum Time and EffortFrom EverandIndex Funds: A Beginner's Guide to Build Wealth Through Diversified ETFs and Low-Cost Passive Investments for Long-Term Financial Security with Minimum Time and EffortRating: 5 out of 5 stars5/5 (38)

- Equity Research On Paint and FMCG SectorDocument43 pagesEquity Research On Paint and FMCG SectornehagadgeNo ratings yet

- A Study On Portfolio Management: Wesley Post Graduate College Osmania University 2009 - 2011Document73 pagesA Study On Portfolio Management: Wesley Post Graduate College Osmania University 2009 - 2011Neelam VijaywargiNo ratings yet

- Synopsis On A Comparative Study of Equity Linked Savings Schemes Floated by Domestic Mutual Fund PlayersDocument8 pagesSynopsis On A Comparative Study of Equity Linked Savings Schemes Floated by Domestic Mutual Fund PlayersPraveen Sehgal100% (1)

- Project On Impact of Dividends Policy 1Document43 pagesProject On Impact of Dividends Policy 1Soma BanikNo ratings yet

- Investors' Investment PreferencesDocument50 pagesInvestors' Investment PreferencesLeeladhar KushwahaNo ratings yet

- Understanding Investors and Equity MarketsDocument81 pagesUnderstanding Investors and Equity Marketschaluvadiin100% (2)

- A Project Report On Equity Analysis at Kotak Security, HyderabadDocument92 pagesA Project Report On Equity Analysis at Kotak Security, Hyderabadcity cyberNo ratings yet

- EQUITY ANALYSIS GSTDocument24 pagesEQUITY ANALYSIS GSTnithashaindrojuNo ratings yet

- Project On Impact of Dividends PolicyDocument45 pagesProject On Impact of Dividends Policyarjunmba119624100% (1)

- Investing in Mutual Funds: Factors to ConsiderDocument4 pagesInvesting in Mutual Funds: Factors to ConsiderSatbir Ratti33% (3)

- How To Begin Investing In The Stock Market: Obtaining Financial FreedomFrom EverandHow To Begin Investing In The Stock Market: Obtaining Financial FreedomNo ratings yet

- A simple approach to bond trading: The introductory guide to bond investments and their portfolio managementFrom EverandA simple approach to bond trading: The introductory guide to bond investments and their portfolio managementRating: 5 out of 5 stars5/5 (1)

- An Empirical Study On Performance of Mutual Funds in IndiaDocument5 pagesAn Empirical Study On Performance of Mutual Funds in Indiaanon_336382763No ratings yet

- Equity Analysis Pharma and It SectorDocument88 pagesEquity Analysis Pharma and It SectorcityNo ratings yet

- Equity Analysis of SBI Bank-1Document69 pagesEquity Analysis of SBI Bank-1mustafe ABDULLAHINo ratings yet

- Influence of Portfolio in Investment Decision Making - CD EquityDocument98 pagesInfluence of Portfolio in Investment Decision Making - CD Equityrajesh bathulaNo ratings yet

- Equity Analysis in Banking sector-ICICI Direct New WordDocument56 pagesEquity Analysis in Banking sector-ICICI Direct New WordJoshua heavenNo ratings yet

- Managing Stock Portfolios: Understanding Market and Sector ImpactsDocument7 pagesManaging Stock Portfolios: Understanding Market and Sector Impactsmutia rasyaNo ratings yet

- How to Create and Maintain a Diversified Investment Portfolio: A Comprehensive Guide on Investment and Portfolio ManagementFrom EverandHow to Create and Maintain a Diversified Investment Portfolio: A Comprehensive Guide on Investment and Portfolio ManagementNo ratings yet

- Investment Gems: Exploring Lucrative Opportunities in IPOs, ETFs, and Mutual FundsFrom EverandInvestment Gems: Exploring Lucrative Opportunities in IPOs, ETFs, and Mutual FundsNo ratings yet

- Black Book Online Trading and Stock BrokingDocument53 pagesBlack Book Online Trading and Stock BrokingAditya LokareNo ratings yet

- 10 Steps To Invest in Equity - SFLBDocument3 pages10 Steps To Invest in Equity - SFLBSudhir AnandNo ratings yet

- Equity Research On Paint and FMCG SectorDocument47 pagesEquity Research On Paint and FMCG SectornehagadgeNo ratings yet

- Bill MillerDocument6 pagesBill Millerfrans leonard100% (1)

- Risk Return Analysis EDELWEISSDocument73 pagesRisk Return Analysis EDELWEISSPrathapReddyNo ratings yet

- Investing Made Simple - Warren Buffet Strategies To Building Wealth And Creating Passive IncomeFrom EverandInvesting Made Simple - Warren Buffet Strategies To Building Wealth And Creating Passive IncomeNo ratings yet

- The Case For Low-Cost Index Fund Investing - Thierry PollaDocument19 pagesThe Case For Low-Cost Index Fund Investing - Thierry PollaThierry Polla100% (1)

- Securities Analysis & Portfolio Management GuideDocument52 pagesSecurities Analysis & Portfolio Management GuideruchisinghnovNo ratings yet

- Project Report On Portfolio ConstructionDocument37 pagesProject Report On Portfolio ConstructionMazhar Zaman67% (3)

- Equity FundsDocument3 pagesEquity FundsRosyDayNo ratings yet

- Fundamental Analysis of SecuritiesDocument86 pagesFundamental Analysis of SecuritiesRashid SiddiquiNo ratings yet

- Mutual Funds vs ETFs: Which is BetterDocument34 pagesMutual Funds vs ETFs: Which is BetterAayushi jainNo ratings yet

- Situational Analysis Equity Analysis: Objectives of The StudyDocument4 pagesSituational Analysis Equity Analysis: Objectives of The StudyNipul BafnaNo ratings yet

- The Case For Low-Cost Index-Fund Investing: Vanguard Research April 2019Document20 pagesThe Case For Low-Cost Index-Fund Investing: Vanguard Research April 2019budNo ratings yet

- Fundamental Aanalysis On ICICI BankDocument56 pagesFundamental Aanalysis On ICICI BankAsif KhanNo ratings yet

- Bhavesh Sawant Bhuvan DalviDocument8 pagesBhavesh Sawant Bhuvan DalviBhuvan DalviNo ratings yet

- Securities Analysis & Portfolio Management IntroDocument50 pagesSecurities Analysis & Portfolio Management IntrogirishNo ratings yet

- Equity Portfolio ManagementDocument22 pagesEquity Portfolio ManagementMayur DaveNo ratings yet

- How to Make Money Trading Stocks & Shares: A comprehensive manual for achieving financial success in the marketFrom EverandHow to Make Money Trading Stocks & Shares: A comprehensive manual for achieving financial success in the marketNo ratings yet

- Sectoral Funds Outperformed Diversified FundsDocument21 pagesSectoral Funds Outperformed Diversified FundsMalathi KuttyNo ratings yet

- Thesis - MiniDocument10 pagesThesis - MiniDr Waseem CNo ratings yet

- EMH AssignmentDocument8 pagesEMH AssignmentJonathanNo ratings yet

- Sip Report On Investment OptionsDocument17 pagesSip Report On Investment OptionsSravani Reddy BodduNo ratings yet

- Investment ProcessDocument3 pagesInvestment Processq2boby100% (4)

- Creating and Monitoring A Diversified Stock PortfolioDocument11 pagesCreating and Monitoring A Diversified Stock Portfolioసతీష్ మండవNo ratings yet

- CMTMNT Letr 2Document1 pageCMTMNT Letr 2Arun OusephNo ratings yet

- BrandingDocument20 pagesBrandingArun OusephNo ratings yet

- Anthi Kkadappurath OrolakkudayeduthuDocument2 pagesAnthi Kkadappurath OrolakkudayeduthuArun OusephNo ratings yet

- HRM CaseDocument4 pagesHRM CaseArun OusephNo ratings yet

- A True Entrepreneur Is A DoerDocument1 pageA True Entrepreneur Is A DoerArun OusephNo ratings yet

- Brand Positioning Mini ProjectDocument58 pagesBrand Positioning Mini Projectmohangoel99100% (7)

- 1 Analysis of Gold Loan Business of K.S.F.EDocument77 pages1 Analysis of Gold Loan Business of K.S.F.EArun OusephNo ratings yet

- 1 Analysis of Gold Loan Business of K.S.F.EDocument77 pages1 Analysis of Gold Loan Business of K.S.F.EArun OusephNo ratings yet

- ADR Issue ProcessDocument2 pagesADR Issue ProcessAishwarya RamakrishnaNo ratings yet

- Acc 108 Current LiabilitiesDocument5 pagesAcc 108 Current Liabilitiesmkrisnaharq99No ratings yet

- BIR EAccReg System Walkthrough For TP Users - RZMDocument121 pagesBIR EAccReg System Walkthrough For TP Users - RZMMark Lord Morales BumagatNo ratings yet

- DP & Trading Combine Closure Request Form - 2Document2 pagesDP & Trading Combine Closure Request Form - 2Supriya DasNo ratings yet

- IBPA Yield Curve: Daily Price & Fair Values Indonesia Corporate BondsDocument11 pagesIBPA Yield Curve: Daily Price & Fair Values Indonesia Corporate Bondsbintar_21No ratings yet

- Chap012 2Document125 pagesChap012 2Aai NurrNo ratings yet

- Answer - CHAPTER 7 FUTURES AND OPTIONS ON FOREIGN EXCHANGEDocument7 pagesAnswer - CHAPTER 7 FUTURES AND OPTIONS ON FOREIGN EXCHANGETRÂM BÙI THỊ MAINo ratings yet

- Daily Price HistoryDocument574 pagesDaily Price HistoryrockingjoeNo ratings yet

- Compliance Officers (Brokers) Module Curriculum 1.Document2 pagesCompliance Officers (Brokers) Module Curriculum 1.ambreenkhanamNo ratings yet

- Wim Plast - Annual Report 2022Document168 pagesWim Plast - Annual Report 2022Kritibandhu SwainNo ratings yet

- Summer Project On Kotak SecuritiesDocument55 pagesSummer Project On Kotak SecuritiesAvinash Singh75% (16)

- Example Table Changes in EquityDocument2 pagesExample Table Changes in EquitySam VNo ratings yet

- Example SwapDocument10 pagesExample SwapThanh Huyền TrầnNo ratings yet

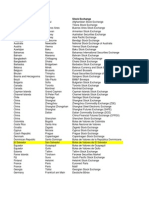

- List of Stock ExchangeDocument15 pagesList of Stock ExchangeTimothy MununuziNo ratings yet

- MFE FormulaDocument28 pagesMFE Formulajes_kur100% (1)

- ICICI Balanced Advantage Fund - One PagerDocument2 pagesICICI Balanced Advantage Fund - One PagerjoycoolNo ratings yet

- Financial Futures Markets: © 2003 South-Western/Thomson LearningDocument35 pagesFinancial Futures Markets: © 2003 South-Western/Thomson LearningM. Usama ZakaNo ratings yet

- Mechanics of Options MarketsDocument31 pagesMechanics of Options MarketsPriyank PipaliaNo ratings yet

- Earning and Stock Split - Asquith Et Al 1989Document18 pagesEarning and Stock Split - Asquith Et Al 1989Fransiskus ShaulimNo ratings yet

- ClassSession 26 - Dell Case - HandoutsDocument43 pagesClassSession 26 - Dell Case - Handoutsdrey baxterNo ratings yet

- Hedge Fund Strategies, Mutual Fund Comparison & Fund of FundsDocument46 pagesHedge Fund Strategies, Mutual Fund Comparison & Fund of Fundsbboyvn100% (1)

- Mutual Fund Report Feb-20Document39 pagesMutual Fund Report Feb-20muddasir1980No ratings yet

- AC216 Unit 4 Assignment 5 - Amortization MorganDocument2 pagesAC216 Unit 4 Assignment 5 - Amortization MorganEliana Morgan100% (1)

- Introduction to key Indian financial markets infrastructureDocument69 pagesIntroduction to key Indian financial markets infrastructureanon_517749135No ratings yet

- Running Account AuthorisationDocument1 pageRunning Account AuthorisationTirthGanatraNo ratings yet

- TM Tut 13 Credit Derivatives Revision PDFDocument5 pagesTM Tut 13 Credit Derivatives Revision PDFQuynh Ngoc DangNo ratings yet

- Study of Stock Market and Analysis of Infrastructure SectorDocument82 pagesStudy of Stock Market and Analysis of Infrastructure SectorRupali BoradeNo ratings yet

- Stock Valuation - Practice QuestionsDocument2 pagesStock Valuation - Practice QuestionsMuhammad Mansoor0% (1)

- FM11 CH 7 Mini-Case Old10Document11 pagesFM11 CH 7 Mini-Case Old10AGNo ratings yet