You might also like

- Chapter 7Document6 pagesChapter 7Muhammed YismawNo ratings yet

- Risk:: The Two Major Types of Risks AreDocument16 pagesRisk:: The Two Major Types of Risks AreAbhishek TyagiNo ratings yet

- MUSEDocument12 pagesMUSEmuse tamiruNo ratings yet

- The Portfoli Theory: Systematic Risk - These Are Market Risks That Cannot Be Diversified Away. InterestDocument12 pagesThe Portfoli Theory: Systematic Risk - These Are Market Risks That Cannot Be Diversified Away. Interestmuse tamiruNo ratings yet

- Reduction of Portfolio Risk Through DiversificationDocument38 pagesReduction of Portfolio Risk Through DiversificationDilshaad Shaikh100% (1)

- DiversificationDocument8 pagesDiversificationambulahbdugNo ratings yet

- Objective of Study Concepts Investment Options Data Collection Analysis Recommendation Limitations ReferencesDocument26 pagesObjective of Study Concepts Investment Options Data Collection Analysis Recommendation Limitations Referenceshtikyani_1No ratings yet

- Risk & Return Analysis - Prime BookDocument25 pagesRisk & Return Analysis - Prime Bookßïshñü PhüyãlNo ratings yet

- Answers To Concepts in Review: S R R NDocument5 pagesAnswers To Concepts in Review: S R R NJerine TanNo ratings yet

- Portfolio TheoryDocument3 pagesPortfolio TheoryZain MughalNo ratings yet

- Unit-2 Portfolio Analysis &selectionDocument64 pagesUnit-2 Portfolio Analysis &selectiontanishq8807No ratings yet

- Harry Markowitz's Modern Portfolio Theory: The Efficient FrontierDocument7 pagesHarry Markowitz's Modern Portfolio Theory: The Efficient Frontiermahbobullah rahmaniNo ratings yet

- Unit 4Document17 pagesUnit 4vivek badhanNo ratings yet

- Powerpoint Concept Smjhne Security-Analysis-and-Portfolo-Management-Unit-4-Dr-Asma-KhanDocument66 pagesPowerpoint Concept Smjhne Security-Analysis-and-Portfolo-Management-Unit-4-Dr-Asma-KhanShailjaNo ratings yet

- Understanding The Efficient FrontierDocument4 pagesUnderstanding The Efficient FrontierThanh Tu NguyenNo ratings yet

- Diversification (Finance)Document8 pagesDiversification (Finance)ElsenNo ratings yet

- Basics of FinanceDocument46 pagesBasics of Financeisrael_zamora6389No ratings yet

- Finman3 Report DiscussionDocument5 pagesFinman3 Report DiscussionFlorence CuansoNo ratings yet

- Chapter-2 Portfolio Analysis and SelectionDocument14 pagesChapter-2 Portfolio Analysis and Selection8008 Aman GuptaNo ratings yet

- Understanding Risk and ReturnDocument5 pagesUnderstanding Risk and ReturnFORCHIA MAE CUTARNo ratings yet

- 17 Investment ManagementDocument20 pages17 Investment ManagementAdebajo AbdulrazaqNo ratings yet

- Safe Investment??: (A Case Study On Risk of Diversification)Document26 pagesSafe Investment??: (A Case Study On Risk of Diversification)A Srihari KrishnaNo ratings yet

- Introduction To Portfolio ManagementDocument84 pagesIntroduction To Portfolio ManagementRadhika SivadiNo ratings yet

- Risk Return AnalysisDocument1 pageRisk Return Analysissnehachandan91No ratings yet

- Portfolio Evaluation and RevisionDocument53 pagesPortfolio Evaluation and Revisionjibumon k gNo ratings yet

- Portfolio 8Document4 pagesPortfolio 8Saloni NeelamNo ratings yet

- Portfolio Theory - Ses2Document82 pagesPortfolio Theory - Ses2Vaidyanathan Ravichandran100% (1)

- Definition of Portfolio AnalysisDocument15 pagesDefinition of Portfolio Analysissimrenchoudhary057No ratings yet

- Portfolio ConstructionDocument13 pagesPortfolio ConstructionRonak GosaliaNo ratings yet

- Risk Return Analysis-IIFLDocument131 pagesRisk Return Analysis-IIFLPrathapReddy100% (1)

- Portfolio Selection Summary FMPDocument3 pagesPortfolio Selection Summary FMPMufti AliNo ratings yet

- Earnings Per Share-ProDocument3 pagesEarnings Per Share-ProVibhorBajpaiNo ratings yet

- 3.1 Portfolio TheoryDocument15 pages3.1 Portfolio TheoryRajarshi DaharwalNo ratings yet

- Retail Banking Assignment Yashkumar Patel 17020942046: Ans. Modern Portfolio TheoryDocument5 pagesRetail Banking Assignment Yashkumar Patel 17020942046: Ans. Modern Portfolio TheoryYashkumar PatelNo ratings yet

- Basics of FinanceDocument46 pagesBasics of FinanceELgün F. QurbanovNo ratings yet

- BBA Unit 5Document4 pagesBBA Unit 5gorang GehaniNo ratings yet

- Risk Return Analysis Analysis of Banking and FMCG StocksDocument93 pagesRisk Return Analysis Analysis of Banking and FMCG StocksbhagathnagarNo ratings yet

- Topic: What Do You Understand by Efficient Frontier (With Diagram) ? IntroductionDocument2 pagesTopic: What Do You Understand by Efficient Frontier (With Diagram) ? Introductiondeepti sharmaNo ratings yet

- Investment Management FAQDocument3 pagesInvestment Management FAQRockyBalboaaNo ratings yet

- Portfolio Management - Module 2Document16 pagesPortfolio Management - Module 2satyamchoudhary2004No ratings yet

- Risk and Return For Single SecuritiesDocument10 pagesRisk and Return For Single Securitieskritigupta.may1999No ratings yet

- Investment, Security and Portfolio ManagementDocument396 pagesInvestment, Security and Portfolio ManagementSM FriendNo ratings yet

- Unit 2 PORTFOLIO RISK AND RETURNDocument19 pagesUnit 2 PORTFOLIO RISK AND RETURNmahi jainNo ratings yet

- M6 Assignment 1Document3 pagesM6 Assignment 1Lorraine CaliwanNo ratings yet

- Chapter 7Document11 pagesChapter 7Seid KassawNo ratings yet

- Markowitz ModelDocument25 pagesMarkowitz ModelVignesh PrabhuNo ratings yet

- Corporate Portfolio Analysis TechniquesDocument24 pagesCorporate Portfolio Analysis TechniquesSanjay DhageNo ratings yet

- Chapter 6 NotesDocument2 pagesChapter 6 Notesazhar80malikNo ratings yet

- Chapter - 1Document69 pagesChapter - 1111induNo ratings yet

- BAUTISTA BAFIMARX ACT181, Activity 2Document3 pagesBAUTISTA BAFIMARX ACT181, Activity 2Joshua BautistaNo ratings yet

- Investment Portfolio Diversification:: Diversify Our Company InvestmentsDocument4 pagesInvestment Portfolio Diversification:: Diversify Our Company Investmentsfiza akhterNo ratings yet

- Risk and ReturnDocument7 pagesRisk and Returnshinobu kochoNo ratings yet

- IA - Limitation in PortfolioDocument4 pagesIA - Limitation in PortfolioJustina BaharunNo ratings yet

- What Is Portfolio ManagementDocument2 pagesWhat Is Portfolio ManagementTariq MahmoodNo ratings yet

- Portfoli o Anaysi S: Financial Manageme NTDocument3 pagesPortfoli o Anaysi S: Financial Manageme NTRahul BaidNo ratings yet

- Modern Portfolio Theory (Markowitz)Document6 pagesModern Portfolio Theory (Markowitz)Millat AfridiNo ratings yet

- Dipu MedicalDocument1 pageDipu MedicalPranjit BhuyanNo ratings yet

- TZBT LRQCMG ONg DwoDocument6 pagesTZBT LRQCMG ONg DwoPranjit BhuyanNo ratings yet

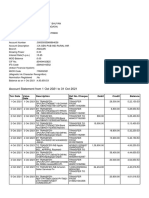

- Account Statement From 1 Nov 2021 To 30 Nov 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 1 Nov 2021 To 30 Nov 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancePranjit BhuyanNo ratings yet

- Investment ManagementDocument38 pagesInvestment ManagementPranjit BhuyanNo ratings yet

- Management Information SystemDocument98 pagesManagement Information SystemPranjit BhuyanNo ratings yet

- Indifference Curve, Which Reflects That Investor's Preferences Regarding Risk and Return, IsDocument5 pagesIndifference Curve, Which Reflects That Investor's Preferences Regarding Risk and Return, Ismd mehedi hasanNo ratings yet

- Rev 1 - Prelim Examination - From Partnership Formation To Joint ArrangemeDocument6 pagesRev 1 - Prelim Examination - From Partnership Formation To Joint ArrangemeCM Lance100% (2)

- Islamic QuizDocument4 pagesIslamic QuizSharmila DeviNo ratings yet

- Fra Project FinalllDocument23 pagesFra Project Finalllshahtaj khanNo ratings yet

- Project Report FormatDocument9 pagesProject Report FormatGiri SukumarNo ratings yet

- CHPTR 4 Project Analysis and EvaluationDocument32 pagesCHPTR 4 Project Analysis and EvaluationSivaranjini KaliappanNo ratings yet

- Quantitative Investment Analysis CFA Institute Investment SeriesDocument159 pagesQuantitative Investment Analysis CFA Institute Investment SeriesMuhamad ArmawaddinNo ratings yet

- Stock Market - Black BookDocument82 pagesStock Market - Black BookHrisha Bhatt62% (52)

- The FVA - Forward Volatility AgreementDocument9 pagesThe FVA - Forward Volatility Agreementshih_kaichih100% (1)

- FAIIQuiz 1 BsolDocument3 pagesFAIIQuiz 1 BsolHuzaifa Bin SaeedNo ratings yet

- Chapter 005Document30 pagesChapter 005Yinan Lu100% (2)

- IFIC Bank Internship ReportDocument136 pagesIFIC Bank Internship ReportAppleNo ratings yet

- Accenture Strategy ZBX Zero Based Transformation POV July2019Document9 pagesAccenture Strategy ZBX Zero Based Transformation POV July2019Deepak SharmaNo ratings yet

- BIM Experiences and Expectations: The Constructors' PerspectiveDocument24 pagesBIM Experiences and Expectations: The Constructors' PerspectiveArifNo ratings yet

- CF 26051Document20 pagesCF 26051sdfdsfNo ratings yet

- Credit Management System of IFIC Bank LTDDocument73 pagesCredit Management System of IFIC Bank LTDHasib SimantoNo ratings yet

- 12.course OutlineDocument3 pages12.course OutlineMD. ANWAR UL HAQUENo ratings yet

- Revised Amlc TrancodesDocument25 pagesRevised Amlc TrancodesGuevarraWellrhoNo ratings yet

- Quick Take: Ashok Leyland LTDDocument8 pagesQuick Take: Ashok Leyland LTDshrikantmsdNo ratings yet

- Quiz 5Document5 pagesQuiz 5Lê Thanh ThủyNo ratings yet

- Loan SalesDocument17 pagesLoan SalesWILLY SETIAWANNo ratings yet

- By LawsDocument8 pagesBy LawsChrissy SabellaNo ratings yet

- Bottled Water Strategy in UKDocument19 pagesBottled Water Strategy in UKshibin21No ratings yet

- Business Standard English DelhiDocument25 pagesBusiness Standard English DelhiRajan NandolaNo ratings yet

- QWDocument23 pagesQWCarlo Angelo CastilloNo ratings yet

- LS4-7 (3) MARIANO - EditedDocument16 pagesLS4-7 (3) MARIANO - EditedarnelNo ratings yet

- The Option Value of LifeDocument21 pagesThe Option Value of LifeSusanne BurriNo ratings yet

- Business Credit Made EasyDocument68 pagesBusiness Credit Made Easylabeledagenius100% (25)

- 5 6152282107373683204Document49 pages5 6152282107373683204Musyahadah ZauqiNo ratings yet