You might also like

- Risk and Rates of Return: Learning ObjectivesDocument36 pagesRisk and Rates of Return: Learning Objectivesssregens82No ratings yet

- Static Picture Effects For Powerpoint Slides: Reproductio N Instructions Printing Instructions Removing InstructionsDocument17 pagesStatic Picture Effects For Powerpoint Slides: Reproductio N Instructions Printing Instructions Removing Instructionsssregens82No ratings yet

- Building Multi-Tier Web Applications in Virtual EnvironmentsDocument30 pagesBuilding Multi-Tier Web Applications in Virtual Environmentsssregens82No ratings yet

- Orchestro State Inventory Management 2015Document8 pagesOrchestro State Inventory Management 2015ssregens82No ratings yet

- Lussier 3 Ech 05Document50 pagesLussier 3 Ech 05ssregens82No ratings yet

- CHP 3Document2 pagesCHP 3ssregens82No ratings yet

- Supplier General QualificationsDocument3 pagesSupplier General Qualificationsssregens82No ratings yet

- Judicial Power of Supreme CourtDocument2 pagesJudicial Power of Supreme Courtssregens82No ratings yet

- Week 8 AssignmentDocument5 pagesWeek 8 Assignmentssregens82100% (2)

- Transportation and Logistics OptimizationDocument18 pagesTransportation and Logistics Optimizationssregens82No ratings yet

- AMIS 525 Pop Quiz - Chapters 22 and 23Document5 pagesAMIS 525 Pop Quiz - Chapters 22 and 23ssregens82No ratings yet

- Regular Flow Irregular Flow Irregular Flow DepreciationDocument1 pageRegular Flow Irregular Flow Irregular Flow Depreciationssregens82No ratings yet

- Problems, Problem Spaces and Search: Dr. Suthikshn KumarDocument47 pagesProblems, Problem Spaces and Search: Dr. Suthikshn Kumarssregens82No ratings yet

- V Ac - SC V (Aa Ar) - (Sa SR) V (Aa Ar) - (Aa SR) + (Aa SR) - (Sa SR) V ( (Aa Ar) - (Aa SR) ) + ( (Aa SR) - (Sa SR) )Document1 pageV Ac - SC V (Aa Ar) - (Sa SR) V (Aa Ar) - (Aa SR) + (Aa SR) - (Sa SR) V ( (Aa Ar) - (Aa SR) ) + ( (Aa SR) - (Sa SR) )ssregens82No ratings yet

- TPRICEDocument1 pageTPRICEssregens82No ratings yet

- Chapter 1 BowersoxDocument38 pagesChapter 1 Bowersoxssregens82100% (1)

- Vcost DemoDocument2 pagesVcost Demossregens82No ratings yet

- Signs For Income VarianceDocument1 pageSigns For Income Variancessregens82No ratings yet

- Time Value PracticeDocument1 pageTime Value Practicessregens82No ratings yet

- Process StepsDocument1 pageProcess Stepsssregens82No ratings yet

- I (P Q) - (V Q) - F: The Fundamental EquationDocument1 pageI (P Q) - (V Q) - F: The Fundamental Equationssregens82No ratings yet

- Ri RoiDocument1 pageRi Roissregens82No ratings yet

- Percent DoneDocument1 pagePercent Donessregens82No ratings yet

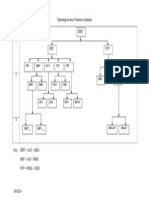

- Operating Income Variances DiagramDocument1 pageOperating Income Variances Diagramssregens82No ratings yet

- Total For 5 Years Each YearDocument1 pageTotal For 5 Years Each Yearssregens82No ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Lecture On Fundamental Analysis - Dr. NiveditaDocument32 pagesLecture On Fundamental Analysis - Dr. NiveditaSanjanaNo ratings yet

- Asset Accounting Year End CloseDocument16 pagesAsset Accounting Year End ClosePriya MadhuNo ratings yet

- BAM PPT 2019-09 Investor DayDocument92 pagesBAM PPT 2019-09 Investor DayRocco HuangNo ratings yet

- The Implementation of Customer Due Diligence Princinple For Electronic Money As Preventive Measures of Terrorism Financing in Bank XDocument221 pagesThe Implementation of Customer Due Diligence Princinple For Electronic Money As Preventive Measures of Terrorism Financing in Bank XOddy Ramadhika SusmoyoNo ratings yet

- Bengkalis MuriaDocument10 pagesBengkalis Muriareza hariansyahNo ratings yet

- Business Plan Investors BankersDocument199 pagesBusiness Plan Investors BankersDJ-Raihan RatulNo ratings yet

- PrathyushaDocument17 pagesPrathyushaPolamada PrathyushaNo ratings yet

- A Report On WIndow DressingDocument6 pagesA Report On WIndow DressingsaumyabratadasNo ratings yet

- Is Mers in Your MortgageDocument9 pagesIs Mers in Your MortgageRicharnellia-RichieRichBattiest-Collins67% (3)

- Chap007-Practice SolutionDocument80 pagesChap007-Practice SolutionVũ Trần Nhật ViNo ratings yet

- Report of The Auditor-General On The Public Accounts of Ghana - Ministries, Departments and Other Agencies For The Year Ended 31 December 2021Document212 pagesReport of The Auditor-General On The Public Accounts of Ghana - Ministries, Departments and Other Agencies For The Year Ended 31 December 2021ogbarmey-tettey andyNo ratings yet

- Citibank - WikipediaDocument10 pagesCitibank - Wikipediasharin kulalNo ratings yet

- Financial Appraisal of ProjectDocument22 pagesFinancial Appraisal of ProjectMahmudur RahmanNo ratings yet

- Valuation - Multiples and EV Value DriversDocument27 pagesValuation - Multiples and EV Value DriversstrokemeNo ratings yet

- Chapter 2Document25 pagesChapter 2heobenicerNo ratings yet

- The Coal Mines (Nationalisation) Act, 1973Document65 pagesThe Coal Mines (Nationalisation) Act, 1973shashwat kumarNo ratings yet

- Dunlop India Limited 2012 PDFDocument10 pagesDunlop India Limited 2012 PDFdidwaniasNo ratings yet

- AFS 2016 - Towncall Rural Bank, Inc. Page 28 of 42Document3 pagesAFS 2016 - Towncall Rural Bank, Inc. Page 28 of 42Judith CastroNo ratings yet

- Estate Tax-Handout 2Document4 pagesEstate Tax-Handout 2Xerez SingsonNo ratings yet

- Ashi KhoriyaDocument18 pagesAshi KhoriyaAdarsh VermaNo ratings yet

- Daftar Pustaka: GOKMARIA SIMARMATA, Supriyadi, M.SC., PH.D., CMA., CA., AkDocument3 pagesDaftar Pustaka: GOKMARIA SIMARMATA, Supriyadi, M.SC., PH.D., CMA., CA., AkMuhammad WildanNo ratings yet

- Kims RLCO Trading System DescriptionDocument21 pagesKims RLCO Trading System DescriptionAmol b100% (2)

- Rencana TradingDocument17 pagesRencana TradingArya PuwentaNo ratings yet

- (CredTrans) 85 - Mahoney V TuasonDocument3 pages(CredTrans) 85 - Mahoney V TuasonALEC NICOLE PARAFINANo ratings yet

- RBF Exchane Control BrochureDocument24 pagesRBF Exchane Control BrochureRavineshNo ratings yet

- Methods of Project Financing: Project Finance Equity Finance The ProjectDocument9 pagesMethods of Project Financing: Project Finance Equity Finance The ProjectA vyasNo ratings yet

- Debt Management in Pakistan: Presented by Hira Wahla Saeed Ansari Atika Imtiaz Umair SiddiquiDocument38 pagesDebt Management in Pakistan: Presented by Hira Wahla Saeed Ansari Atika Imtiaz Umair Siddiquiumair_siddiqui89No ratings yet

- 2551Q LboDocument2 pages2551Q Lboava1234567890No ratings yet

- Forex Combo System.Document10 pagesForex Combo System.flathonNo ratings yet

- Signature of TestatorDocument2 pagesSignature of TestatorChaya NgNo ratings yet