You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Micro Economic Project ReportDocument43 pagesMicro Economic Project ReportJaneefarNo ratings yet

- Main Theories of FDIDocument22 pagesMain Theories of FDIThu TrangNo ratings yet

- The Ideological Dimension of GlobalizationDocument6 pagesThe Ideological Dimension of GlobalizationJulia May BalagNo ratings yet

- Ch28 Test Bank 4-5-10Document9 pagesCh28 Test Bank 4-5-10bluephoe100% (1)

- Group3 GroupResearchAssignmentDocument23 pagesGroup3 GroupResearchAssignmentGajulin, April JoyNo ratings yet

- China - The Banking SystemDocument3 pagesChina - The Banking Systemamitsonik100% (1)

- Economic Report On Indonesia 2017 PDFDocument280 pagesEconomic Report On Indonesia 2017 PDFWahyu Eko WidodoNo ratings yet

- 3 B Revision NotesDocument169 pages3 B Revision NotesAurelia KimNo ratings yet

- BEC1054 - Mid-Term (Take Home Test) - T1 - 20202021 (Q)Document6 pagesBEC1054 - Mid-Term (Take Home Test) - T1 - 20202021 (Q)Sweethaa ArumugamNo ratings yet

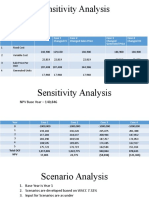

- Sensitivity Analysis & Scenario AnalysisDocument5 pagesSensitivity Analysis & Scenario AnalysisYasir RahimNo ratings yet

- 1 Definition of Economics: Chapter 1 What Is Economics?Document54 pages1 Definition of Economics: Chapter 1 What Is Economics?riham elnagarNo ratings yet

- Tsunamis To Long WavesDocument23 pagesTsunamis To Long WavesLoose0% (1)

- Stock Market CrashDocument15 pagesStock Market CrashsdaminctgNo ratings yet

- Scheela 2015 - Formal and Informal Venture Capital Investing in SEADocument21 pagesScheela 2015 - Formal and Informal Venture Capital Investing in SEAFaldi HarisNo ratings yet

- 21UBN2T441 - Financial Analytics Notes PDFDocument49 pages21UBN2T441 - Financial Analytics Notes PDFDeepakOjhaNo ratings yet

- Micro Chapter 6 ExerciseDocument13 pagesMicro Chapter 6 Exercisehuonglee273No ratings yet

- Valuing Impacts From Observed Behavior-Indirect Method - Asset ValuationDocument24 pagesValuing Impacts From Observed Behavior-Indirect Method - Asset ValuationJan Luziel MorenoNo ratings yet

- ECO135 HW7QuestionsDocument2 pagesECO135 HW7QuestionsAdvennie NuhujananNo ratings yet

- Variance Analysis WIKIPEDIA PDFDocument2 pagesVariance Analysis WIKIPEDIA PDFcaapromoNo ratings yet

- Chapter 2: Asset Classes and Financial Instruments: Problem SetsDocument6 pagesChapter 2: Asset Classes and Financial Instruments: Problem SetsBiloni KadakiaNo ratings yet

- Assignment - Doc-401 FIM - 24042016113313Document10 pagesAssignment - Doc-401 FIM - 24042016113313Ahmed RaajNo ratings yet

- CELL PHONES SUPPORT ECONOMIC DEVELOPMENT (Case Study)Document4 pagesCELL PHONES SUPPORT ECONOMIC DEVELOPMENT (Case Study)jan martinNo ratings yet

- Chapter ExercisesDocument17 pagesChapter ExercisesPaller Shery RoseNo ratings yet

- Part 5 - Chapter 33 Aggregate Demand and Aggregate SupplyDocument36 pagesPart 5 - Chapter 33 Aggregate Demand and Aggregate SupplyTHU DUONG MINHNo ratings yet

- Location Theory-Johann Von ThunenDocument17 pagesLocation Theory-Johann Von ThunenAlyssa ArricivitaNo ratings yet

- Purchasing Power Parity Theory and ExchaDocument24 pagesPurchasing Power Parity Theory and ExchaTharshiNo ratings yet

- What Is Variance AnalysisDocument10 pagesWhat Is Variance Analysismujuni brianmjuNo ratings yet

- A Brief HistoryDocument3 pagesA Brief HistoryRazor11111No ratings yet

- Sociology, Psychology and The Study of EducationDocument23 pagesSociology, Psychology and The Study of Educationprojecttrans transNo ratings yet

- The Global Crisis and Vietnam's Policy Responses: LE Thi Thuy VanDocument12 pagesThe Global Crisis and Vietnam's Policy Responses: LE Thi Thuy VanAly NguyễnNo ratings yet