You might also like

- Hype Cycle For Healthcare ProviderDocument36 pagesHype Cycle For Healthcare Providershenero1No ratings yet

- Venture Capital ReportDocument28 pagesVenture Capital ReportStarlettTVNo ratings yet

- Forrester Requirements ManagementDocument12 pagesForrester Requirements ManagementMudit KapoorNo ratings yet

- Zendesk Benchmark Report 2014Document18 pagesZendesk Benchmark Report 2014Eduardo RodriguesNo ratings yet

- Advanced Analytics for Government The Ultimate Step-By-Step GuideFrom EverandAdvanced Analytics for Government The Ultimate Step-By-Step GuideNo ratings yet

- Business Intelligence in Health Care IndustryDocument2 pagesBusiness Intelligence in Health Care IndustrysasiarchieNo ratings yet

- Drive Your Business With Predictive AnalyticsDocument10 pagesDrive Your Business With Predictive Analyticsyoungwarrior888100% (1)

- Virtualization Pharma BR 1638314 PDFDocument24 pagesVirtualization Pharma BR 1638314 PDFParth DesaiNo ratings yet

- The Practice of Predictive Analytics in Healthcare - by Gopalakrishna PalemDocument27 pagesThe Practice of Predictive Analytics in Healthcare - by Gopalakrishna PalemGopalakrishna Palem100% (1)

- Forrester AgileDocument18 pagesForrester AgileVeaceslav SerghiencoNo ratings yet

- 2021-10 COCIR - MTE Interoperability Standards in Digital HealthDocument29 pages2021-10 COCIR - MTE Interoperability Standards in Digital HealthdickyNo ratings yet

- Intelligent Document Processing (IDP) - Technology Vendor Landscape With Products PEAK Matrix™ Assessment 2019Document78 pagesIntelligent Document Processing (IDP) - Technology Vendor Landscape With Products PEAK Matrix™ Assessment 2019Vigneshwar A SNo ratings yet

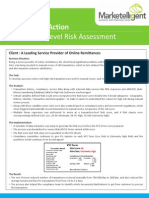

- Analytics in Action - How Marketelligent Helped An Online Remittance Firm Identify Risky TransactionsDocument2 pagesAnalytics in Action - How Marketelligent Helped An Online Remittance Firm Identify Risky TransactionsMarketelligentNo ratings yet

- CB Insights - Digital Health Report 2021Document186 pagesCB Insights - Digital Health Report 2021Suketu KotichaNo ratings yet

- Analytics in Action - How Marketelligent Helped A CPG Company Boost Store Order ValueDocument2 pagesAnalytics in Action - How Marketelligent Helped A CPG Company Boost Store Order ValueMarketelligentNo ratings yet

- Data MonetizationDocument3 pagesData MonetizationmohnishNo ratings yet

- Medtech in Asia Committing at Scale To Raise Standards of Care For Patients PDFDocument49 pagesMedtech in Asia Committing at Scale To Raise Standards of Care For Patients PDFKunalNo ratings yet

- OriginalDocument23 pagesOriginalNireasNo ratings yet

- Business Analytics IntroductionDocument37 pagesBusiness Analytics IntroductionTejash GannabattulaNo ratings yet

- Data Digitization and DisruptionDocument18 pagesData Digitization and DisruptionSimpleLuNo ratings yet

- The Forrester Wave-Master Data Management Solutions, Q1 2014Document17 pagesThe Forrester Wave-Master Data Management Solutions, Q1 2014Pallavi ReddyNo ratings yet

- (Dr. Kim) Data Analytics-Inroduction (KDS)Document51 pages(Dr. Kim) Data Analytics-Inroduction (KDS)Kimthan ChhoeurngNo ratings yet

- Big Data: New Insights Transform Industries: White PaperDocument12 pagesBig Data: New Insights Transform Industries: White PaperKishalay DattaNo ratings yet

- Process Discovery Part 2Document32 pagesProcess Discovery Part 2Rahul AryanNo ratings yet

- Operations Management - BenchmarkingDocument22 pagesOperations Management - BenchmarkingPeter Kowalski KNo ratings yet

- Blockchain ResearchDocument20 pagesBlockchain ResearchusoroukNo ratings yet

- Analytics in Action - How Marketelligent Helped A Quick Service Restaurant Chain Identify Customer Pain PointsDocument2 pagesAnalytics in Action - How Marketelligent Helped A Quick Service Restaurant Chain Identify Customer Pain PointsMarketelligentNo ratings yet

- Analytics in Action - How Marketelligent Helped Increase Customer Engagement Via Targeted Cross-SellDocument2 pagesAnalytics in Action - How Marketelligent Helped Increase Customer Engagement Via Targeted Cross-SellMarketelligentNo ratings yet

- Real Analytics: Shifting From Business Hindsight To Insight To ForesightDocument6 pagesReal Analytics: Shifting From Business Hindsight To Insight To ForesightDeloitte AnalyticsNo ratings yet

- Ib Business Management Full GlossaryDocument24 pagesIb Business Management Full Glossaryevangelinebai8No ratings yet

- Data Driven Healthcare For PayersDocument24 pagesData Driven Healthcare For PayersLinda WatsonNo ratings yet

- Fractal Analytics - Corporate ReportDocument2 pagesFractal Analytics - Corporate ReportShashi BhagnariNo ratings yet

- Innovations in MDM Implementation: Success Via A Boxed ApproachDocument4 pagesInnovations in MDM Implementation: Success Via A Boxed ApproachCognizantNo ratings yet

- Time Series Analysis in Spark SQLDocument5 pagesTime Series Analysis in Spark SQLJP VijaykumarNo ratings yet

- Healthcare Report Q1 2021Document75 pagesHealthcare Report Q1 2021Venkatraman KrishnamoorthyNo ratings yet

- Assignment - 2 AIT580: Shravan Chintha G01064991 Big DataDocument5 pagesAssignment - 2 AIT580: Shravan Chintha G01064991 Big DataMulya ShreeNo ratings yet

- Sample Operations Academy Brochure (3414)Document10 pagesSample Operations Academy Brochure (3414)01dynamicNo ratings yet

- Global Hydrogen Peroxide Market - Growth, Trends and Forecasts 2018 - 2023Document187 pagesGlobal Hydrogen Peroxide Market - Growth, Trends and Forecasts 2018 - 2023Khiết NguyênNo ratings yet

- Data-Driven Healthcare Organizations Use Big Data Analytics For Big GainsDocument8 pagesData-Driven Healthcare Organizations Use Big Data Analytics For Big GainsHandsome RobNo ratings yet

- Advisory Board Womens Health Strategic Plan TemplateFinal MPLCDocument63 pagesAdvisory Board Womens Health Strategic Plan TemplateFinal MPLCKang DjoenNo ratings yet

- Monte Carlo MethodDocument23 pagesMonte Carlo MethodCHINGZU212No ratings yet

- WP Impact of Strategic Simulation On Product ProfitabilityDocument6 pagesWP Impact of Strategic Simulation On Product ProfitabilitymcruzalvNo ratings yet

- SAP Global Batch TracebilityDocument55 pagesSAP Global Batch Tracebilityshai_m1No ratings yet

- List of Analytics Consulting Companies in IndiaDocument3 pagesList of Analytics Consulting Companies in IndiaAmardeep KaushalNo ratings yet

- PHD CSE Seminar in Course WorkDocument17 pagesPHD CSE Seminar in Course Workkumarajay7th0% (1)

- Twenty Ways To Split Agile Stories PDFDocument1 pageTwenty Ways To Split Agile Stories PDFBarry Gian JamesNo ratings yet

- Analytics in Action - How Marketelligent Helped A B2B Retailer Increase Its Lead VelocityDocument2 pagesAnalytics in Action - How Marketelligent Helped A B2B Retailer Increase Its Lead VelocityMarketelligentNo ratings yet

- Analytics in Action - How Marketelligent Helped A Retailer Rationalize SKU'sDocument2 pagesAnalytics in Action - How Marketelligent Helped A Retailer Rationalize SKU'sMarketelligentNo ratings yet

- Business Foundation Capstone Framework For Analysis: CycleDocument36 pagesBusiness Foundation Capstone Framework For Analysis: CycleclugufriprNo ratings yet

- Purdue Data Science Master Program - v5Document30 pagesPurdue Data Science Master Program - v5Subramani SivakumarNo ratings yet

- CB Insights AI 100 Trends WebinarDocument34 pagesCB Insights AI 100 Trends WebinarYannick Martineau GoupilNo ratings yet

- Bi SopDocument2 pagesBi SopMuhd AfiqNo ratings yet

- People Analytics 3Document6 pagesPeople Analytics 3contactchintanNo ratings yet

- CC Fraud Analytics CapstoneDocument10 pagesCC Fraud Analytics CapstoneRohit VoraNo ratings yet

- Profit From Your Forecasting Software: A Best Practice Guide for Sales ForecastersFrom EverandProfit From Your Forecasting Software: A Best Practice Guide for Sales ForecastersNo ratings yet

- IT Infrastructure Deployment A Complete Guide - 2020 EditionFrom EverandIT Infrastructure Deployment A Complete Guide - 2020 EditionNo ratings yet

- Complaint Challenging Site Neutral Payment Policy181204Document22 pagesComplaint Challenging Site Neutral Payment Policy181204Jesse MajorNo ratings yet

- Fifth Circuit Obamacare RulingDocument98 pagesFifth Circuit Obamacare RulingLaw&CrimeNo ratings yet

- ACA Lawsuit Put On Hold Over Government ShutdownDocument3 pagesACA Lawsuit Put On Hold Over Government ShutdownHLMeditNo ratings yet

- House Motion To Intervene in ACA Lawsuit, Fifth CircuitDocument33 pagesHouse Motion To Intervene in ACA Lawsuit, Fifth CircuitHLMeditNo ratings yet

- Texas. Et Al v. U.S. Et Al OpinionDocument55 pagesTexas. Et Al v. U.S. Et Al OpinionDoug MataconisNo ratings yet

- DOJ Argues Entire ACA Should Fall in Fifth Circuit Brief - May 2019Document75 pagesDOJ Argues Entire ACA Should Fall in Fifth Circuit Brief - May 2019HLMeditNo ratings yet

- OSF HealthCare Prevails in Dispute Over Church PlanDocument16 pagesOSF HealthCare Prevails in Dispute Over Church PlanHLMeditNo ratings yet

- Intermountain To Seek Writ SCOTUSDocument9 pagesIntermountain To Seek Writ SCOTUSHLMedit100% (1)

- Reforming America's Healthcare System Through Choice and CompetitionDocument119 pagesReforming America's Healthcare System Through Choice and CompetitionHLMeditNo ratings yet

- Jury Awards $50M in NorthShore Health Malpractice SuitDocument23 pagesJury Awards $50M in NorthShore Health Malpractice SuitHLMeditNo ratings yet

- North Memorial Health Care Prevails On Appeal in EEOC-Backed SuitDocument18 pagesNorth Memorial Health Care Prevails On Appeal in EEOC-Backed SuitHLMeditNo ratings yet

- AMA Letter To DOJ Regarding CVS Aetna MergerDocument141 pagesAMA Letter To DOJ Regarding CVS Aetna MergerHLMedit100% (1)

- Maine Attorney General ACA Lawsuit 837384fb 1155 4ac6 Ad98 5f4c18fd2e4aDocument5 pagesMaine Attorney General ACA Lawsuit 837384fb 1155 4ac6 Ad98 5f4c18fd2e4aHLMeditNo ratings yet

- Lawsuit To Stipulate Terms of CVS-Aetna MergerDocument19 pagesLawsuit To Stipulate Terms of CVS-Aetna MergerHLMeditNo ratings yet

- Van Tatenhove Dismissal of Bevin LawsuitDocument12 pagesVan Tatenhove Dismissal of Bevin LawsuitInsider LouisvilleNo ratings yet

- Letter of Support For ACOs and MSSP NPRM Sign On 09202018Document3 pagesLetter of Support For ACOs and MSSP NPRM Sign On 09202018HLMeditNo ratings yet

- CHS Subsidiary HMA Reaches $260 Million Settlement Over Billing PracticesDocument68 pagesCHS Subsidiary HMA Reaches $260 Million Settlement Over Billing PracticesHLMeditNo ratings yet

- Next Generation ACOs - First Annual ReportDocument2 pagesNext Generation ACOs - First Annual ReportHLMeditNo ratings yet

- UnitedHealth Wins Medicare Overpayment Rule CaseDocument30 pagesUnitedHealth Wins Medicare Overpayment Rule CaseHLMedit100% (1)

- Hospitals Sue HHS Over 340BDocument19 pagesHospitals Sue HHS Over 340BHLMeditNo ratings yet

- Arkansas Medicaid Work Requirement Faces Legal ChallengeDocument38 pagesArkansas Medicaid Work Requirement Faces Legal ChallengeHLMeditNo ratings yet

- Health Plan Files Another Risk-Adjustments LawsuitDocument68 pagesHealth Plan Files Another Risk-Adjustments LawsuitHLMeditNo ratings yet

- AHA Responds HHS Medicare Appeals BacklogDocument19 pagesAHA Responds HHS Medicare Appeals BacklogHLMeditNo ratings yet

- Maryland Sues To Head Off Texas-Led ACA ChallengeDocument34 pagesMaryland Sues To Head Off Texas-Led ACA ChallengeHLMeditNo ratings yet

- States Suing Trump Administration Over Association Health Plans Seek Quick WinDocument68 pagesStates Suing Trump Administration Over Association Health Plans Seek Quick WinHLMeditNo ratings yet

- Medicare To Eliminate Appeals Backlog Within 4 Years, HHS Tells JudgeDocument30 pagesMedicare To Eliminate Appeals Backlog Within 4 Years, HHS Tells JudgeHLMeditNo ratings yet

- Cigna Reiterates Support For Proposed Merger With Express ScriptsDocument9 pagesCigna Reiterates Support For Proposed Merger With Express ScriptsHLMeditNo ratings yet

- Stakeholders Urge Restart To ACA Risk-Adjustment PaymentsDocument4 pagesStakeholders Urge Restart To ACA Risk-Adjustment PaymentsHLMeditNo ratings yet

- Health Plan Accuses HHS of Risk-Adjustment CharadeDocument4 pagesHealth Plan Accuses HHS of Risk-Adjustment CharadeHLMeditNo ratings yet

- Cities Sue Trump Over ACA 'Sabotage'Document134 pagesCities Sue Trump Over ACA 'Sabotage'HLMeditNo ratings yet

- Class 9 and 11-ptm CircularDocument2 pagesClass 9 and 11-ptm CircularRishabh GargNo ratings yet

- FortiSASE-23.4-FortiGate NGFW To FortiSASE SPA Hub Conversion Deployment GuideDocument72 pagesFortiSASE-23.4-FortiGate NGFW To FortiSASE SPA Hub Conversion Deployment Guideliving4it.peNo ratings yet

- Hapter 11: © 2006 Prentice Hall Business Publishing Accounting Information Systems, 10/e Romney/SteinbartDocument86 pagesHapter 11: © 2006 Prentice Hall Business Publishing Accounting Information Systems, 10/e Romney/Steinbartarum NastitiNo ratings yet

- Research On The Relationship Between The Growth of OTT Service Market and The Change in The Structure of The Pay-TV MarketDocument49 pagesResearch On The Relationship Between The Growth of OTT Service Market and The Change in The Structure of The Pay-TV MarketPrathamesh DivekarNo ratings yet

- About AonDocument6 pagesAbout AonAmit ChauhanNo ratings yet

- New Customer Packet FormDocument8 pagesNew Customer Packet FormDark _No ratings yet

- Lic Pension PlusDocument10 pagesLic Pension PlustsrajanNo ratings yet

- Fasspay Merchant Application v20220728Document3 pagesFasspay Merchant Application v20220728dauswes0% (1)

- DSR Report 30 Jun 17..Document215 pagesDSR Report 30 Jun 17..Karuna MoorthiNo ratings yet

- Get Cheap Mexican Dedicated Hosting For Online BusinessDocument4 pagesGet Cheap Mexican Dedicated Hosting For Online Businessvaibhav sharmaNo ratings yet

- Chapter 1-QuizDocument27 pagesChapter 1-QuizJpzelle100% (1)

- Arabia Tech - Product PricingDocument40 pagesArabia Tech - Product PricingLechelaNo ratings yet

- Ramsey County District Court Cases Andert Tschida 1943 - 1958Document5 pagesRamsey County District Court Cases Andert Tschida 1943 - 1958api-327987435No ratings yet

- AdjustmentsDocument16 pagesAdjustmentsScouter SejatiNo ratings yet

- ? Optical Solutions For Mobile Transport Networks ?Document21 pages? Optical Solutions For Mobile Transport Networks ?munasheNo ratings yet

- Bedford Hospital NHS Trust: Examining The Management of The Inpatient Waiting ListDocument81 pagesBedford Hospital NHS Trust: Examining The Management of The Inpatient Waiting ListPeter LouisNo ratings yet

- Physical DistributionDocument2 pagesPhysical DistributionKeshav ShankarNo ratings yet

- Battleface IPID GBPDocument2 pagesBattleface IPID GBPmaria monsecaNo ratings yet

- To Resign or Serve?Document5 pagesTo Resign or Serve?RamadhanNo ratings yet

- Tax Invoice: Account No. 5742504365Document1 pageTax Invoice: Account No. 5742504365vishnuvarthanNo ratings yet

- TopicsDocument4 pagesTopicsAryadeep ChakrabortyNo ratings yet

- MidtermQ2 - Home Office Branch Accounting Billing Above CostDocument13 pagesMidtermQ2 - Home Office Branch Accounting Billing Above Costsarahbee100% (2)

- EOI - INSDAG Architecture Award Competition 2023Document1 pageEOI - INSDAG Architecture Award Competition 2023ebinhorrison sNo ratings yet

- Reliance Mutual Funds ProjectDocument58 pagesReliance Mutual Funds ProjectShivangi SinghNo ratings yet

- Bicycle Motorcycle Car/ Private Type Jeep Pedicab Tricycle Jeepney Multicab & RuscoDocument5 pagesBicycle Motorcycle Car/ Private Type Jeep Pedicab Tricycle Jeepney Multicab & Ruscokim suarezNo ratings yet

- Chapter 13: Basics of Commercial BankingDocument2 pagesChapter 13: Basics of Commercial BankingShane Tabunggao100% (1)

- 6 - Postal Glossary Part IIDocument55 pages6 - Postal Glossary Part IIUma MaheswararaoNo ratings yet

- Meal Mentor: Block A, Phase 2, Street 7, Johar Town, Lahore (042) - 4589000, +923334630878Document6 pagesMeal Mentor: Block A, Phase 2, Street 7, Johar Town, Lahore (042) - 4589000, +923334630878Nizra AwaisNo ratings yet

- IGP and EGPDocument11 pagesIGP and EGPEstelle MandengNo ratings yet

- DISCOVERING Ethiopia - Tourism Sector GuideDocument17 pagesDISCOVERING Ethiopia - Tourism Sector GuideMULUSEWNo ratings yet