You might also like

- XTO Energy Liquidity and Solvency AnalysisDocument6 pagesXTO Energy Liquidity and Solvency AnalysisCarneadesNo ratings yet

- Components of RNOA - Profit Margin and Asset TurnoverDocument3 pagesComponents of RNOA - Profit Margin and Asset TurnoverCarneadesNo ratings yet

- Net Operating Profit Margin (NOPM)Document1 pageNet Operating Profit Margin (NOPM)CarneadesNo ratings yet

- Earnings Quality Analysis - Operating Cash Flow To Net IncomeDocument3 pagesEarnings Quality Analysis - Operating Cash Flow To Net IncomeCarneadesNo ratings yet

- Basic V Diluted EPSDocument1 pageBasic V Diluted EPSCarneadesNo ratings yet

- Aetna Q2 09 Financial ResultsDocument14 pagesAetna Q2 09 Financial ResultsCarneadesNo ratings yet

- Bond Pricing 101Document3 pagesBond Pricing 101CarneadesNo ratings yet

- Vertical Analysis of Financial Statements - Pepsi V CokeDocument2 pagesVertical Analysis of Financial Statements - Pepsi V CokeCarneades33% (3)

- Introduction To Credit Risk Analysis: Debt To Equity RatioDocument3 pagesIntroduction To Credit Risk Analysis: Debt To Equity RatioCarneadesNo ratings yet

- OCF To Current LiabilitiesDocument1 pageOCF To Current LiabilitiesCarneadesNo ratings yet

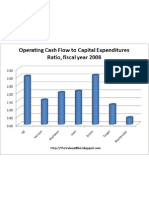

- OCF To CapexDocument1 pageOCF To CapexCarneadesNo ratings yet

- Housing Starts August 2009Document1 pageHousing Starts August 2009CarneadesNo ratings yet

- Duke Energy Allowances To ReceivablesDocument1 pageDuke Energy Allowances To ReceivablesCarneadesNo ratings yet

- Monthly CMBS Delinquency August 2009Document1 pageMonthly CMBS Delinquency August 2009CarneadesNo ratings yet

- Democrats and Out of State Campaign ContributionsDocument3 pagesDemocrats and Out of State Campaign ContributionsCarneadesNo ratings yet

- RealPoint CMBS Delinquency Report July 2009Document15 pagesRealPoint CMBS Delinquency Report July 2009Carneades100% (1)

- America's Healthy Future Act of 2009Document223 pagesAmerica's Healthy Future Act of 2009KFFHealthNewsNo ratings yet

- Semiconductor Data Through July 2009Document2 pagesSemiconductor Data Through July 2009CarneadesNo ratings yet

- The SEC's Role Regarding and Oversight of Nationally Recognized Statistical Rating OrganizationsDocument124 pagesThe SEC's Role Regarding and Oversight of Nationally Recognized Statistical Rating OrganizationsCarneadesNo ratings yet

- Prison Population As % of US Population 1980-2007Document1 pagePrison Population As % of US Population 1980-2007CarneadesNo ratings yet

- Social Security COLA History 1999-2009Document1 pageSocial Security COLA History 1999-2009CarneadesNo ratings yet

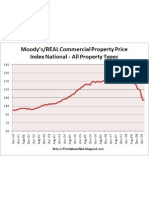

- Moodys CPPI August 2009Document1 pageMoodys CPPI August 2009CarneadesNo ratings yet

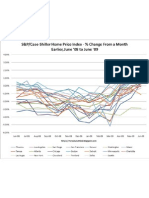

- SP/Case Shiller Index Through June 2009Document1 pageSP/Case Shiller Index Through June 2009CarneadesNo ratings yet

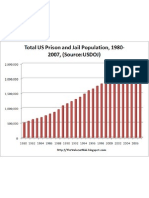

- US Prison Population 1980-2007Document1 pageUS Prison Population 1980-2007CarneadesNo ratings yet

- TIC Data June 2009Document1 pageTIC Data June 2009CarneadesNo ratings yet

- ENSYS Cap and Trade Briefing 8-20-09Document25 pagesENSYS Cap and Trade Briefing 8-20-09CarneadesNo ratings yet

- Medicare Modernization ActDocument416 pagesMedicare Modernization ActCarneadesNo ratings yet

- July 2009 Housing Starts 2005-PresentDocument1 pageJuly 2009 Housing Starts 2005-PresentCarneadesNo ratings yet

- July 2009 Housing Starts 1959-PresentDocument1 pageJuly 2009 Housing Starts 1959-PresentCarneadesNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Claudio and Lydia Reyes V CaDocument2 pagesClaudio and Lydia Reyes V CaJan Jason Guerrero LumanagNo ratings yet

- AkuntansiDocument46 pagesAkuntansiRo Untoro ToroNo ratings yet

- Royalty AccountsDocument5 pagesRoyalty AccountsRobert Henson100% (2)

- Quiz No 11Document12 pagesQuiz No 11xiadfreakyNo ratings yet

- ATP 107 Conveyancing Project C-16Document18 pagesATP 107 Conveyancing Project C-16Anthony KipropNo ratings yet

- Favis V City of BaguioDocument3 pagesFavis V City of BaguioGhreighz GalinatoNo ratings yet

- Manlift Lease AgreementDocument6 pagesManlift Lease AgreementChris OpubaNo ratings yet

- 12 English Core Impq WritingDocument55 pages12 English Core Impq WritingAshmita Nagpal33% (3)

- Leasing and Hire-PurchaseDocument30 pagesLeasing and Hire-PurchaseDileep SinghNo ratings yet

- Cheat Sheet Accounting For Sub Leases Under The New Lease Accounting Standard (NZ IFRS 16)Document4 pagesCheat Sheet Accounting For Sub Leases Under The New Lease Accounting Standard (NZ IFRS 16)MaissyNo ratings yet

- Review Economics Mankiw Chap 5, Chap 6, Chap 13Document47 pagesReview Economics Mankiw Chap 5, Chap 6, Chap 13Hà (NIIE) Võ Thị NgọcNo ratings yet

- Contract Lease Residential PropertyDocument3 pagesContract Lease Residential PropertyMetha Dawn Orolfo-OlivarNo ratings yet

- Instruction Book For The Pitch-Then-Plan Business Planning ProcessDocument26 pagesInstruction Book For The Pitch-Then-Plan Business Planning ProcessSai Chakradhar AravetiNo ratings yet

- Farm Costing and BudgetingDocument25 pagesFarm Costing and Budgetingfruitfulluft50% (2)

- Postpaid Bill 7710074295 DECDocument3 pagesPostpaid Bill 7710074295 DEConkarNo ratings yet

- Digest Sales 2Document4 pagesDigest Sales 2Christian ParadoNo ratings yet

- CONTRACT LEASEDocument5 pagesCONTRACT LEASEHe Ro50% (2)

- Name: Date: Financial Accounting and ReportingDocument3 pagesName: Date: Financial Accounting and ReportingLeizzamar BayadogNo ratings yet

- Bar 2018 - MlquDocument138 pagesBar 2018 - MlquTimmy GonzalesNo ratings yet

- Sale Agreement Between City of Kalamazoo and Developers For Lot 2Document29 pagesSale Agreement Between City of Kalamazoo and Developers For Lot 2Malachi BarrettNo ratings yet

- AP MPL Act 1965 SectionsDocument32 pagesAP MPL Act 1965 SectionsRaghu RamNo ratings yet

- Commercial Lease Letter of IntentDocument2 pagesCommercial Lease Letter of IntentNicolae FlorianNo ratings yet

- Rent Agreement Format MakaanIQDocument2 pagesRent Agreement Format MakaanIQJuzer NomaniNo ratings yet

- CH 15Document3 pagesCH 15vivienNo ratings yet

- Real Estate Types and Condominium ConceptsDocument18 pagesReal Estate Types and Condominium ConceptsApril Dacles Baldonado100% (1)

- A - Price List & Payment Plan - Boulevard Walk - 12-06-2019Document6 pagesA - Price List & Payment Plan - Boulevard Walk - 12-06-2019Nitin AgnihotriNo ratings yet

- Rent TerminationDocument5 pagesRent TerminationoluwaseunNo ratings yet

- Residential Tenancy Agreement: Standard FormDocument11 pagesResidential Tenancy Agreement: Standard FormKim Ling KuanNo ratings yet

- Connected Quizzing QuestionsDocument37 pagesConnected Quizzing QuestionsAnusha RamjattanNo ratings yet

- Terms and ConditionsDocument2 pagesTerms and Conditionsian1333No ratings yet