You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- PR - Icade Santé Purchased The Buildings of 7 Clinis Held by Capio SantéDocument1 pagePR - Icade Santé Purchased The Buildings of 7 Clinis Held by Capio SantéIcadeNo ratings yet

- PR - Icade Will Build The New TGV Station in MontpellierDocument2 pagesPR - Icade Will Build The New TGV Station in MontpellierIcadeNo ratings yet

- PR - Icade Signs Lease With The French Ministry of The InteriorDocument1 pagePR - Icade Signs Lease With The French Ministry of The InteriorIcadeNo ratings yet

- PR - Icade Signs A Substantial Lease Agreement On EQHODocument1 pagePR - Icade Signs A Substantial Lease Agreement On EQHOIcadeNo ratings yet

- PR - 2014 Half-Year Results Resilient Cash-Flows in A Still-Strained MarketDocument11 pagesPR - 2014 Half-Year Results Resilient Cash-Flows in A Still-Strained MarketIcadeNo ratings yet

- PR - Icade - Bond - Issue - VUKDocument1 pagePR - Icade - Bond - Issue - VUKIcadeNo ratings yet

- PR - Icade Santé Wins The Tender Bid Launched by Capio SantéDocument1 pagePR - Icade Santé Wins The Tender Bid Launched by Capio SantéIcadeNo ratings yet

- Half Year Financial Report - June 2014Document84 pagesHalf Year Financial Report - June 2014IcadeNo ratings yet

- PR - Icade Takes A Significant Step Towards Complete Withdrawal From GermanyDocument1 pagePR - Icade Takes A Significant Step Towards Complete Withdrawal From GermanyIcadeNo ratings yet

- PR - Icade Santé Acquires 3 ClinicsDocument1 pagePR - Icade Santé Acquires 3 ClinicsIcadeNo ratings yet

- PR - Icade - Q1 - 2014 ActivityDocument9 pagesPR - Icade - Q1 - 2014 ActivityIcadeNo ratings yet

- PR - EQHO: Icade and KPMG Sign A LeaseDocument1 pagePR - EQHO: Icade and KPMG Sign A LeaseIcadeNo ratings yet

- Icade Annual Report - Reference Document 2012Document368 pagesIcade Annual Report - Reference Document 2012IcadeNo ratings yet

- PR - Livraison - Parc - Zoologique - ParisDocument2 pagesPR - Livraison - Parc - Zoologique - ParisIcadeNo ratings yet

- PR - Résultats Annuels 2013Document54 pagesPR - Résultats Annuels 2013IcadeNo ratings yet

- PR - EpraDocument1 pagePR - EpraIcadeNo ratings yet

- PR - Icade Enters A New Chapter of Its History enDocument2 pagesPR - Icade Enters A New Chapter of Its History enIcadeNo ratings yet

- CP - Icade - NominationDocument1 pageCP - Icade - NominationIcadeNo ratings yet

- PR - Icade Will Construct A New "Bridge Building"Document1 pagePR - Icade Will Construct A New "Bridge Building"IcadeNo ratings yet

- PR - Icade Klepierre Odysseum VUKDocument2 pagesPR - Icade Klepierre Odysseum VUKIcadeNo ratings yet

- PR - Bond Issue - IcadeDocument1 pagePR - Bond Issue - IcadeIcadeNo ratings yet

- PR - Icade Merger - Buyout Offer Exception Granted PDFDocument1 pagePR - Icade Merger - Buyout Offer Exception Granted PDFIcadeNo ratings yet

- Presentation of The Half-Year Results 2013 Icade - VUKDocument76 pagesPresentation of The Half-Year Results 2013 Icade - VUKIcadeNo ratings yet

- RP - Icade Le BeauvaisisDocument1 pageRP - Icade Le BeauvaisisIcadeNo ratings yet

- PR - Update To The Icade Reference DocumentDocument1 pagePR - Update To The Icade Reference DocumentIcadeNo ratings yet

- PR - Icade Santé Acquires The Hôpital de La Loire in Saint EtienneDocument1 pagePR - Icade Santé Acquires The Hôpital de La Loire in Saint EtienneIcadeNo ratings yet

- PR - Merger of Silic Into Icade PDFDocument2 pagesPR - Merger of Silic Into Icade PDFIcadeNo ratings yet

- PR - Icades First Half Results 2013 PDFDocument63 pagesPR - Icades First Half Results 2013 PDFIcadeNo ratings yet

- PR Success of The Public Offer For Silic - Vuk PDFDocument2 pagesPR Success of The Public Offer For Silic - Vuk PDFIcadeNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- RREEF The Future Size of The Global Real Estate Market (2007)Document22 pagesRREEF The Future Size of The Global Real Estate Market (2007)mr_mrsNo ratings yet

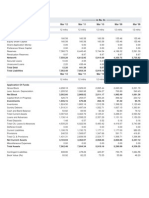

- Balance Sheet and P&L of CiplaDocument2 pagesBalance Sheet and P&L of CiplaPratik AhluwaliaNo ratings yet

- Mechanics of Futures Markets ExplainedDocument23 pagesMechanics of Futures Markets ExplainedaliNo ratings yet

- Far - First Preboard QuestionnaireDocument14 pagesFar - First Preboard QuestionnairewithyouidkNo ratings yet

- Sustainability 13 01933 v2Document15 pagesSustainability 13 01933 v2ronNo ratings yet

- Trendsetter Term SheetPPTDocument16 pagesTrendsetter Term SheetPPTMary Williams100% (2)

- Mining case nationality disputeDocument15 pagesMining case nationality disputeteryo expressNo ratings yet

- 101 Profit & Loss Type 1 BY 854×480@AsurReborn BotDocument7 pages101 Profit & Loss Type 1 BY 854×480@AsurReborn BotYash SharmaNo ratings yet

- Bloomberg Markets Magazine 2014-05.bakDocument130 pagesBloomberg Markets Magazine 2014-05.bakFeynman2014No ratings yet

- Conceptual QuestionsDocument5 pagesConceptual QuestionsSarwanti PurwandariNo ratings yet

- Corvex Capital - Restoring The Health To Commonwealth - 2013.02.26Document69 pagesCorvex Capital - Restoring The Health To Commonwealth - 2013.02.26Wall Street WanderlustNo ratings yet

- Paper 1 - Fundamentals of Securities and Futures RegulationDocument50 pagesPaper 1 - Fundamentals of Securities and Futures RegulationBogey Pretty100% (1)

- Homework 3: Pine Street Capital (Part I) : I Introduction and InstructionsDocument4 pagesHomework 3: Pine Street Capital (Part I) : I Introduction and Instructionslevan1225No ratings yet

- McDonald's Stock Clearly Benefits From Its Large Buybacks - Here Is Why (NYSE - MCD) - Seeking AlphaDocument12 pagesMcDonald's Stock Clearly Benefits From Its Large Buybacks - Here Is Why (NYSE - MCD) - Seeking AlphaWaleed TariqNo ratings yet

- 2 ACC5215 2020 M11 Associates and JV All SlidesDocument23 pages2 ACC5215 2020 M11 Associates and JV All SlidesDev GargNo ratings yet

- Soap Industry in Capital BudgetingDocument63 pagesSoap Industry in Capital BudgetingShivam Panday0% (1)

- Capital Budgeting Techniques for Investment EvaluationDocument5 pagesCapital Budgeting Techniques for Investment EvaluationUday Gowda0% (1)

- Questions Number One P LTD and Its Subsidiary Consolidated Income Statement For The Year Ended 31 December 2003Document29 pagesQuestions Number One P LTD and Its Subsidiary Consolidated Income Statement For The Year Ended 31 December 2003JOHN KAMANDANo ratings yet

- The Bankers Code Book PDFDocument202 pagesThe Bankers Code Book PDFOrdu Henry Onyebuchukwu100% (3)

- Direct Lenders First Real Test: Deloitte Alternative Lender Deal Tracker Spring 2020Document56 pagesDirect Lenders First Real Test: Deloitte Alternative Lender Deal Tracker Spring 2020fjdglf klfdNo ratings yet

- Audit of CFS Mind MapDocument1 pageAudit of CFS Mind Mapgovarthan1976No ratings yet

- Pricing Strategy: Midterm ExaminationDocument6 pagesPricing Strategy: Midterm ExaminationAndrea Jane M. BEDAÑONo ratings yet

- GL HOTELS LIMITED ("GL Hotels"/ "Target Company")Document1 pageGL HOTELS LIMITED ("GL Hotels"/ "Target Company")vridhiNo ratings yet

- Curso Forex Novato A Professional Más 60 Vídeos Explicativos PDFDocument5 pagesCurso Forex Novato A Professional Más 60 Vídeos Explicativos PDFLUISA SANCHEZNo ratings yet

- MIC ELECTRONICS LTD BUY OPPORTUNITYDocument17 pagesMIC ELECTRONICS LTD BUY OPPORTUNITYSudipta BoseNo ratings yet

- OTC Exchange of IndiaDocument17 pagesOTC Exchange of IndiaJigar_Dedhia_8946No ratings yet

- Problems On PPEDocument1 pageProblems On PPEimrul kaishNo ratings yet

- Post Qualification FormDocument25 pagesPost Qualification FormLalit Trivedi100% (1)

- TA112. BQA F.L Solution CMA September 2022 Exam.Document6 pagesTA112. BQA F.L Solution CMA September 2022 Exam.Mohammed Javed UddinNo ratings yet

- Virginia Key Marina RFP No 12-14-077 Presentation PDFDocument54 pagesVirginia Key Marina RFP No 12-14-077 Presentation PDFal_crespoNo ratings yet