You might also like

- L2-Probas-enoncé-TD 3Document2 pagesL2-Probas-enoncé-TD 3Widen EL KANDOUSSiNo ratings yet

- Aps U6 Test Review 2016 KeyDocument4 pagesAps U6 Test Review 2016 Keynuoti guanNo ratings yet

- 12 Practice FinalDocument7 pages12 Practice FinalsaiNo ratings yet

- Problem set seven beta distributions probabilitiesDocument4 pagesProblem set seven beta distributions probabilitiesNaty Dasilva Jr.No ratings yet

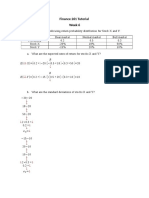

- Finance 261 Portfolio Standard DeviationDocument4 pagesFinance 261 Portfolio Standard DeviationManuel BoahenNo ratings yet

- Random Variable 2Document25 pagesRandom Variable 2KuldeepPaudelNo ratings yet

- Stat 330 Homework 4 Solution Probability Mass Functions Expected Values VariancesDocument3 pagesStat 330 Homework 4 Solution Probability Mass Functions Expected Values VariancesPei JingNo ratings yet

- Microeconomics–Final exam questions on pricing strategies, game theory, duopoly markets, common resource dilemma, and worker incentive schemesDocument3 pagesMicroeconomics–Final exam questions on pricing strategies, game theory, duopoly markets, common resource dilemma, and worker incentive schemesAnu AmruthNo ratings yet

- BRAC University, Spring 2011Document22 pagesBRAC University, Spring 2011Ratul RaihanNo ratings yet

- HW 1Document3 pagesHW 1Hande ÖzerNo ratings yet

- Homework 1Document5 pagesHomework 1Ashok ThiruvengadamNo ratings yet

- MidtermOR2 2021Document7 pagesMidtermOR2 2021Ân VõNo ratings yet

- Final Homework, Due May 3 (Returned May 8) :: F X e XDocument2 pagesFinal Homework, Due May 3 (Returned May 8) :: F X e XYusuf HusseinNo ratings yet

- 02 2 디지털논리 Boolean algebra2Document17 pages02 2 디지털논리 Boolean algebra2오현진No ratings yet

- Decisions Under UncertaintyDocument23 pagesDecisions Under UncertaintyfefahimNo ratings yet

- Homework 1 Outline of SolutionsDocument7 pagesHomework 1 Outline of SolutionsJeff SchulthiesNo ratings yet

- Quantum Relaxations Close Gaps in Classical CSPsDocument43 pagesQuantum Relaxations Close Gaps in Classical CSPsKevin MondragonNo ratings yet

- Test 6 and 7B AP Statistics Name:: Y - 1 0 1 2 - P (Y) 3C 2C 0.4 0.1Document5 pagesTest 6 and 7B AP Statistics Name:: Y - 1 0 1 2 - P (Y) 3C 2C 0.4 0.1Elizabeth CNo ratings yet

- Behavioral Finance - Tutorial2Document4 pagesBehavioral Finance - Tutorial2imran_omiNo ratings yet

- Cov corellationDocument4 pagesCov corellation8918.stkabirdinNo ratings yet

- Prac Test 1 - Quant MethodsDocument22 pagesPrac Test 1 - Quant MethodsryanNo ratings yet

- BIVARIATE DISTRIBUTION HOMEWORKDocument4 pagesBIVARIATE DISTRIBUTION HOMEWORKNigar QurbanovaNo ratings yet

- 1187w01 Prex3Document2 pages1187w01 Prex3Nguyen Manh TuanNo ratings yet

- Introduction To Probability Tutorial 6 Weeks 7Document2 pagesIntroduction To Probability Tutorial 6 Weeks 7Phan NhưNo ratings yet

- Statistics and Probability: Quarter 3 - Week 2.1Document18 pagesStatistics and Probability: Quarter 3 - Week 2.1Any AnimeNo ratings yet

- Problem Set 1Document3 pagesProblem Set 1Rahul JoshiNo ratings yet

- Introduction to Two-Dimensional Random VariablesDocument23 pagesIntroduction to Two-Dimensional Random VariablesOnetwothree TubeNo ratings yet

- Introduction to Probability TutorialDocument4 pagesIntroduction to Probability TutorialBach Tran HuuNo ratings yet

- HW 1Document3 pagesHW 1Vera Kristanti PurbaNo ratings yet

- PT - Practice Assignment 2 (With Solutions)Document7 pagesPT - Practice Assignment 2 (With Solutions)Vishnu BhanderiNo ratings yet

- Mva CapmDocument27 pagesMva Capmjc820809No ratings yet

- Assignment 1: Joint Probability DistributionDocument3 pagesAssignment 1: Joint Probability Distributionshrutika pathakNo ratings yet

- Carnival Game PaperDocument16 pagesCarnival Game Paperapi-352669460No ratings yet

- 4 PDFDocument17 pages4 PDFBadrulNo ratings yet

- Stat2 2020 - Practice ExamDocument26 pagesStat2 2020 - Practice ExamSeptian Nendra SaidNo ratings yet

- Homework 3 SolutionsDocument9 pagesHomework 3 SolutionsMaya SaraviaNo ratings yet

- Problem Set 3Document2 pagesProblem Set 3Nitin KumarNo ratings yet

- Tutorial 1Document3 pagesTutorial 1Yin Tung ChanNo ratings yet

- Lecture 3Document25 pagesLecture 3api-3729886No ratings yet

- UCLA Statistics Practice ProblemsDocument2 pagesUCLA Statistics Practice ProblemsJeeferson LopezNo ratings yet

- Random: VariableDocument43 pagesRandom: VariableNikko BautistaNo ratings yet

- Problem1 PDFDocument3 pagesProblem1 PDFCami Arce DerpićNo ratings yet

- Answer Set 1 - Fall 2008Document6 pagesAnswer Set 1 - Fall 2008Linh ChiNo ratings yet

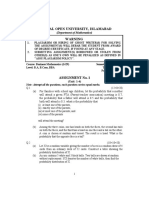

- Allama Iqbal Open University, Islamabad Warning: (Department of Mathematics)Document6 pagesAllama Iqbal Open University, Islamabad Warning: (Department of Mathematics)Arisha KhanNo ratings yet

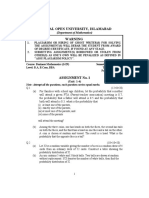

- Allama Iqbal Open University, Islamabad Warning: (Department of Mathematics)Document6 pagesAllama Iqbal Open University, Islamabad Warning: (Department of Mathematics)Javid ShahNo ratings yet

- Artificial Intelligence: Utility Theory Chapter 16, AIMADocument20 pagesArtificial Intelligence: Utility Theory Chapter 16, AIMArishabhNo ratings yet

- Random Variable: The Term Random Variable Is Widely Used in Statistics. A PracticalDocument32 pagesRandom Variable: The Term Random Variable Is Widely Used in Statistics. A PracticalRaviNo ratings yet

- ag1Document30 pagesag1Soumi MaityNo ratings yet

- EE5143 Tutorial1Document5 pagesEE5143 Tutorial1Sayan Rudra PalNo ratings yet

- 2.4 the Binomial Distribution 習題Document5 pages2.4 the Binomial Distribution 習題sandywu930510No ratings yet

- DT3 Homework 2Document1 pageDT3 Homework 2whatever0% (1)

- Molave Vocational Technical School Statistics WorksheetDocument5 pagesMolave Vocational Technical School Statistics WorksheetDypsy Pearl A. Pantinople0% (1)

- Quiz6 Ch05 PDFDocument5 pagesQuiz6 Ch05 PDFEarthy Dream TheNo ratings yet

- Module 0092: Boolean Expression MinimizationDocument5 pagesModule 0092: Boolean Expression Minimizationmohiuddin_vuNo ratings yet

- QF2104 Tutorial - Assignment 5 (Discussion Q4 II Rephased)Document3 pagesQF2104 Tutorial - Assignment 5 (Discussion Q4 II Rephased)igndunnoNo ratings yet

- De Moiver's Theorem (Trigonometry) Mathematics Question BankFrom EverandDe Moiver's Theorem (Trigonometry) Mathematics Question BankNo ratings yet

- E120 Fall14 HW1Document2 pagesE120 Fall14 HW1kimball_536238392No ratings yet

- E120 FALL14 HW4SolsDocument2 pagesE120 FALL14 HW4Solskimball_536238392No ratings yet

- E120 FALL14 HW3SolsDocument2 pagesE120 FALL14 HW3Solskimball_536238392No ratings yet

- E120 Fall14 HW3Document2 pagesE120 Fall14 HW3kimball_536238392No ratings yet

- E120 Fall14 HW4Document2 pagesE120 Fall14 HW4Taskin KhanNo ratings yet

- E120 FALL14 HW7SolsDocument2 pagesE120 FALL14 HW7Solskimball_536238392No ratings yet

- E120 Fall14 HW10Document1 pageE120 Fall14 HW10kimball_536238392No ratings yet

- E120 Fall14 HW2Document2 pagesE120 Fall14 HW2kimball_536238392No ratings yet

- E120 FALL14 HW9SolsDocument2 pagesE120 FALL14 HW9Solskimball_536238392No ratings yet

- E120 FALL14 HW8SolsDocument4 pagesE120 FALL14 HW8Solskimball_536238392No ratings yet

- E120 FALL14 HW2SolsDocument3 pagesE120 FALL14 HW2Solskimball_536238392No ratings yet

- E120 FALL14 HW1SolsDocument2 pagesE120 FALL14 HW1Solskimball_536238392No ratings yet

- E120 FALL14 HW10SolsDocument2 pagesE120 FALL14 HW10Solskimball_536238392No ratings yet

- E120 Fall14 HW7Document2 pagesE120 Fall14 HW7kimball_536238392No ratings yet

- E120 Fall14 HW9Document2 pagesE120 Fall14 HW9kimball_536238392No ratings yet

- E120 Fall14 HW5Document2 pagesE120 Fall14 HW5kimball_536238392No ratings yet

- E120 Fall14 HW6Document2 pagesE120 Fall14 HW6kimball_536238392No ratings yet

- E120 FALL14 HW6SolsDocument2 pagesE120 FALL14 HW6Solskimball_536238392No ratings yet

- E120 FALL14 HW5SolsDocument3 pagesE120 FALL14 HW5Solskimball_536238392No ratings yet