You might also like

- Fachwirt Videos YOUTUBE IHKSchwabenDocument5 pagesFachwirt Videos YOUTUBE IHKSchwabenFlaviub23No ratings yet

- Game of LifeDocument51 pagesGame of LifeFlaviub23No ratings yet

- Resurse Online de MatematicaDocument3 pagesResurse Online de MatematicaFlaviub23No ratings yet

- Sae EbookDocument264 pagesSae EbookFlaviub23No ratings yet

- As A Man Thinketh: by James AllenDocument22 pagesAs A Man Thinketh: by James AllenFlaviub23No ratings yet

- A Special GiftDocument106 pagesA Special GiftFlaviub23No ratings yet

- Road Signs 1Document11 pagesRoad Signs 1Flaviub23No ratings yet

- MFSCDocument28 pagesMFSCFlaviub23No ratings yet

- Remembrance Karen WrightDocument52 pagesRemembrance Karen WrightFlaviub23No ratings yet

- WTGH SampleChapterDocument12 pagesWTGH SampleChapterFlaviub23No ratings yet

- A Big Picture E-BookDocument35 pagesA Big Picture E-BookFlaviub23No ratings yet

- Creating The Value of LifeDocument155 pagesCreating The Value of LifeFlaviub23No ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Treynor RatioDocument1 pageTreynor Ratiosana_sr_96No ratings yet

- MGT201 Finalterm GoldenFileDocument230 pagesMGT201 Finalterm GoldenFilemaryamNo ratings yet

- A Plan With The Potential To Maximise Your Returns and Your DreamsDocument37 pagesA Plan With The Potential To Maximise Your Returns and Your DreamssaanjliNo ratings yet

- FINA1904 - ALL Weitzel - Spring 2019Document11 pagesFINA1904 - ALL Weitzel - Spring 2019JamesNo ratings yet

- Ias 16Document33 pagesIas 16Kiri chris100% (1)

- Countif Sumif ExercisesDocument24 pagesCountif Sumif Exercisessatya jitendraNo ratings yet

- Momo Statement ReportDocument2 pagesMomo Statement ReportHolybabyNo ratings yet

- Solution 786526Document38 pagesSolution 786526Anvesha AgarwalNo ratings yet

- Cash Flow StatementDocument11 pagesCash Flow StatementJonathanKelly Bitonga BargasoNo ratings yet

- P1 Investment Appraisal MethodsDocument3 pagesP1 Investment Appraisal MethodsSadeep Madhushan0% (1)

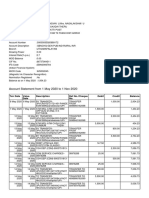

- Account Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument9 pagesAccount Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChellapandiNo ratings yet

- Sample MCQsDocument6 pagesSample MCQsRubal GargNo ratings yet

- Chapter 11 Performance Measurement in Decentralized OrganizationsDocument28 pagesChapter 11 Performance Measurement in Decentralized OrganizationsMariam MahmoudNo ratings yet

- Financial Risk SystemDocument2 pagesFinancial Risk SystembezbraNo ratings yet

- Bus 5111: Financial Management: Written Assignment Unit 1 Ratios CalculationDocument5 pagesBus 5111: Financial Management: Written Assignment Unit 1 Ratios CalculationCharles IrikefeNo ratings yet

- F Wall Street PDFDocument2 pagesF Wall Street PDFGuyNo ratings yet

- Theodore E. Raiford - Mathematics of FinanceDocument500 pagesTheodore E. Raiford - Mathematics of FinanceHeru HermawanNo ratings yet

- HDFC Bank Millennia Credit Card: Inspired Living, Ready For YouDocument3 pagesHDFC Bank Millennia Credit Card: Inspired Living, Ready For YouPratik AgarwalNo ratings yet

- 2022 Victor Tamayo YourDocument9 pages2022 Victor Tamayo YourCiber 13100% (3)

- Health Development Corporation Spread Sheet (Sol)Document8 pagesHealth Development Corporation Spread Sheet (Sol)Surya Kant100% (2)

- Bank of BarodaDocument99 pagesBank of BarodaYash Parekh100% (2)

- UntitledDocument6 pagesUntitledB - Clores, Mark RyanNo ratings yet

- Macro BookDocument237 pagesMacro BookcorishcaNo ratings yet

- Ticket Plus實名制購票流程 2023061301Document14 pagesTicket Plus實名制購票流程 2023061301daniel111478No ratings yet

- Chapter 8Document7 pagesChapter 8Yenelyn Apistar CambarijanNo ratings yet

- University of Lagos: School of Postgraduate StudiesDocument17 pagesUniversity of Lagos: School of Postgraduate StudiesAguda Henry OluwasegunNo ratings yet

- Challan Format (Specialist)Document1 pageChallan Format (Specialist)hgfvhgNo ratings yet

- Dtaa AnnexureDocument4 pagesDtaa AnnexureAkansha SharmaNo ratings yet

- Working Capital Management AssignmentDocument10 pagesWorking Capital Management AssignmentRitesh Singh RathoreNo ratings yet

- Neighborhood 3 B29 L19Document4 pagesNeighborhood 3 B29 L19Kate CastañaresNo ratings yet