You might also like

- Profit & Loss Statement: O' Lites GymDocument8 pagesProfit & Loss Statement: O' Lites GymNoorulain Adnan100% (5)

- 2014 Volume 2 CH 2 AnswersDocument15 pages2014 Volume 2 CH 2 AnswersJames Louis B. AntonioNo ratings yet

- Answers - Chapter 2 Vol 2 2009Document13 pagesAnswers - Chapter 2 Vol 2 2009Crystin Marie Tiu100% (1)

- PROSIELCODocument1 pagePROSIELCOnarras11No ratings yet

- 7 Quiz Bonds Payable & Note Payable - Part 1: 1 1 PT 2 PTDocument5 pages7 Quiz Bonds Payable & Note Payable - Part 1: 1 1 PT 2 PTJessa Mae BanseNo ratings yet

- Albay Electric Cooperative, Inc. (Aleco) : 2017 Budget Utilization ReportDocument12 pagesAlbay Electric Cooperative, Inc. (Aleco) : 2017 Budget Utilization ReportEdsel Alfred OtaoNo ratings yet

- Aud PWDocument16 pagesAud PWJikaNo ratings yet

- Quiz 2Document6 pagesQuiz 2GwynethNo ratings yet

- 02 FAR02-answersDocument18 pages02 FAR02-answersBea GarciaNo ratings yet

- ProjectionDocument3 pagesProjectionPrabhu SNo ratings yet

- Pradeep ProfitDocument9 pagesPradeep ProfitPradeep TiwariNo ratings yet

- Balance Sheet of HDFC STANDARD LIFE As at March 31 For Five YearsDocument7 pagesBalance Sheet of HDFC STANDARD LIFE As at March 31 For Five YearsNagendra PrasadNo ratings yet

- Mayor's Office Budget January 1, 2012 - September 30, 2012Document4 pagesMayor's Office Budget January 1, 2012 - September 30, 2012dlebrayNo ratings yet

- Answers - Chapter 2 Vol 2 RvsedDocument13 pagesAnswers - Chapter 2 Vol 2 Rvsedjamflox100% (3)

- Black Hole Futsal & Café: Schedule 1-11 Referred To Above Form An Integral Part of The Financial StatementDocument9 pagesBlack Hole Futsal & Café: Schedule 1-11 Referred To Above Form An Integral Part of The Financial Statementkalpana BaralNo ratings yet

- Project Report PDFDocument13 pagesProject Report PDFMan KumaNo ratings yet

- Fin 254 Group Project ExcelDocument12 pagesFin 254 Group Project Excelapi-422062723No ratings yet

- Mayor's Office Budget: January 2013 - August 2013Document4 pagesMayor's Office Budget: January 2013 - August 2013dlebrayNo ratings yet

- Final Projected AccountsDocument29 pagesFinal Projected Accountsjunaid buttNo ratings yet

- JMA 2021 BudgetDocument8 pagesJMA 2021 BudgetJerryJoshuaDiazNo ratings yet

- EXAM SOLUTIONS May - June 2020 Suggested SolutionsDocument6 pagesEXAM SOLUTIONS May - June 2020 Suggested SolutionsphumeleleNo ratings yet

- Company Financial StatementsDocument3 pagesCompany Financial StatementsNarasimha Jammigumpula0% (1)

- Balance Sheet of WiproDocument3 pagesBalance Sheet of WiproRinni JainNo ratings yet

- NCC Bank RatiosDocument20 pagesNCC Bank RatiosRahnoma Bilkis NavaidNo ratings yet

- Balance Sheet For 2009 & 2008: Assets 2009 (Nu.) 2008 (Nu.)Document3 pagesBalance Sheet For 2009 & 2008: Assets 2009 (Nu.) 2008 (Nu.)Singye SherubNo ratings yet

- LeverageDocument12 pagesLeverageprathamrastogi10No ratings yet

- Break Even AnalysisDocument13 pagesBreak Even Analysisprathamrastogi10No ratings yet

- ACCT105 Quizzes and SolutionsDocument8 pagesACCT105 Quizzes and SolutionsAway To PonderNo ratings yet

- SSBPloanDocument6 pagesSSBPloanSyahmi Samsudin100% (1)

- Balance Sheet TATA STEELDocument1 pageBalance Sheet TATA STEELJanak VaghasiaNo ratings yet

- Nations Trust Bank PLC and Its Subsidiaries: Company Number PQ 118Document19 pagesNations Trust Bank PLC and Its Subsidiaries: Company Number PQ 118haffaNo ratings yet

- Amortization TableDocument4 pagesAmortization TableFerdinand SanchezNo ratings yet

- Total Compensation Framework Template (Annex A)Document2 pagesTotal Compensation Framework Template (Annex A)Noreen Boots Gocon-GragasinNo ratings yet

- Project Report On: Saraswati Vidya Mandiram-NarpalaDocument24 pagesProject Report On: Saraswati Vidya Mandiram-NarpalaUsmankhan KhanNo ratings yet

- Balance Sheet of ACC: - in Rs. Cr.Document8 pagesBalance Sheet of ACC: - in Rs. Cr.Rekha RaoNo ratings yet

- Dalmiya Print 065-066Document8 pagesDalmiya Print 065-066Sashi MallikNo ratings yet

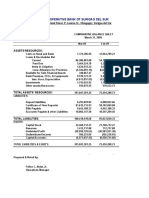

- Cooperative Bank of Surigao Del SurDocument4 pagesCooperative Bank of Surigao Del SurAnonymous iScW9lNo ratings yet

- Your Policy No. 144808 / 53-IPDocument2 pagesYour Policy No. 144808 / 53-IPtanveer.randhawa25No ratings yet

- Accounts (NEW DRAFT) 24 SeptDocument45 pagesAccounts (NEW DRAFT) 24 Septsaria.ossama.95No ratings yet

- Financials at A GlanceDocument2 pagesFinancials at A GlanceAmol MahajanNo ratings yet

- Hylton Center Financials 2010-2017Document1 pageHylton Center Financials 2010-2017Greg Hambrick100% (2)

- Performance HighlightsDocument2 pagesPerformance HighlightsPushpendra KumarNo ratings yet

- Homework 1 Suggested SolutionsDocument14 pagesHomework 1 Suggested SolutionsPHI NGUYEN HOANGNo ratings yet

- Processing Stats v5Document2 pagesProcessing Stats v5rhinoj101No ratings yet

- Accounting ProjectDocument16 pagesAccounting Projectnawal jamshaidNo ratings yet

- Audited Amc 09-10Document14 pagesAudited Amc 09-10kamalkantshuklaNo ratings yet

- Lra Dipa 01 2018Document3 pagesLra Dipa 01 2018Khairul RiskiNo ratings yet

- Balance Sheet of North Delhi Power Limited (2007-2011) : ParticularsDocument5 pagesBalance Sheet of North Delhi Power Limited (2007-2011) : ParticularsBhavika AroraNo ratings yet

- 3rd Quarterly Accounts - Prime Finance 1st MF 13Document1 page3rd Quarterly Accounts - Prime Finance 1st MF 13Abrar FaisalNo ratings yet

- 1 e Ifrs 16 Example Lease Modification Scope Decrease 01Document11 pages1 e Ifrs 16 Example Lease Modification Scope Decrease 01Jashinta Mahadewi MjmNo ratings yet

- BHCPR User's Guide - March 2013Document3 pagesBHCPR User's Guide - March 2013Kaya NedaNo ratings yet

- Peng Teknologi InformasiDocument6 pagesPeng Teknologi InformasiYudo RamadhanNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Exhibit 19ZZGDocument7 pagesExhibit 19ZZGOSDocs2012No ratings yet

- ' in LakhsDocument53 pages' in LakhsParthNo ratings yet

- Receivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesDocument3 pagesReceivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesGlance BautistaNo ratings yet

- Microsoft Vs Intuit ValuationDocument4 pagesMicrosoft Vs Intuit ValuationcorvettejrwNo ratings yet

- The Mechanics of Securitization: A Practical Guide to Structuring and Closing Asset-Backed Security TransactionsFrom EverandThe Mechanics of Securitization: A Practical Guide to Structuring and Closing Asset-Backed Security TransactionsNo ratings yet