You might also like

- Stock Audit of Bank Borrowers: IntroductionDocument5 pagesStock Audit of Bank Borrowers: Introductionravindra kumar jainNo ratings yet

- Stock Audit Manual: Gevaria & AssociatesDocument7 pagesStock Audit Manual: Gevaria & AssociatesparthNo ratings yet

- Mastering Bookkeeping: Unveiling the Key to Financial SuccessFrom EverandMastering Bookkeeping: Unveiling the Key to Financial SuccessNo ratings yet

- Stock AuditDocument5 pagesStock AuditCA Santosh SrivastavaNo ratings yet

- Stock Audit of Bank Borrowers: IntroductionDocument8 pagesStock Audit of Bank Borrowers: Introductionniravtrivedi72No ratings yet

- Stock Audit of Banks BorrowersDocument5 pagesStock Audit of Banks Borrowersrohantailor100% (1)

- Auditing Lecture Notes 04172022Document16 pagesAuditing Lecture Notes 04172022Abegail Cadacio100% (2)

- Accounts of Banking CompaniesDocument24 pagesAccounts of Banking CompaniesrachealllNo ratings yet

- 15.preparation of ProposalDocument48 pages15.preparation of Proposalpuran1234567890No ratings yet

- Stock Audit PresentationDocument27 pagesStock Audit PresentationShan BsmaniNo ratings yet

- Verification and Valuation of Different Kinds of AssetsDocument4 pagesVerification and Valuation of Different Kinds of AssetsRamesh RanjanNo ratings yet

- ACCO 30053 Auditing and Assurance Concepts and Applications 1 Module - AY2021Document76 pagesACCO 30053 Auditing and Assurance Concepts and Applications 1 Module - AY2021Christel Oruga100% (1)

- Chapter 20 - Answer PDFDocument10 pagesChapter 20 - Answer PDFjhienellNo ratings yet

- Audit ProgramDocument9 pagesAudit ProgramChris Ian TagsipNo ratings yet

- Monitoring & Follow Up of Advances: H S Sharma, Guest Faculty, IIBFDocument51 pagesMonitoring & Follow Up of Advances: H S Sharma, Guest Faculty, IIBFBhaskara Sita Ramayya PNo ratings yet

- Company A:c-Banking CompaniesDocument30 pagesCompany A:c-Banking CompaniessarahhussainNo ratings yet

- Unit 6Document12 pagesUnit 6fekadegebretsadik478729No ratings yet

- Approach For Safety of Loans Follow Up and Monitoring Process Q3Document6 pagesApproach For Safety of Loans Follow Up and Monitoring Process Q3maunilshahNo ratings yet

- Portfolio in Applied Auditing: Kenneth Adrian S. BrunoDocument14 pagesPortfolio in Applied Auditing: Kenneth Adrian S. BrunoAngel Dela Cruz CoNo ratings yet

- CH 6 Audit IIDocument14 pagesCH 6 Audit IIsamuel debebeNo ratings yet

- Credit MonitoringDocument20 pagesCredit MonitoringSupriya Gunthey Ranade100% (1)

- Causes For Npa Reasons For Borrower Accountability InternalDocument4 pagesCauses For Npa Reasons For Borrower Accountability InternalMilu Mathew MoorkkattilNo ratings yet

- Credit Monitoring and Follow-Up: MeaningDocument23 pagesCredit Monitoring and Follow-Up: Meaningpuran1234567890100% (2)

- Stock Audit in Banks Compatible ModeDocument6 pagesStock Audit in Banks Compatible ModechhayabiyaniNo ratings yet

- Bank Audit ProgramDocument6 pagesBank Audit Programramu9999100% (1)

- Scope of Internal Audit - RDocument4 pagesScope of Internal Audit - RHarshadaNo ratings yet

- Stock Audit Report Bank FormatDocument18 pagesStock Audit Report Bank FormatVikash AgrawalNo ratings yet

- Audit of Sole ProprietorDocument9 pagesAudit of Sole ProprietorPrincess Bhavika100% (1)

- Personal Textbook Assignment Matthew Huston ACC/491 December 8, 2014 David MancinaDocument5 pagesPersonal Textbook Assignment Matthew Huston ACC/491 December 8, 2014 David MancinaMatt100% (1)

- Mahesh CVDocument4 pagesMahesh CVRj GuptaNo ratings yet

- Audit Programme For Audit of BanksDocument8 pagesAudit Programme For Audit of BanksGaurav AgrawalNo ratings yet

- Compliance Checklist - PlantDocument36 pagesCompliance Checklist - Plantsaji kumarNo ratings yet

- Introduction of The TopicDocument8 pagesIntroduction of The TopicPooja AgarwalNo ratings yet

- Strategic Credit Management - IntroductionDocument14 pagesStrategic Credit Management - IntroductionDr VIRUPAKSHA GOUD G50% (2)

- Advances Pre Sanction and Post SanctionDocument16 pagesAdvances Pre Sanction and Post Sanctionmail2ncNo ratings yet

- Approval, Disburshment and RecoveryDocument6 pagesApproval, Disburshment and Recoveryakash_0000No ratings yet

- Audit ProgrammeDocument12 pagesAudit ProgrammeCA Nagendranadh TadikondaNo ratings yet

- Audit of Liabilities - HandoutsDocument19 pagesAudit of Liabilities - Handoutsanthony23vinaraoNo ratings yet

- Aud Pro Cash and Cash Equi-1-4Document4 pagesAud Pro Cash and Cash Equi-1-4Mikaella JonaNo ratings yet

- Bank Audit Check List & Procedure (Concurrent Audit) : IndexDocument12 pagesBank Audit Check List & Procedure (Concurrent Audit) : IndexCA Jay ThakurNo ratings yet

- Explain What Type of Information Should Be Included in The Schedule For The Permanent File in Respect of The MortgageDocument5 pagesExplain What Type of Information Should Be Included in The Schedule For The Permanent File in Respect of The MortgageBeyonce SmithNo ratings yet

- Chapter-01 Accounting For Banking CompanyDocument26 pagesChapter-01 Accounting For Banking CompanyRabbi Ul Apon100% (1)

- Chapter 24 AnsDocument10 pagesChapter 24 AnsDave Manalo100% (1)

- Current AssetsDocument3 pagesCurrent AssetsAshish DhingraNo ratings yet

- NPA ProjectDocument65 pagesNPA ProjectRanjeet GaikwadNo ratings yet

- Credit - MonitoringDocument39 pagesCredit - MonitoringNeeti SanghaniNo ratings yet

- Substantive Procedures (Combined) 2Document23 pagesSubstantive Procedures (Combined) 2mtolamandisaNo ratings yet

- V4RFP Document As Per RCOBTDocument21 pagesV4RFP Document As Per RCOBTtofik awelNo ratings yet

- Advances & Prudential NormsDocument48 pagesAdvances & Prudential Normssonia87No ratings yet

- FLR - 4Document7 pagesFLR - 4TannyCharayaNo ratings yet

- Audit of Cash and Marketable SecuritiesDocument21 pagesAudit of Cash and Marketable Securitiesዝምታ ተሻለNo ratings yet

- Nagindas Khandwala College: Presented To:-Poonam Popat Ma'amDocument23 pagesNagindas Khandwala College: Presented To:-Poonam Popat Ma'amRitika_swift13No ratings yet

- Audit ProceduresDocument5 pagesAudit ProceduresAna RetNo ratings yet

- Finance LTD.: 1 & 2 QuarterDocument6 pagesFinance LTD.: 1 & 2 QuarterSushil ShresthaNo ratings yet

- Annexure I (Scope of Audit - Concurrent Auditor)Document29 pagesAnnexure I (Scope of Audit - Concurrent Auditor)Niraj JainNo ratings yet

- Auditing Notes PadmasunDocument11 pagesAuditing Notes PadmasunPadmasunNo ratings yet

- Audit ProgramDocument8 pagesAudit ProgramChris Ian TagsipNo ratings yet

- Marketing Strategies ProjectDocument15 pagesMarketing Strategies ProjectKartik TrivediNo ratings yet

- United Bank of IndiaDocument5 pagesUnited Bank of IndiaRajesh DubeyNo ratings yet

- TCG March Report 2023 1681756740Document17 pagesTCG March Report 2023 1681756740Dan CyglerNo ratings yet

- Collecting BankerDocument26 pagesCollecting BankerTeja RaviNo ratings yet

- Hoodies & Sweaters - NUDE PROJECTDocument1 pageHoodies & Sweaters - NUDE PROJECTMartina Carbonell TorderaNo ratings yet

- Financial Management-1: Risk Return Analysis Project 1Document7 pagesFinancial Management-1: Risk Return Analysis Project 1Sukanya VankamamidiNo ratings yet

- Project - PdicDocument60 pagesProject - PdicGellibeeNo ratings yet

- Value Added Subscription PlansDocument1 pageValue Added Subscription PlansChetna SharmaNo ratings yet

- SAP FICO SyllabusDocument1 pageSAP FICO SyllabusMaurya ShantanuNo ratings yet

- UGBS April 2021 Assignment MPhil. MSc. and MBADocument6 pagesUGBS April 2021 Assignment MPhil. MSc. and MBAabigail acheampongNo ratings yet

- Mergers and Acquisitions (M&as) in The Nigerian BankingDocument10 pagesMergers and Acquisitions (M&as) in The Nigerian BankingRitji DimkaNo ratings yet

- DHFL Sanction LetterDocument6 pagesDHFL Sanction LetterRamesh Kulkarni75% (4)

- 2022 - 05 - Bad and Doubtful DebtsDocument39 pages2022 - 05 - Bad and Doubtful DebtsSafi UllahNo ratings yet

- Multiple Choice Questions: Top of FormDocument96 pagesMultiple Choice Questions: Top of Formchanfa3851No ratings yet

- Exon Mobile Financial Data BloombergDocument32 pagesExon Mobile Financial Data BloombergShardul MudeNo ratings yet

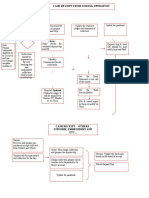

- Cash Receipt From School OperationDocument2 pagesCash Receipt From School Operationmardee justoNo ratings yet

- 15 Code of Ethics For Professional Accountants in The PhilippinesDocument11 pages15 Code of Ethics For Professional Accountants in The PhilippinesDia Mae GenerosoNo ratings yet

- June 2021 Mark SchemeDocument17 pagesJune 2021 Mark SchemeElenaNo ratings yet

- Stand by LCDocument3 pagesStand by LCmd salehinNo ratings yet

- Capital Structure Analysis of Hero HondaDocument7 pagesCapital Structure Analysis of Hero HondaNiklesh ChandakNo ratings yet

- Light BillDocument2 pagesLight BillSANJAY DUMBRENo ratings yet

- Partnership Agreement: 1. PartiesDocument11 pagesPartnership Agreement: 1. PartiesAmelia ConwayNo ratings yet

- Insolvency Law and Corporate RehabilitationDocument33 pagesInsolvency Law and Corporate RehabilitationElizar JoseNo ratings yet

- Auditing Theory Test BankDocument9 pagesAuditing Theory Test BankCezanne Pi-ay EckmanNo ratings yet

- Analysis of Revenue and Expenditure at Citi (Monica Alex Fernandes)Document69 pagesAnalysis of Revenue and Expenditure at Citi (Monica Alex Fernandes)Monica FernandesNo ratings yet

- LOP Insurance Concepts 1704791419Document40 pagesLOP Insurance Concepts 1704791419djhx5vv2s8No ratings yet

- Issue of DebenturesDocument15 pagesIssue of DebenturesKrish BhargavaNo ratings yet

- 2Nd Floor, Palm Spring Centre, Next To D-Mart Shopp - Centre, Link Road, Malad (West), Mumbai, Maharashtra-400064 Phone-022-30801000 Fax-022-28449002Document1 page2Nd Floor, Palm Spring Centre, Next To D-Mart Shopp - Centre, Link Road, Malad (West), Mumbai, Maharashtra-400064 Phone-022-30801000 Fax-022-28449002Brandon WilliamsNo ratings yet

- University of South Wales: Strategic Financial Management (AF4S31-V2) Module Assessment 1Document16 pagesUniversity of South Wales: Strategic Financial Management (AF4S31-V2) Module Assessment 1Regina AtkinsNo ratings yet

- FM11 - CH - 06 - Bonds and Their ValuationDocument49 pagesFM11 - CH - 06 - Bonds and Their ValuationAneesaNo ratings yet

- Institute of Bankers of Sri Lanka: D 07 - Investment BankingDocument17 pagesInstitute of Bankers of Sri Lanka: D 07 - Investment BankingSuvindu DulhanNo ratings yet

- (ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideFrom Everand(ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideRating: 2.5 out of 5 stars2.5/5 (2)

- A Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowFrom EverandA Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowNo ratings yet

- Guide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyFrom EverandGuide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyNo ratings yet

- Business Process Mapping: Improving Customer SatisfactionFrom EverandBusiness Process Mapping: Improving Customer SatisfactionRating: 5 out of 5 stars5/5 (1)

- Bribery and Corruption Casebook: The View from Under the TableFrom EverandBribery and Corruption Casebook: The View from Under the TableNo ratings yet

- Frequently Asked Questions in International Standards on AuditingFrom EverandFrequently Asked Questions in International Standards on AuditingRating: 1 out of 5 stars1/5 (1)

- GDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekFrom EverandGDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekNo ratings yet

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersFrom EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersRating: 4.5 out of 5 stars4.5/5 (11)

- Financial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksFrom EverandFinancial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksRating: 4 out of 5 stars4/5 (1)

- Audit. Review. Compilation. What's the Difference?From EverandAudit. Review. Compilation. What's the Difference?Rating: 5 out of 5 stars5/5 (1)

- Scrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsFrom EverandScrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsNo ratings yet

- The Layman's Guide GDPR Compliance for Small Medium BusinessFrom EverandThe Layman's Guide GDPR Compliance for Small Medium BusinessRating: 5 out of 5 stars5/5 (1)

- Executive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceFrom EverandExecutive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceRating: 4 out of 5 stars4/5 (1)

- GDPR for DevOp(Sec) - The laws, Controls and solutionsFrom EverandGDPR for DevOp(Sec) - The laws, Controls and solutionsRating: 5 out of 5 stars5/5 (1)

- Audit and Assurance Essentials: For Professional Accountancy ExamsFrom EverandAudit and Assurance Essentials: For Professional Accountancy ExamsNo ratings yet

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachFrom EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachRating: 4 out of 5 stars4/5 (1)