You might also like

- Commodity Research Report 12 March 2019 Ways2CapitalDocument13 pagesCommodity Research Report 12 March 2019 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 06 March 2019 Ways2CapitalDocument13 pagesCommodity Research Report 06 March 2019 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 26 December 2018 Ways2CapitalDocument17 pagesEquity Research Report 26 December 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 11 December 2018 Ways2CapitalDocument13 pagesCommodity Research Report 11 December 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 31 December 2018 Ways2CapitalDocument13 pagesCommodity Research Report 31 December 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 03 December 2018 Ways2CapitalDocument13 pagesCommodity Research Report 03 December 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 21 January 2019 Ways2CapitalDocument13 pagesCommodity Research Report 21 January 2019 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 21 January 2019 Ways2CapitalDocument17 pagesEquity Research Report 21 January 2019 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 26 December 2018 Ways2CapitalDocument13 pagesCommodity Research Report 26 December 2018 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 18 December 2018 Ways2CapitalDocument17 pagesEquity Research Report 18 December 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 18 December 2018 Ways2CapitalDocument13 pagesCommodity Research Report 18 December 2018 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 18 September 2018 Ways2CapitalDocument17 pagesEquity Research Report 18 September 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 20 November 2018 Ways2CapitalDocument13 pagesCommodity Research Report 20 November 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 27november 2018 Ways2CapitalDocument13 pagesCommodity Research Report 27november 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 13 November 2018 Ways2CapitalDocument13 pagesCommodity Research Report 13 November 2018 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 27 November 2018 Ways2CapitalDocument17 pagesEquity Research Report 27 November 2018 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 13 November 2018 Ways2CapitalDocument17 pagesEquity Research Report 13 November 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 06 November 2018 Ways2CapitalDocument13 pagesCommodity Research Report 06 November 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 23 October 2018 Ways2CapitalDocument13 pagesCommodity Research Report 23 October 2018 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 06 November 2018 Ways2CapitalDocument17 pagesEquity Research Report 06 November 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 16 October 2018 Ways2CapitalDocument13 pagesCommodity Research Report 16 October 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 30 October 2018 Ways2CapitalDocument13 pagesCommodity Research Report 30 October 2018 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 23 October 2018 Ways2CapitalDocument17 pagesEquity Research Report 23 October 2018 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 09 October 2018 Ways2CapitalDocument17 pagesEquity Research Report 09 October 2018 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 30 October 2018 Ways2CapitalDocument17 pagesEquity Research Report 30 October 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 16 October 2018 Ways2CapitalDocument13 pagesCommodity Research Report 16 October 2018 Ways2CapitalWays2CapitalNo ratings yet

- Equity Research Report 16 October 2018 Ways2CapitalDocument17 pagesEquity Research Report 16 October 2018 Ways2CapitalWays2CapitalNo ratings yet

- Commodity Research Report 09 October 2018 Ways2CapitalDocument13 pagesCommodity Research Report 09 October 2018 Ways2CapitalWays2CapitalNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Gas y Petroleo Enero 2017Document96 pagesGas y Petroleo Enero 2017Jose Santos100% (1)

- Advanced Oil Gas Accounting International Petroleum Accounting International Petroleum Operations MSC Postgraduate Diploma Intensive Full TimeDocument70 pagesAdvanced Oil Gas Accounting International Petroleum Accounting International Petroleum Operations MSC Postgraduate Diploma Intensive Full TimeMoheieldeen SamehNo ratings yet

- Financila Times EuropeDocument36 pagesFinancila Times EuropeTihomir RajčićNo ratings yet

- Production Sharing AgreementsDocument106 pagesProduction Sharing AgreementsAl Hafiz Ibn HamzahNo ratings yet

- The Strategic Importance of Oil in The Iraqi Economy and Its Future Outlook in Light of The Current and Expected Oil Prices For The Period (2010-2030)Document18 pagesThe Strategic Importance of Oil in The Iraqi Economy and Its Future Outlook in Light of The Current and Expected Oil Prices For The Period (2010-2030)Research ParkNo ratings yet

- Homework Week 2Document3 pagesHomework Week 2vernellNo ratings yet

- The Industry HandbookDocument34 pagesThe Industry HandbookslpypndaNo ratings yet

- Business Economics: Presented By: Akshit Arora (201) Yash Bhayani (202) Akhil Sawant (209) Ankit MehtaDocument16 pagesBusiness Economics: Presented By: Akshit Arora (201) Yash Bhayani (202) Akhil Sawant (209) Ankit MehtaYash BhayaniNo ratings yet

- Pakistan's Energy Problems and their Political and Economic EffectsDocument78 pagesPakistan's Energy Problems and their Political and Economic EffectsNaima RabbaniNo ratings yet

- Oil and Gas MCQ QuestionsDocument29 pagesOil and Gas MCQ Questionsabby nzrlNo ratings yet

- Oil & Gas Investment Banking 101 - Interviews, Deals, ValuationDocument31 pagesOil & Gas Investment Banking 101 - Interviews, Deals, ValuationmayorladNo ratings yet

- Imt Covid19 XXXDocument8 pagesImt Covid19 XXXAdrianNo ratings yet

- Reading The Markets Norway: Steeper Norwegian Swap Curve On Higher Wage GrowthDocument10 pagesReading The Markets Norway: Steeper Norwegian Swap Curve On Higher Wage GrowthJaviera Muñoz CarreñoNo ratings yet

- Ramady M Mahdi W Opec in A Shale Oil World Where To Next PDFDocument293 pagesRamady M Mahdi W Opec in A Shale Oil World Where To Next PDFBalanuța IanaNo ratings yet

- Solution Manual For International Economics 15th EditionDocument4 pagesSolution Manual For International Economics 15th Editiondandyizemanuree9nn2y100% (21)

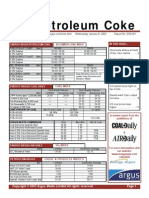

- Pet CokeDocument12 pagesPet Cokezementhead100% (1)

- International Crude Oil Price Movements FactorsDocument28 pagesInternational Crude Oil Price Movements FactorsmksscribdNo ratings yet

- INFLATION REMAINS STEADYDocument17 pagesINFLATION REMAINS STEADYEdito Jr BautistaNo ratings yet

- Nwssu - Mod in Contemporary World - Module2Document34 pagesNwssu - Mod in Contemporary World - Module2raymundo canizaresNo ratings yet

- Literature 102-Thesis-DarwinDocument155 pagesLiterature 102-Thesis-DarwinMartin CharlesNo ratings yet

- D Vandana Hari Vanda InsightsDocument40 pagesD Vandana Hari Vanda InsightsAmanNo ratings yet

- Two Examples of OligopolyDocument21 pagesTwo Examples of Oligopoly1t4No ratings yet

- Current GK November 2022Document52 pagesCurrent GK November 2022venu MNo ratings yet

- BBG Commodity Market PDFDocument9 pagesBBG Commodity Market PDFsabljicaNo ratings yet

- Y 2015 Annual LetterDocument24 pagesY 2015 Annual Letterrwmortell3580No ratings yet

- Oligopoly: Powerpoint Slides Prepared By: Andreea Chiritescu Eastern Illinois UniversityDocument45 pagesOligopoly: Powerpoint Slides Prepared By: Andreea Chiritescu Eastern Illinois UniversitywillowNo ratings yet

- OIL GAS ANGOLA-2021-definitiefDocument20 pagesOIL GAS ANGOLA-2021-definitiefSecretario SigmaNo ratings yet

- Research Paper About Oil Price HikeDocument6 pagesResearch Paper About Oil Price Hikeefeq3hd0100% (1)

- Opec Bulletin 08 2021Document96 pagesOpec Bulletin 08 2021Andre KoichiNo ratings yet

- 05dec23 Asia FCRST Market BriefingDocument55 pages05dec23 Asia FCRST Market BriefingJarodNo ratings yet