You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Pan ApplicationDocument2 pagesPan Applicationamrut9No ratings yet

- Supporting Real-Time Problem Resolution Via Just-in-Time Collaboration With ExpertsDocument2 pagesSupporting Real-Time Problem Resolution Via Just-in-Time Collaboration With Expertsamrut9No ratings yet

- Change in Authorized SignatoriesDocument2 pagesChange in Authorized Signatoriesamrut9No ratings yet

- Names of Siva PDFDocument25 pagesNames of Siva PDFamrut9No ratings yet

- Ethernet Cable Colour - Code Standards & Methods of CrimpingDocument15 pagesEthernet Cable Colour - Code Standards & Methods of Crimpingamrut9No ratings yet

- Balaji Computers: S. No Qty Rate Amount ItemDocument4 pagesBalaji Computers: S. No Qty Rate Amount Itemamrut9No ratings yet

- Help en AlcatekDocument17 pagesHelp en Alcatekamrut9No ratings yet

- Excel FormulaDocument1 pageExcel Formulaamrut9No ratings yet

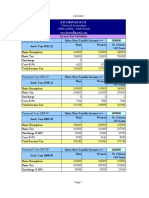

- Year-Wise Tax CalculatorDocument2 pagesYear-Wise Tax Calculatoramrut9No ratings yet

- IFRS ApplicabilityDocument2 pagesIFRS Applicabilityamrut9No ratings yet

- CiplaDocument10 pagesCiplaamrut9100% (1)

- Education in India: Company SecretaryDocument18 pagesEducation in India: Company Secretaryamrut9No ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Housing Finance A Comparative Study of SBI and HDFC BankDocument3 pagesHousing Finance A Comparative Study of SBI and HDFC BankEditor IJTSRDNo ratings yet

- Elliott Wave: Fact or Fiction?: by F. David MinbashianDocument5 pagesElliott Wave: Fact or Fiction?: by F. David Minbashianapi-19771937No ratings yet

- No Objection Certificate PDFDocument1 pageNo Objection Certificate PDFpropvisor real estate100% (1)

- The Sumerian SwindleDocument447 pagesThe Sumerian SwindleqwzrtzNo ratings yet

- Amarpali NoticeDocument4 pagesAmarpali NoticeSharjeel AhmadNo ratings yet

- CH01Document41 pagesCH01ahmad_habibi_70% (1)

- Maritime CommerceDocument7 pagesMaritime CommerceAyeDingoasen-CabalbalNo ratings yet

- Globoeconomic Policies For Overcoming Global RecessionDocument39 pagesGloboeconomic Policies For Overcoming Global RecessionsasumNo ratings yet

- V.K FITNESS J SERIES PDFDocument4 pagesV.K FITNESS J SERIES PDFavik mukherjeeNo ratings yet

- SAN Notification2021Document1 pageSAN Notification2021Ndumiso MagaganeNo ratings yet

- Course Coordinator: Dr. Noor Ulain RizviDocument26 pagesCourse Coordinator: Dr. Noor Ulain RizviMahima Sudhir GaikwadNo ratings yet

- Bookkeeping FinalDocument67 pagesBookkeeping FinalKatlene JoyNo ratings yet

- Accenture V Commission G.R. 190102 (Digest)Document3 pagesAccenture V Commission G.R. 190102 (Digest)mercy rodriguezNo ratings yet

- Chapter 4 Branch AccountingDocument17 pagesChapter 4 Branch Accountingkefyalew TNo ratings yet

- Fundamental RulesDocument41 pagesFundamental RulesSrikanth KovurNo ratings yet

- IMLI-Marine Insurance LawDocument25 pagesIMLI-Marine Insurance LawHERBERTO PARDONo ratings yet

- Item Wise Boq: (Domestic Tenders - Rates Are To Given in Rupees (Inr) Only)Document3 pagesItem Wise Boq: (Domestic Tenders - Rates Are To Given in Rupees (Inr) Only)RAMAN SHARMANo ratings yet

- Credit Risk Analysis of Rupali Bank LimitedDocument105 pagesCredit Risk Analysis of Rupali Bank Limitedkhansha ComputersNo ratings yet

- Scope of Livestock InsuranceDocument16 pagesScope of Livestock InsuranceAjaz HussainNo ratings yet

- SEC. 84. Rates of Estate Tax. - There Shall Be Levied, Assessed, Collected and Paid UponDocument10 pagesSEC. 84. Rates of Estate Tax. - There Shall Be Levied, Assessed, Collected and Paid UponJoy Navaja DominguezNo ratings yet

- Test Bank For Investments 11th Edition Alan Marcus Zvi Bodie Alex Kane Isbn1259277178 Isbn 9781259277177Document24 pagesTest Bank For Investments 11th Edition Alan Marcus Zvi Bodie Alex Kane Isbn1259277178 Isbn 9781259277177JosephGonzalezqxdf97% (38)

- Pakistan Stock Exchange: (1994-2019 OVERVIEW)Document31 pagesPakistan Stock Exchange: (1994-2019 OVERVIEW)danixh HameedNo ratings yet

- InvestmentDocument106 pagesInvestmentSujal BedekarNo ratings yet

- Group Five Efficient Capital Market TheoryDocument21 pagesGroup Five Efficient Capital Market TheoryAmbrose Ageng'aNo ratings yet

- Get Ready For Ifrs 17 ADocument70 pagesGet Ready For Ifrs 17 Aالخليفة دجوNo ratings yet

- Far Week 6 Investment Properties RevieweesDocument4 pagesFar Week 6 Investment Properties RevieweesAdan NadaNo ratings yet

- Iip FinalDocument57 pagesIip FinalNagireddy KalluriNo ratings yet

- My Record of Group ContributionDocument16 pagesMy Record of Group ContributionMemey C.No ratings yet

- Sak EmkmDocument13 pagesSak EmkmniprianahNo ratings yet

- Airlines: About First ResearchDocument16 pagesAirlines: About First ResearchIza YulizaNo ratings yet