You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Guess Paper Tips from Knowledgepool FBDocument6 pagesGuess Paper Tips from Knowledgepool FBShahzadNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- ISO 27002 Questionnaire-Controls 1-10Document12 pagesISO 27002 Questionnaire-Controls 1-10ShahzadNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Stock Template UKDocument19 pagesStock Template UKteddyNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Notification of Lockdown in Sindh Till 16 05 2021 GOSDocument2 pagesNotification of Lockdown in Sindh Till 16 05 2021 GOSShahzadNo ratings yet

- Risk AnalysisDocument26 pagesRisk AnalysisAldo Vm100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- 10-Draft Punjab Municipal Water Act 2014Document32 pages10-Draft Punjab Municipal Water Act 2014ShahzadNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Blood Glucose - 30May2021-12Jun2021Document2 pagesBlood Glucose - 30May2021-12Jun2021ShahzadNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- KCCI member directory listing codes and contact detailsDocument1 pageKCCI member directory listing codes and contact detailsShahzadNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Working Paper 95Document38 pagesWorking Paper 95ShahzadNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Al-Rehman Impex and other companies contact and address detailsDocument1 pageAl-Rehman Impex and other companies contact and address detailsShahzadNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- WSR Csms StoryDocument4 pagesWSR Csms StoryBanjoNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- WSR Csms StoryDocument4 pagesWSR Csms StoryBanjoNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Alimentacao Infantil Cristiane MachadoDocument25 pagesAlimentacao Infantil Cristiane MachadomacouthNo ratings yet

- VoterListweb2016-2017 97Document1 pageVoterListweb2016-2017 97ShahzadNo ratings yet

- VoterListweb2016-2017 35Document1 pageVoterListweb2016-2017 35ShahzadNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Verb Transfer For English To Urdu MTDocument90 pagesVerb Transfer For English To Urdu MTchandamkmNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- VoterListweb2016-2017 74Document1 pageVoterListweb2016-2017 74ShahzadNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- KCCI member directory listingDocument3 pagesKCCI member directory listingShahzad100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- KCCI member directory codes 1281-1296Document1 pageKCCI member directory codes 1281-1296ShahzadNo ratings yet

- Textile Industry: Sector UpdateDocument5 pagesTextile Industry: Sector UpdateShahzadNo ratings yet

- VoterListweb2016-2017 95Document1 pageVoterListweb2016-2017 95Field ChemistNo ratings yet

- VoterListweb2016-2017 29Document1 pageVoterListweb2016-2017 29ShahzadNo ratings yet

- List of KCCI members with contact detailsDocument1 pageList of KCCI members with contact detailsShahzadNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Product KeyDocument1 pageProduct Keymanoj_yadav191985No ratings yet

- Personnel File Checklist for School StaffDocument1 pagePersonnel File Checklist for School StaffShahzadNo ratings yet

- Good Old Lessons in From An Age-Old Fable: TeamworkDocument31 pagesGood Old Lessons in From An Age-Old Fable: Teamworkjennifer sampangNo ratings yet

- KCCI member directory listing over 900 business contactsDocument1 pageKCCI member directory listing over 900 business contactsShahzadNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- VoterListweb2016-2017 60Document1 pageVoterListweb2016-2017 60ShahzadNo ratings yet

- VoterListweb2016-2017 67Document1 pageVoterListweb2016-2017 67ShahzadNo ratings yet

- VoterListweb2016-2017 72Document1 pageVoterListweb2016-2017 72ShahzadNo ratings yet

- A Study On Non Performing Assets of Sbi and Canara BankDocument75 pagesA Study On Non Performing Assets of Sbi and Canara BankeshuNo ratings yet

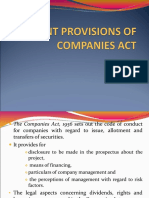

- Relevant Provisions of Companies ActDocument19 pagesRelevant Provisions of Companies Actrthi04No ratings yet

- Siddheshwar Agriculture Cooperative LTD.: Bhurakot, KanchanpurDocument6 pagesSiddheshwar Agriculture Cooperative LTD.: Bhurakot, Kanchanpurmadhu chaudharyNo ratings yet

- BIS Primer PDFDocument71 pagesBIS Primer PDFutah777No ratings yet

- Integration of FICO With Other ModulesDocument2 pagesIntegration of FICO With Other ModulesKrrishNo ratings yet

- Bangladesh Bank: (Base Year: 2020, Job ID: 10151)Document1 pageBangladesh Bank: (Base Year: 2020, Job ID: 10151)taxes zone 5No ratings yet

- General Power of Attorney v2Document4 pagesGeneral Power of Attorney v2Abegail Protacio GuardianNo ratings yet

- USAID Mission Closure ChecklistsDocument41 pagesUSAID Mission Closure Checklistswedaje2003No ratings yet

- MR Cinton Fundulu MR Cinton Fundulu Road 36 Maheba Refugee Settlement SolweziDocument2 pagesMR Cinton Fundulu MR Cinton Fundulu Road 36 Maheba Refugee Settlement Solweziclintion funduluNo ratings yet

- Raki RakiDocument63 pagesRaki RakiRAJA SHEKHARNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- MlArm GuidebookDocument8 pagesMlArm GuidebookMzukisi0% (1)

- Airpay Clients ProductDocument29 pagesAirpay Clients ProductKunal GroverNo ratings yet

- Meaning of Euro Currency Market:: The Following Factors Led To Its Growth: 1. Flow of US AidDocument3 pagesMeaning of Euro Currency Market:: The Following Factors Led To Its Growth: 1. Flow of US AidAijaz KhajaNo ratings yet

- Descriptive Text Beserta Soal Dan Jawaban Victoria C. BeckhamDocument9 pagesDescriptive Text Beserta Soal Dan Jawaban Victoria C. BeckhamDavid SyaifudinNo ratings yet

- CSCI262 Trustedcomputing 1+2Document86 pagesCSCI262 Trustedcomputing 1+2ami_haroonNo ratings yet

- I-Bank User Manual PDFDocument39 pagesI-Bank User Manual PDFLyhalim SethNo ratings yet

- Introduction To E-CommerceDocument30 pagesIntroduction To E-CommerceSuraj ShahNo ratings yet

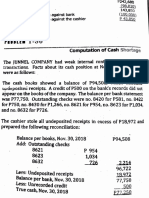

- Problem 2Document4 pagesProblem 2redassdawn100% (1)

- Account Statement SummaryDocument2 pagesAccount Statement SummaryH.P. Builders Pvt. Ltd.No ratings yet

- Bank Relationship Manager Resume SampleDocument8 pagesBank Relationship Manager Resume Samplepehygakasyk2100% (1)

- Mudarabah-A New Guideline of Bank NegaraDocument67 pagesMudarabah-A New Guideline of Bank NegaraolooaNo ratings yet

- Early in January 2013 Hopkins Company Is Preparing For A PDFDocument1 pageEarly in January 2013 Hopkins Company Is Preparing For A PDFAnbu jaromiaNo ratings yet

- DistrictCivilFamilyDktBook JuryDocument96 pagesDistrictCivilFamilyDktBook JuryKristy May0% (1)

- Exchange Rate DeterminationDocument22 pagesExchange Rate Determinationrajarjun100% (1)

- Special Investigation Report On The Allegations of Financial Impropriety in The Office of The Prime MinisterDocument111 pagesSpecial Investigation Report On The Allegations of Financial Impropriety in The Office of The Prime MinisterOle Tangen Jr.No ratings yet

- TRAIN Act of 2018 & Taxation Law UpdatesDocument21 pagesTRAIN Act of 2018 & Taxation Law UpdatesPafra BariuanNo ratings yet

- Job Order Costing ExplainedDocument1 pageJob Order Costing Explainedagm25No ratings yet

- Managerial Decision MakingDocument13 pagesManagerial Decision MakingcrazypankajNo ratings yet

- Fature Tatimore Shitje: Noa New Office AlbaniaDocument2 pagesFature Tatimore Shitje: Noa New Office AlbaniaNOA New office AlbaniaNo ratings yet

- No Due CertificateDocument3 pagesNo Due Certificatemanoj khathumria100% (2)

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.From EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Rating: 5 out of 5 stars5/5 (82)

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsFrom EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNo ratings yet

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- Sacred Success: A Course in Financial MiraclesFrom EverandSacred Success: A Course in Financial MiraclesRating: 5 out of 5 stars5/5 (15)

- Improve Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouFrom EverandImprove Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouRating: 5 out of 5 stars5/5 (5)