You might also like

- Solution Manual For Financial Accounting An Integrated Approach 6th Edition by TrotmanDocument34 pagesSolution Manual For Financial Accounting An Integrated Approach 6th Edition by Trotmana540142314100% (2)

- Anti Avoidance RulesDocument15 pagesAnti Avoidance RulesAanchal KashyapNo ratings yet

- Chapter 16 - Ppe Part 2Document10 pagesChapter 16 - Ppe Part 2Xiena50% (2)

- Turtle StrategyDocument31 pagesTurtle StrategyJeniffer Rayen100% (3)

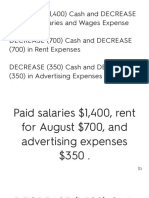

- Part 5Document2 pagesPart 5PRETTYKO0% (1)

- Valuation of PerquisitesDocument22 pagesValuation of PerquisitesKamesh TiwariNo ratings yet

- Income From SalaryDocument66 pagesIncome From SalaryShamika LloydNo ratings yet

- DepositoryDocument29 pagesDepositoryChirag VaghelaNo ratings yet

- Competition Act 2002Document72 pagesCompetition Act 2002Vishwas KumarNo ratings yet

- Income From Other SourcesDocument9 pagesIncome From Other Sourcesrajsab20061093No ratings yet

- Income From Other SourcesDocument12 pagesIncome From Other SourcesMuqddas AbbasNo ratings yet

- Final FM NotesDocument54 pagesFinal FM NotesPawan YadavNo ratings yet

- SEBI: The Purpose, Objective and Functions of SEBIDocument10 pagesSEBI: The Purpose, Objective and Functions of SEBIKunal0% (1)

- Income Under The Head of SalaryDocument2 pagesIncome Under The Head of Salarykajal100% (1)

- Class - 1 Meaning, Nature, and Scope of Corporate FinanceDocument2 pagesClass - 1 Meaning, Nature, and Scope of Corporate FinancemonicaNo ratings yet

- The Value of The Bond or Debenture Is The "FAIR (INTRINSIC / ECOCOMIC) VALUE" WhichDocument3 pagesThe Value of The Bond or Debenture Is The "FAIR (INTRINSIC / ECOCOMIC) VALUE" WhichWahaj Kayani100% (1)

- Assignment On Role of EcgcDocument11 pagesAssignment On Role of EcgcBhawna DagarNo ratings yet

- Buy Back of Shares Under The Companies Act, 1956 - An InsightDocument4 pagesBuy Back of Shares Under The Companies Act, 1956 - An InsightHrdk DveNo ratings yet

- Procedure For Assessment of Income TaxDocument3 pagesProcedure For Assessment of Income Taxdiksha kumariNo ratings yet

- Buy Back PowerPoint Presentation CompleteDocument22 pagesBuy Back PowerPoint Presentation CompleteRaj GandhiNo ratings yet

- Questions of Corporate GovernanceDocument6 pagesQuestions of Corporate GovernanceVrushali ThobhaniNo ratings yet

- Factors Determining Capital StructureDocument3 pagesFactors Determining Capital StructuretushNo ratings yet

- Deposit Insurance and Credit Guarantee Corporation Act 1961Document10 pagesDeposit Insurance and Credit Guarantee Corporation Act 1961Debayan GhoshNo ratings yet

- Reconstruction and Winding Up of A CompanyDocument29 pagesReconstruction and Winding Up of A CompanyjithukumarNo ratings yet

- Residential Status and Incidence of Tax On Income Under Income Tax ActDocument6 pagesResidential Status and Incidence of Tax On Income Under Income Tax ActhaseefaNo ratings yet

- Income Under The Head SalaryDocument8 pagesIncome Under The Head Salarykhullar6870No ratings yet

- Unit - 4 Study Material ACGDocument21 pagesUnit - 4 Study Material ACGAbhijeet UpadhyayNo ratings yet

- Foreign Exchange Management Act, 1999Document33 pagesForeign Exchange Management Act, 1999Syed FarazNo ratings yet

- Financial Market Regulation FDDocument15 pagesFinancial Market Regulation FDShubham RawatNo ratings yet

- Indian Depository ReceiptsDocument16 pagesIndian Depository Receipts777priyanka100% (1)

- Investor ProtectionDocument9 pagesInvestor ProtectionGaurav SharmaNo ratings yet

- Paper VI Income TaxDocument245 pagesPaper VI Income TaxMukul SharmaNo ratings yet

- Introduction - SEBI Takeover CodeDocument7 pagesIntroduction - SEBI Takeover CodeSHUBHANGI DIXITNo ratings yet

- 75ad8sem IX Banking and Insurance Law-Pdf - 2Document1 page75ad8sem IX Banking and Insurance Law-Pdf - 2Om H TiwariNo ratings yet

- Demerger and Tax On M&aDocument5 pagesDemerger and Tax On M&aChandan SinghNo ratings yet

- Winding Up OF COMPANYDocument19 pagesWinding Up OF COMPANYRabbikaNo ratings yet

- Competition Law ProjectDocument11 pagesCompetition Law Projectprithvi yadavNo ratings yet

- Assessment of Hindu Undivided FamilyDocument3 pagesAssessment of Hindu Undivided FamilyRupali Singh0% (1)

- Assessment On Agricultural IncomeDocument28 pagesAssessment On Agricultural Incomedivya srivastavaNo ratings yet

- International LiquidityDocument4 pagesInternational LiquidityAshish TagadeNo ratings yet

- Insurance Act 1938Document19 pagesInsurance Act 1938SijoNo ratings yet

- General Principles of Insurance LawDocument12 pagesGeneral Principles of Insurance LawCarina Amor ClaveriaNo ratings yet

- Income Under The Head SalariesDocument21 pagesIncome Under The Head SalariesAnupam BaliNo ratings yet

- DebenturesDocument12 pagesDebenturesPayal Patel100% (2)

- Special Contracts PDFDocument52 pagesSpecial Contracts PDFSakshi VermaNo ratings yet

- Shares: Meaning and Nature of SharesDocument9 pagesShares: Meaning and Nature of SharesNeenaNo ratings yet

- A Project Report On Depository System inDocument27 pagesA Project Report On Depository System ingupthaNo ratings yet

- L 20 Salient Features of Indian ConstitutionDocument9 pagesL 20 Salient Features of Indian ConstitutionKartike JainNo ratings yet

- Own or LeaseDocument6 pagesOwn or LeaseMANOJNo ratings yet

- Income Tax Law & Practice-Lesson - 1 To 12Document250 pagesIncome Tax Law & Practice-Lesson - 1 To 12Space ResearchNo ratings yet

- Portfolio TheoryDocument6 pagesPortfolio TheorykrgitNo ratings yet

- Resdential Status Questionsby Garun Kumar GDCM SrikakulamDocument9 pagesResdential Status Questionsby Garun Kumar GDCM Srikakulamgeddadaarun100% (1)

- International Liquidity & International ReservesDocument17 pagesInternational Liquidity & International ReservesPrabu Manoharan100% (1)

- Tax Planning MergerDocument4 pagesTax Planning MergerAks SinhaNo ratings yet

- Set Off & Carry Forward of LossesDocument21 pagesSet Off & Carry Forward of LossesanchalNo ratings yet

- Debt MarketDocument11 pagesDebt MarketPsychopheticNo ratings yet

- Termination of Lease by Notice: A Project Proposal Made by NameDocument5 pagesTermination of Lease by Notice: A Project Proposal Made by NameGyanendra SinghNo ratings yet

- Greenbury Committee PresDocument19 pagesGreenbury Committee PresDeepesh YadavNo ratings yet

- Partnership Firm TaxationDocument4 pagesPartnership Firm TaxationAvishek PathakNo ratings yet

- Business Law - Electronic RecordsDocument11 pagesBusiness Law - Electronic RecordsVinamra Garg100% (1)

- Project On Banker and CustomersDocument85 pagesProject On Banker and Customersrakesh9006No ratings yet

- Security Analysis and Portfolio Management: Master of Business AdministrationDocument80 pagesSecurity Analysis and Portfolio Management: Master of Business AdministrationSagar Paul'gNo ratings yet

- Investigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorFrom EverandInvestigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorNo ratings yet

- Notes of Dividend PolicyDocument16 pagesNotes of Dividend PolicyVineet VermaNo ratings yet

- Threading The Needle: Value Creation in A Low-Growth EconomyDocument0 pagesThreading The Needle: Value Creation in A Low-Growth EconomyMadhavasadasivan PothiyilNo ratings yet

- Work Profile of Officers in Credit Risk Management Cell 1) Senior ManagerDocument4 pagesWork Profile of Officers in Credit Risk Management Cell 1) Senior ManagerMadhavasadasivan PothiyilNo ratings yet

- Deputy General Manager Group Head - IRMG: Divya.N OffierDocument1 pageDeputy General Manager Group Head - IRMG: Divya.N OffierMadhavasadasivan PothiyilNo ratings yet

- 16 Business GroupsDocument12 pages16 Business GroupsMadhavasadasivan PothiyilNo ratings yet

- Contract Costing - Practise ProblemsDocument3 pagesContract Costing - Practise ProblemsMadhavasadasivan Pothiyil50% (2)

- Practice Questions For OBEDocument16 pagesPractice Questions For OBEJaihindNo ratings yet

- Chapter 11: The Efficient Market Hypothesis: Problem SetsDocument9 pagesChapter 11: The Efficient Market Hypothesis: Problem SetsNatalie OngNo ratings yet

- Topic 18 - Structured Products and SecuritisationDocument44 pagesTopic 18 - Structured Products and SecuritisationDweep KapadiaNo ratings yet

- Security Analysis AND Portfolio ManagementDocument12 pagesSecurity Analysis AND Portfolio ManagementBhoomesh ChandolaNo ratings yet

- Institute of Accountancy ArushaDocument15 pagesInstitute of Accountancy ArushaaureliaNo ratings yet

- Conso Sofp - Chapter 10Document23 pagesConso Sofp - Chapter 10bibijamiatun08No ratings yet

- Go Rural FM AssignmentDocument31 pagesGo Rural FM AssignmentHumphrey OsaigbeNo ratings yet

- 15 Minute Opening Range BreakoutDocument5 pages15 Minute Opening Range BreakoutSIightlyNo ratings yet

- Partnership HandoutsDocument9 pagesPartnership HandoutsEuniceChungNo ratings yet

- Torrent PowerDocument8 pagesTorrent PowerSudhir SinghNo ratings yet

- QuizletDocument150 pagesQuizletSaif Ali KhanNo ratings yet

- The Karnataka Bank Limited Ulwe: Date: 16-05-2023Document53 pagesThe Karnataka Bank Limited Ulwe: Date: 16-05-2023Amit SinghNo ratings yet

- Amfi Mock TestDocument6 pagesAmfi Mock TestDhiraj100% (3)

- Divis Laboratories LTD Industry: Pharmaceuticals - Indian - Bulk DrugsDocument19 pagesDivis Laboratories LTD Industry: Pharmaceuticals - Indian - Bulk DrugsAbhishekKumarNo ratings yet

- Equity PricingDocument4 pagesEquity PricingMichelle ManuelNo ratings yet

- Stock Cheat SheetDocument6 pagesStock Cheat SheetalishaNo ratings yet

- Smoke AND MirrorsDocument23 pagesSmoke AND MirrorsKinNo ratings yet

- Financial Ratios - Sheet1Document4 pagesFinancial Ratios - Sheet1Melanie SamsonaNo ratings yet

- Laporan Keuangan PT - Hutama KaryaDocument152 pagesLaporan Keuangan PT - Hutama KaryaAlfa AnugerahNo ratings yet

- Accounting For Taxes 6Document7 pagesAccounting For Taxes 6charlene kate bunaoNo ratings yet

- Analisa Ekonomi: Break Event Point (BEP)Document17 pagesAnalisa Ekonomi: Break Event Point (BEP)zahrah nadhirah kaniaNo ratings yet

- Bizuneh MindaDocument58 pagesBizuneh Mindasamibelay1234No ratings yet

- Fine Foods Limited: FU Wang Food LimitedDocument8 pagesFine Foods Limited: FU Wang Food LimitedS. M. Zamirul IslamNo ratings yet

- How To Make The Most of Small Business Qualified StockDocument2 pagesHow To Make The Most of Small Business Qualified StockMahesh GajjelliNo ratings yet

- KPIs For Finance & Accounting ManagerDocument5 pagesKPIs For Finance & Accounting Managervmglenn.ivcNo ratings yet

- 08 Long Term Construction ContractsDocument2 pages08 Long Term Construction ContractsErineNo ratings yet