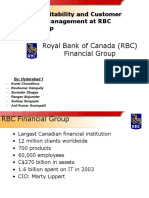

Case Study Royal Bank of Canada

Case Study Royal Bank of Canada

You might also like

- EY Case Study Technology ImplementationDocument6 pagesEY Case Study Technology ImplementationDarshani Audhish100% (1)

- Michelin: Building A Digital Service Platform: AssignmentDocument4 pagesMichelin: Building A Digital Service Platform: AssignmentKirat Chhabra100% (1)

- Esmt Business-Case Brochure 0Document24 pagesEsmt Business-Case Brochure 0Pulkit RitoliaNo ratings yet

- Cost of Equity Risk Free Rate of Return + Beta × (Market Rate of Return - Risk Free Rate of Return)Document7 pagesCost of Equity Risk Free Rate of Return + Beta × (Market Rate of Return - Risk Free Rate of Return)chatterjee rikNo ratings yet

- RBC Financial GroupDocument25 pagesRBC Financial GroupRangan Majumder50% (2)

- RBC CaseAnswers Group13Document4 pagesRBC CaseAnswers Group13Shikha Gupta100% (1)

- Marvel Case SolutionsDocument3 pagesMarvel Case Solutionsmayur7894No ratings yet

- Case Study Presentation - Royal Bank of CanadaDocument6 pagesCase Study Presentation - Royal Bank of CanadaAbhishek Verma100% (1)

- Summary of Elkay CaseDocument1 pageSummary of Elkay CaseJessi Badillo BustamanteNo ratings yet

- Case 15 TN Facebook's BeaconDocument3 pagesCase 15 TN Facebook's BeaconAfiq Hassan50% (2)

- Case Study - Reaching The Summit and beyond-HKBN PDFDocument26 pagesCase Study - Reaching The Summit and beyond-HKBN PDFSitara Qadir100% (1)

- Engstrom Auto Mirror Plant Case StudyDocument2 pagesEngstrom Auto Mirror Plant Case StudySumedh Ukey100% (1)

- Fab Lab Business ModelsDocument8 pagesFab Lab Business Modelsptroxler100% (1)

- RBC Case StudyDocument20 pagesRBC Case StudyIshmeet SinghNo ratings yet

- A Tale of Two Electronic Components DistributorsDocument2 pagesA Tale of Two Electronic Components DistributorsAqsa100% (1)

- City BANK Performance EvaluationDocument6 pagesCity BANK Performance EvaluationAnkit SachdevaNo ratings yet

- IHRM HSBC Case Study 3Document3 pagesIHRM HSBC Case Study 3bhavyasree pothulaNo ratings yet

- Hanover Bates Analysis - Intro N Case FactsDocument8 pagesHanover Bates Analysis - Intro N Case FactsMuhammad Jahanzeb AamirNo ratings yet

- Swot Analysis of Banking IndustryDocument3 pagesSwot Analysis of Banking Industrymehreenshahid789No ratings yet

- Consultant Comeuppance: - Gautam - Khayati - Namita - Pulkit - Saurabh - SumitDocument15 pagesConsultant Comeuppance: - Gautam - Khayati - Namita - Pulkit - Saurabh - SumitSaurabh PaliwalNo ratings yet

- Transforming A National Education SystemDocument6 pagesTransforming A National Education Systemeh07No ratings yet

- Dbs Group Fact Sheet: Corporate InformationDocument10 pagesDbs Group Fact Sheet: Corporate InformationleekosalNo ratings yet

- Cola Wars Continue: Coke & Pepsi inDocument14 pagesCola Wars Continue: Coke & Pepsi inSumit Thakur75% (12)

- Q1. What Are The Organizational and Operational Issues That Underlie The Problems Facing BPS?Document5 pagesQ1. What Are The Organizational and Operational Issues That Underlie The Problems Facing BPS?Munsif JavedNo ratings yet

- Citi Bank CaseDocument3 pagesCiti Bank Casedua khanNo ratings yet

- Tugas TPPE Indra SatrioDocument26 pagesTugas TPPE Indra SatrioIndra SatrioNo ratings yet

- Motion For Summary JudgmentDocument27 pagesMotion For Summary JudgmentKING 5 News100% (1)

- RBC CaseAnswers Group13Document4 pagesRBC CaseAnswers Group13Jayesh KukretiNo ratings yet

- RBC Case Analysis Tahir SheikhDocument3 pagesRBC Case Analysis Tahir SheikhtahirNo ratings yet

- American Express Final ProjectDocument15 pagesAmerican Express Final Projectapi-36963310% (3)

- At Capital OneDocument36 pagesAt Capital OnesumeetpatnaikNo ratings yet

- Case Analysis 2Document5 pagesCase Analysis 2Bhavesh ChoudharyNo ratings yet

- Team9 - Crafting & Executing Offshore IT StrategyDocument6 pagesTeam9 - Crafting & Executing Offshore IT StrategyAnkit SachdevaNo ratings yet

- Credit Card Marketing: Bank of AmericaDocument3 pagesCredit Card Marketing: Bank of AmericaHamna ShahidNo ratings yet

- Chapter: One: 1.1origin of The ReportDocument38 pagesChapter: One: 1.1origin of The ReportRaihan PervezNo ratings yet

- Case Study UPS & MashaweerDocument12 pagesCase Study UPS & MashaweerMalik of ChakwalNo ratings yet

- Learn) .: CRM Case Study EMBA 2015-2016 Soham Pradhan (Uemf15027)Document2 pagesLearn) .: CRM Case Study EMBA 2015-2016 Soham Pradhan (Uemf15027)ashishNo ratings yet

- The Royal Bank of Scotland Group: The Human Capital StrategyDocument2 pagesThe Royal Bank of Scotland Group: The Human Capital StrategyM Reihan F RNo ratings yet

- Performance Management - ACS - Group 5Document5 pagesPerformance Management - ACS - Group 5El KonstantinNo ratings yet

- RBC Financial Group Power PointDocument25 pagesRBC Financial Group Power PointLevina Sabrina Syah100% (2)

- A Case Study On International Expansion: When Amazon Went To ChinaDocument3 pagesA Case Study On International Expansion: When Amazon Went To ChinaitsarNo ratings yet

- Case Study - Unilever in BrazilDocument1 pageCase Study - Unilever in BrazilArunaNo ratings yet

- Walmart Case StudyDocument14 pagesWalmart Case StudySugandha GhadiNo ratings yet

- Dynamics Capabilities Modelo PPT MomoDocument44 pagesDynamics Capabilities Modelo PPT MomoluanasimonNo ratings yet

- Minor Project ON 'Plastic Money of HDFC Bank''Document67 pagesMinor Project ON 'Plastic Money of HDFC Bank''ankushbabbarbcomNo ratings yet

- Meet 1 - Assignment On Mashaweer Case StudyDocument5 pagesMeet 1 - Assignment On Mashaweer Case StudyDavid MoreiraNo ratings yet

- Porter 5 Force Analysis BankingDocument2 pagesPorter 5 Force Analysis BankingM.K Ravi100% (1)

- Hewlett-Packard (HP) Business Strategy ReportDocument33 pagesHewlett-Packard (HP) Business Strategy Reportjessica_liemNo ratings yet

- Bandhan Bank MbaDocument15 pagesBandhan Bank MbaShebin JohnyNo ratings yet

- Jcpenney Mini-Case 1. What Strategy Was The New Ceo at Jcpenney Seeking To Implement Given The Generic Strategies Found in Chapter 4?Document1 pageJcpenney Mini-Case 1. What Strategy Was The New Ceo at Jcpenney Seeking To Implement Given The Generic Strategies Found in Chapter 4?Leah C.No ratings yet

- Consolidated Drugs Inc - B4Document11 pagesConsolidated Drugs Inc - B4Vaibhav Singh50% (2)

- Maersk: Betting On Blockchain: Group 5Document4 pagesMaersk: Betting On Blockchain: Group 5Surajit MajiNo ratings yet

- Hong Kong Disneyland - Section C - Group 3 PDFDocument7 pagesHong Kong Disneyland - Section C - Group 3 PDFsainath04No ratings yet

- Balbir PashaDocument2 pagesBalbir PashaANUSHKANo ratings yet

- Yahoo! The $100 Million Man: Case OverviewDocument5 pagesYahoo! The $100 Million Man: Case OverviewKriti Sahore0% (2)

- Caribbean BauxiteDocument3 pagesCaribbean BauxiteAdeel Ahmad Bhatti100% (2)

- Introduction To CRMDocument16 pagesIntroduction To CRMkrupal_desaiNo ratings yet

- Summary of Vm#1 Customer FocusDocument6 pagesSummary of Vm#1 Customer FocusShekinah Faith RequintelNo ratings yet

- Chapter One: Introducing of The ReportDocument19 pagesChapter One: Introducing of The Reportrabin sahaNo ratings yet

- Boa On ForeclosureDocument252 pagesBoa On ForeclosureCarolyn WilderNo ratings yet

- SM PPT RBCDocument20 pagesSM PPT RBCAnkita KumariNo ratings yet

- Field Study ProposaL - Feb 10 2020Document10 pagesField Study ProposaL - Feb 10 2020Simran KaurNo ratings yet

- EY Global Consumer Banking Survey 2014Document48 pagesEY Global Consumer Banking Survey 2014ohmygodNo ratings yet

- Assignment: 1 International Human Resources ManagementDocument2 pagesAssignment: 1 International Human Resources ManagementAsm TowheedNo ratings yet

- Sampling of Geosynthetics For TestingDocument3 pagesSampling of Geosynthetics For TestingEdmundo Jaita CuellarNo ratings yet

- Chapter 6 Security AnalysisDocument46 pagesChapter 6 Security AnalysisAshraf KhamisaNo ratings yet

- 4.2 Process CapacityDocument11 pages4.2 Process Capacitysaheb167No ratings yet

- Anu Ujin Bat Erdene CV Resume PDFDocument1 pageAnu Ujin Bat Erdene CV Resume PDFAnuUjin BatErdeneNo ratings yet

- Lazada Seller Center 5Document39 pagesLazada Seller Center 5Mohd Wildan Amir MusaNo ratings yet

- Ujwala N Jagdale and Ors Vs Jagdale Industries PriNC201723061716192583COM45336Document8 pagesUjwala N Jagdale and Ors Vs Jagdale Industries PriNC201723061716192583COM45336Aryan AnandNo ratings yet

- Lecture 2 Kaizen Continuous Improvement - 3Document53 pagesLecture 2 Kaizen Continuous Improvement - 3mannoqamarNo ratings yet

- Ratio Rate ProportionDocument1 pageRatio Rate Proportionfile.kurniawanNo ratings yet

- A Book For Advertising Warriors: How To Make A Benta by Greg B. MacabentaDocument2 pagesA Book For Advertising Warriors: How To Make A Benta by Greg B. MacabentaLorna Dietz100% (1)

- Bull Whip Effect ASsignmentDocument5 pagesBull Whip Effect ASsignmentSajjad HanifNo ratings yet

- Maritime ClusterDocument189 pagesMaritime ClusterTRISTIANDINDA PERMATANo ratings yet

- MDI Graduation Booklet October 2015 Updated Aslani BioDocument20 pagesMDI Graduation Booklet October 2015 Updated Aslani BioAli MraniNo ratings yet

- Portfolio of Telenor Pakistan: HistoryDocument3 pagesPortfolio of Telenor Pakistan: HistoryRamis Raza XaidiNo ratings yet

- Manifesto Metamorphosis of The Ghana Football Association by Aspirant For The GFA Elections AMANDA CLINTONDocument8 pagesManifesto Metamorphosis of The Ghana Football Association by Aspirant For The GFA Elections AMANDA CLINTONKweku Zurek100% (3)

- Admitting Is Gold! Randy RayDocument19 pagesAdmitting Is Gold! Randy RayDaniel WaruguruNo ratings yet

- Profit Volume ChartDocument10 pagesProfit Volume ChartAnonymous 0HycR53No ratings yet

- Ankur Mathur IIPM ResumeDocument3 pagesAnkur Mathur IIPM Resumesarabjitsingh123No ratings yet

- Privatization of Public ServiceDocument41 pagesPrivatization of Public Servicedexie de guzmanNo ratings yet

- Alex Popescu CVDocument8 pagesAlex Popescu CVi.alexpopescuNo ratings yet

- PartnershipDocument8 pagesPartnershipOllie WattsNo ratings yet

- Operations Management - Capacity Planning and Control Sample PDFDocument3 pagesOperations Management - Capacity Planning and Control Sample PDFQuincy RileyNo ratings yet

- BritanniaDocument49 pagesBritanniaParinNo ratings yet

- 16 Best COO Books To Read in 2023Document21 pages16 Best COO Books To Read in 2023NAGARAJU MOTUPALLINo ratings yet

- Information System Management of Idea Cellular Ltd.Document25 pagesInformation System Management of Idea Cellular Ltd.my frnd ganesha100% (1)

- 03 - Review of Literature PDFDocument8 pages03 - Review of Literature PDFJaspal AroraNo ratings yet

- Pearson Edexcel Gcse Business 2021 Paper1 Questionpaper NewformatDocument24 pagesPearson Edexcel Gcse Business 2021 Paper1 Questionpaper NewformatMiri AmeeNo ratings yet

You might also like

- EY Case Study Technology ImplementationDocument6 pagesEY Case Study Technology ImplementationDarshani Audhish100% (1)

- Michelin: Building A Digital Service Platform: AssignmentDocument4 pagesMichelin: Building A Digital Service Platform: AssignmentKirat Chhabra100% (1)

- Esmt Business-Case Brochure 0Document24 pagesEsmt Business-Case Brochure 0Pulkit RitoliaNo ratings yet

- Cost of Equity Risk Free Rate of Return + Beta × (Market Rate of Return - Risk Free Rate of Return)Document7 pagesCost of Equity Risk Free Rate of Return + Beta × (Market Rate of Return - Risk Free Rate of Return)chatterjee rikNo ratings yet

- RBC Financial GroupDocument25 pagesRBC Financial GroupRangan Majumder50% (2)

- RBC CaseAnswers Group13Document4 pagesRBC CaseAnswers Group13Shikha Gupta100% (1)

- Marvel Case SolutionsDocument3 pagesMarvel Case Solutionsmayur7894No ratings yet

- Case Study Presentation - Royal Bank of CanadaDocument6 pagesCase Study Presentation - Royal Bank of CanadaAbhishek Verma100% (1)

- Summary of Elkay CaseDocument1 pageSummary of Elkay CaseJessi Badillo BustamanteNo ratings yet

- Case 15 TN Facebook's BeaconDocument3 pagesCase 15 TN Facebook's BeaconAfiq Hassan50% (2)

- Case Study - Reaching The Summit and beyond-HKBN PDFDocument26 pagesCase Study - Reaching The Summit and beyond-HKBN PDFSitara Qadir100% (1)

- Engstrom Auto Mirror Plant Case StudyDocument2 pagesEngstrom Auto Mirror Plant Case StudySumedh Ukey100% (1)

- Fab Lab Business ModelsDocument8 pagesFab Lab Business Modelsptroxler100% (1)

- RBC Case StudyDocument20 pagesRBC Case StudyIshmeet SinghNo ratings yet

- A Tale of Two Electronic Components DistributorsDocument2 pagesA Tale of Two Electronic Components DistributorsAqsa100% (1)

- City BANK Performance EvaluationDocument6 pagesCity BANK Performance EvaluationAnkit SachdevaNo ratings yet

- IHRM HSBC Case Study 3Document3 pagesIHRM HSBC Case Study 3bhavyasree pothulaNo ratings yet

- Hanover Bates Analysis - Intro N Case FactsDocument8 pagesHanover Bates Analysis - Intro N Case FactsMuhammad Jahanzeb AamirNo ratings yet

- Swot Analysis of Banking IndustryDocument3 pagesSwot Analysis of Banking Industrymehreenshahid789No ratings yet

- Consultant Comeuppance: - Gautam - Khayati - Namita - Pulkit - Saurabh - SumitDocument15 pagesConsultant Comeuppance: - Gautam - Khayati - Namita - Pulkit - Saurabh - SumitSaurabh PaliwalNo ratings yet

- Transforming A National Education SystemDocument6 pagesTransforming A National Education Systemeh07No ratings yet

- Dbs Group Fact Sheet: Corporate InformationDocument10 pagesDbs Group Fact Sheet: Corporate InformationleekosalNo ratings yet

- Cola Wars Continue: Coke & Pepsi inDocument14 pagesCola Wars Continue: Coke & Pepsi inSumit Thakur75% (12)

- Q1. What Are The Organizational and Operational Issues That Underlie The Problems Facing BPS?Document5 pagesQ1. What Are The Organizational and Operational Issues That Underlie The Problems Facing BPS?Munsif JavedNo ratings yet

- Citi Bank CaseDocument3 pagesCiti Bank Casedua khanNo ratings yet

- Tugas TPPE Indra SatrioDocument26 pagesTugas TPPE Indra SatrioIndra SatrioNo ratings yet

- Motion For Summary JudgmentDocument27 pagesMotion For Summary JudgmentKING 5 News100% (1)

- RBC CaseAnswers Group13Document4 pagesRBC CaseAnswers Group13Jayesh KukretiNo ratings yet

- RBC Case Analysis Tahir SheikhDocument3 pagesRBC Case Analysis Tahir SheikhtahirNo ratings yet

- American Express Final ProjectDocument15 pagesAmerican Express Final Projectapi-36963310% (3)

- At Capital OneDocument36 pagesAt Capital OnesumeetpatnaikNo ratings yet

- Case Analysis 2Document5 pagesCase Analysis 2Bhavesh ChoudharyNo ratings yet

- Team9 - Crafting & Executing Offshore IT StrategyDocument6 pagesTeam9 - Crafting & Executing Offshore IT StrategyAnkit SachdevaNo ratings yet

- Credit Card Marketing: Bank of AmericaDocument3 pagesCredit Card Marketing: Bank of AmericaHamna ShahidNo ratings yet

- Chapter: One: 1.1origin of The ReportDocument38 pagesChapter: One: 1.1origin of The ReportRaihan PervezNo ratings yet

- Case Study UPS & MashaweerDocument12 pagesCase Study UPS & MashaweerMalik of ChakwalNo ratings yet

- Learn) .: CRM Case Study EMBA 2015-2016 Soham Pradhan (Uemf15027)Document2 pagesLearn) .: CRM Case Study EMBA 2015-2016 Soham Pradhan (Uemf15027)ashishNo ratings yet

- The Royal Bank of Scotland Group: The Human Capital StrategyDocument2 pagesThe Royal Bank of Scotland Group: The Human Capital StrategyM Reihan F RNo ratings yet

- Performance Management - ACS - Group 5Document5 pagesPerformance Management - ACS - Group 5El KonstantinNo ratings yet

- RBC Financial Group Power PointDocument25 pagesRBC Financial Group Power PointLevina Sabrina Syah100% (2)

- A Case Study On International Expansion: When Amazon Went To ChinaDocument3 pagesA Case Study On International Expansion: When Amazon Went To ChinaitsarNo ratings yet

- Case Study - Unilever in BrazilDocument1 pageCase Study - Unilever in BrazilArunaNo ratings yet

- Walmart Case StudyDocument14 pagesWalmart Case StudySugandha GhadiNo ratings yet

- Dynamics Capabilities Modelo PPT MomoDocument44 pagesDynamics Capabilities Modelo PPT MomoluanasimonNo ratings yet

- Minor Project ON 'Plastic Money of HDFC Bank''Document67 pagesMinor Project ON 'Plastic Money of HDFC Bank''ankushbabbarbcomNo ratings yet

- Meet 1 - Assignment On Mashaweer Case StudyDocument5 pagesMeet 1 - Assignment On Mashaweer Case StudyDavid MoreiraNo ratings yet

- Porter 5 Force Analysis BankingDocument2 pagesPorter 5 Force Analysis BankingM.K Ravi100% (1)

- Hewlett-Packard (HP) Business Strategy ReportDocument33 pagesHewlett-Packard (HP) Business Strategy Reportjessica_liemNo ratings yet

- Bandhan Bank MbaDocument15 pagesBandhan Bank MbaShebin JohnyNo ratings yet

- Jcpenney Mini-Case 1. What Strategy Was The New Ceo at Jcpenney Seeking To Implement Given The Generic Strategies Found in Chapter 4?Document1 pageJcpenney Mini-Case 1. What Strategy Was The New Ceo at Jcpenney Seeking To Implement Given The Generic Strategies Found in Chapter 4?Leah C.No ratings yet

- Consolidated Drugs Inc - B4Document11 pagesConsolidated Drugs Inc - B4Vaibhav Singh50% (2)

- Maersk: Betting On Blockchain: Group 5Document4 pagesMaersk: Betting On Blockchain: Group 5Surajit MajiNo ratings yet

- Hong Kong Disneyland - Section C - Group 3 PDFDocument7 pagesHong Kong Disneyland - Section C - Group 3 PDFsainath04No ratings yet

- Balbir PashaDocument2 pagesBalbir PashaANUSHKANo ratings yet

- Yahoo! The $100 Million Man: Case OverviewDocument5 pagesYahoo! The $100 Million Man: Case OverviewKriti Sahore0% (2)

- Caribbean BauxiteDocument3 pagesCaribbean BauxiteAdeel Ahmad Bhatti100% (2)

- Introduction To CRMDocument16 pagesIntroduction To CRMkrupal_desaiNo ratings yet

- Summary of Vm#1 Customer FocusDocument6 pagesSummary of Vm#1 Customer FocusShekinah Faith RequintelNo ratings yet

- Chapter One: Introducing of The ReportDocument19 pagesChapter One: Introducing of The Reportrabin sahaNo ratings yet

- Boa On ForeclosureDocument252 pagesBoa On ForeclosureCarolyn WilderNo ratings yet

- SM PPT RBCDocument20 pagesSM PPT RBCAnkita KumariNo ratings yet

- Field Study ProposaL - Feb 10 2020Document10 pagesField Study ProposaL - Feb 10 2020Simran KaurNo ratings yet

- EY Global Consumer Banking Survey 2014Document48 pagesEY Global Consumer Banking Survey 2014ohmygodNo ratings yet

- Assignment: 1 International Human Resources ManagementDocument2 pagesAssignment: 1 International Human Resources ManagementAsm TowheedNo ratings yet

- Sampling of Geosynthetics For TestingDocument3 pagesSampling of Geosynthetics For TestingEdmundo Jaita CuellarNo ratings yet

- Chapter 6 Security AnalysisDocument46 pagesChapter 6 Security AnalysisAshraf KhamisaNo ratings yet

- 4.2 Process CapacityDocument11 pages4.2 Process Capacitysaheb167No ratings yet

- Anu Ujin Bat Erdene CV Resume PDFDocument1 pageAnu Ujin Bat Erdene CV Resume PDFAnuUjin BatErdeneNo ratings yet

- Lazada Seller Center 5Document39 pagesLazada Seller Center 5Mohd Wildan Amir MusaNo ratings yet

- Ujwala N Jagdale and Ors Vs Jagdale Industries PriNC201723061716192583COM45336Document8 pagesUjwala N Jagdale and Ors Vs Jagdale Industries PriNC201723061716192583COM45336Aryan AnandNo ratings yet

- Lecture 2 Kaizen Continuous Improvement - 3Document53 pagesLecture 2 Kaizen Continuous Improvement - 3mannoqamarNo ratings yet

- Ratio Rate ProportionDocument1 pageRatio Rate Proportionfile.kurniawanNo ratings yet

- A Book For Advertising Warriors: How To Make A Benta by Greg B. MacabentaDocument2 pagesA Book For Advertising Warriors: How To Make A Benta by Greg B. MacabentaLorna Dietz100% (1)

- Bull Whip Effect ASsignmentDocument5 pagesBull Whip Effect ASsignmentSajjad HanifNo ratings yet

- Maritime ClusterDocument189 pagesMaritime ClusterTRISTIANDINDA PERMATANo ratings yet

- MDI Graduation Booklet October 2015 Updated Aslani BioDocument20 pagesMDI Graduation Booklet October 2015 Updated Aslani BioAli MraniNo ratings yet

- Portfolio of Telenor Pakistan: HistoryDocument3 pagesPortfolio of Telenor Pakistan: HistoryRamis Raza XaidiNo ratings yet

- Manifesto Metamorphosis of The Ghana Football Association by Aspirant For The GFA Elections AMANDA CLINTONDocument8 pagesManifesto Metamorphosis of The Ghana Football Association by Aspirant For The GFA Elections AMANDA CLINTONKweku Zurek100% (3)

- Admitting Is Gold! Randy RayDocument19 pagesAdmitting Is Gold! Randy RayDaniel WaruguruNo ratings yet

- Profit Volume ChartDocument10 pagesProfit Volume ChartAnonymous 0HycR53No ratings yet

- Ankur Mathur IIPM ResumeDocument3 pagesAnkur Mathur IIPM Resumesarabjitsingh123No ratings yet

- Privatization of Public ServiceDocument41 pagesPrivatization of Public Servicedexie de guzmanNo ratings yet

- Alex Popescu CVDocument8 pagesAlex Popescu CVi.alexpopescuNo ratings yet

- PartnershipDocument8 pagesPartnershipOllie WattsNo ratings yet

- Operations Management - Capacity Planning and Control Sample PDFDocument3 pagesOperations Management - Capacity Planning and Control Sample PDFQuincy RileyNo ratings yet

- BritanniaDocument49 pagesBritanniaParinNo ratings yet

- 16 Best COO Books To Read in 2023Document21 pages16 Best COO Books To Read in 2023NAGARAJU MOTUPALLINo ratings yet

- Information System Management of Idea Cellular Ltd.Document25 pagesInformation System Management of Idea Cellular Ltd.my frnd ganesha100% (1)

- 03 - Review of Literature PDFDocument8 pages03 - Review of Literature PDFJaspal AroraNo ratings yet

- Pearson Edexcel Gcse Business 2021 Paper1 Questionpaper NewformatDocument24 pagesPearson Edexcel Gcse Business 2021 Paper1 Questionpaper NewformatMiri AmeeNo ratings yet