You might also like

- Introduction To Project Report:: Shiva Credit Co-Operative Society LimitedDocument83 pagesIntroduction To Project Report:: Shiva Credit Co-Operative Society Limitedpmcmbharat264100% (1)

- Comparative Study Between Two Co-Opertive BankDocument47 pagesComparative Study Between Two Co-Opertive BankParag More71% (7)

- A STUDY OF ACCOUNTING AND STATUTORY REQUIREMENT OF SAI KRUPA C.H.S (Nerul East)Document29 pagesA STUDY OF ACCOUNTING AND STATUTORY REQUIREMENT OF SAI KRUPA C.H.S (Nerul East)Pankaj Rathod67% (3)

- Co Operative Banking Final ProjectDocument65 pagesCo Operative Banking Final ProjectYogi525No ratings yet

- Chapter-2 Review of Literature: Bhatia (1978), in His Study Titled, "Banking Structure and Performance A CaseDocument28 pagesChapter-2 Review of Literature: Bhatia (1978), in His Study Titled, "Banking Structure and Performance A CaseApoorvaNo ratings yet

- Co Operative Banking ProjectDocument55 pagesCo Operative Banking ProjectlizamandevNo ratings yet

- Summer Report On H.P. State Cooperative BankDocument61 pagesSummer Report On H.P. State Cooperative BankVIKAS DOGRA71% (7)

- Industry ProfileDocument15 pagesIndustry ProfileP.Anandha Geethan80% (5)

- Finacial Analysis of Nagpur Nagrik Sahakari Bank 100Document77 pagesFinacial Analysis of Nagpur Nagrik Sahakari Bank 100Shriya MehrotraNo ratings yet

- Internship Report On Kanchepuram Central Cooperative BankDocument28 pagesInternship Report On Kanchepuram Central Cooperative BankSanjay Soupboy50% (2)

- Comparative Between Commercial Bank and Co Operative BankDocument39 pagesComparative Between Commercial Bank and Co Operative BankSoundari Nadar100% (3)

- Major Project (Akhil.k)Document116 pagesMajor Project (Akhil.k)Vinoth Vkr75% (4)

- Saran Blackbook FinalDocument78 pagesSaran Blackbook FinalVishnuNadar100% (3)

- Punjab State Cooperative Bank 1 (Repaired)Document60 pagesPunjab State Cooperative Bank 1 (Repaired)DeepikaSaini75% (4)

- Internship ReportDocument21 pagesInternship ReportShabna33% (3)

- Urban Co-Operative BankDocument96 pagesUrban Co-Operative BankAshutoshSharma0% (1)

- Co Operative Banking ProjectDocument55 pagesCo Operative Banking Projectamit9_prince91% (11)

- Project ReportDocument57 pagesProject Reportadi6187100% (1)

- Co OperativeDocument220 pagesCo OperativeMeenukutty MeenuNo ratings yet

- Co Operative BankDocument76 pagesCo Operative BankGursharan Singh Anamika0% (1)

- Report On Sutex BankDocument55 pagesReport On Sutex Bankjkpatel221No ratings yet

- Project On Co-Operative Banks and Rural DevelopmentDocument52 pagesProject On Co-Operative Banks and Rural DevelopmentDileep94% (17)

- Report On Organisation Study Cover Page1 DeekshaDocument51 pagesReport On Organisation Study Cover Page1 Deekshadeeksha jNo ratings yet

- Synopsis On SbiDocument9 pagesSynopsis On SbiAyush Tiwari100% (1)

- Enjoy Fun Foods LTD, GokakDocument16 pagesEnjoy Fun Foods LTD, GokakAbhishek M TalawarNo ratings yet

- Summer Training Project Report COPERATIVE BANKDocument53 pagesSummer Training Project Report COPERATIVE BANKkaushal24420% (1)

- 3.1 Industry Profile 3.1.1 Banking Industry in IndiaDocument25 pages3.1 Industry Profile 3.1.1 Banking Industry in IndiaUma MaheshwariNo ratings yet

- CAMELS Project of Axis BankDocument47 pagesCAMELS Project of Axis Bankjatinmakwana90No ratings yet

- Sutex Co-Op Bank ProjectDocument49 pagesSutex Co-Op Bank ProjectHinal Prajapati100% (4)

- Role of Urban Cooperative Bank in Banking SectorDocument60 pagesRole of Urban Cooperative Bank in Banking SectorbluechelseanNo ratings yet

- Introduction of The Study: Meaning and Importance of FinanceDocument69 pagesIntroduction of The Study: Meaning and Importance of FinanceJeevitha MuruganNo ratings yet

- Co Operative BankDocument20 pagesCo Operative BankRakesh RockyNo ratings yet

- Kovaidccb Project Report FinalDocument42 pagesKovaidccb Project Report FinalNandakumar KsNo ratings yet

- An Assignment On Indian Banking SystemDocument19 pagesAn Assignment On Indian Banking Systemjourneyis life100% (2)

- Cooperative Banking ProjectDocument53 pagesCooperative Banking ProjectselvamNo ratings yet

- Siddheswar Co-Operative Bank LTD, BijapurDocument63 pagesSiddheswar Co-Operative Bank LTD, Bijapurarunsavukar100% (2)

- TNSC ProfileDocument6 pagesTNSC Profilesuse203750% (2)

- History of Co-Operative Credit Society in IndiaDocument14 pagesHistory of Co-Operative Credit Society in IndiaTerry YanamNo ratings yet

- Varchha Bank ReportDocument79 pagesVarchha Bank ReportSatish Prajapati33% (3)

- Banking Project Topics-2Document4 pagesBanking Project Topics-2Mike KukrejaNo ratings yet

- Bank Project FinalDocument23 pagesBank Project Finalgoudarameshv100% (1)

- Union Bank of IndiaDocument33 pagesUnion Bank of Indiaraghavan swaminathanNo ratings yet

- Review of LiteratureDocument8 pagesReview of LiteratureFurkan BelimNo ratings yet

- Co-Operative Banks: NKGSB Co-Op Bank LTDDocument33 pagesCo-Operative Banks: NKGSB Co-Op Bank LTDFaiz Bakali100% (2)

- Summer Internship Report On Chengalpattu Urban BankDocument29 pagesSummer Internship Report On Chengalpattu Urban BankAliasgar Patanwala40% (5)

- Balasore Cooperative BankDocument44 pagesBalasore Cooperative Bankmir musaweer ali100% (1)

- Project Cooperative BankDocument33 pagesProject Cooperative BankPradeepPrinceraj100% (1)

- Project On Punjab National BankDocument86 pagesProject On Punjab National BankPrakash Singh100% (1)

- Organizational Study of The Perla Service Co-Operative Bank LTD No.c 3377Document37 pagesOrganizational Study of The Perla Service Co-Operative Bank LTD No.c 3377Fathima LibaNo ratings yet

- A Project Report ON "Customer Preference and Satisfaction Level For Credit Schemes Offered by The Varachha Co-Operative Bank"Document109 pagesA Project Report ON "Customer Preference and Satisfaction Level For Credit Schemes Offered by The Varachha Co-Operative Bank"Ankit Malani100% (1)

- NPA Project ReportDocument78 pagesNPA Project ReportAman RajputNo ratings yet

- CooperationDocument10 pagesCooperationNEERAJA UNNINo ratings yet

- Philosophy The Concept of Co-Operation The StrengthDocument3 pagesPhilosophy The Concept of Co-Operation The StrengthroyalchandNo ratings yet

- Chapter - 1Document18 pagesChapter - 1karandeep singhNo ratings yet

- Co-Operative Theory and Practice: Chapter 1 - Introduction To Co-OperationDocument8 pagesCo-Operative Theory and Practice: Chapter 1 - Introduction To Co-OperationVijay KrishnanNo ratings yet

- 09 - Chapter 1Document27 pages09 - Chapter 1Delete SinghNo ratings yet

- Masters' Notes For Co-Op ManagementDocument47 pagesMasters' Notes For Co-Op Managementemerald computersNo ratings yet

- Paper - 1 - Environment For Cooperatives & Rural DevelopmentDocument206 pagesPaper - 1 - Environment For Cooperatives & Rural Developmentbala badhraNo ratings yet

- Project Report HRDocument39 pagesProject Report HRManoj SharmaNo ratings yet

- 07 - Chapter 2Document40 pages07 - Chapter 2Aakash DebnathNo ratings yet

- Score Booster For All Bank Prelims Exams Day 254Document28 pagesScore Booster For All Bank Prelims Exams Day 254Pawan DeepNo ratings yet

- FRM Sample QuestionsDocument9 pagesFRM Sample QuestionsTony0% (1)

- Heirs of Tantoco v. CADocument10 pagesHeirs of Tantoco v. CAevelyn b t.No ratings yet

- Zarai Taraqiati Bank Limited VisionDocument4 pagesZarai Taraqiati Bank Limited VisionAhmad MalikNo ratings yet

- Contemporary Issues in Indian Insurance MarketingDocument16 pagesContemporary Issues in Indian Insurance MarketingPravin SundvaishaNo ratings yet

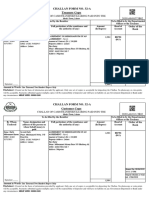

- Challan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into TheDocument1 pageChallan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into TheHafiz ImranNo ratings yet

- 2011 Supreme Court Decisions On Commercial LawDocument9 pages2011 Supreme Court Decisions On Commercial LawMartin MartelNo ratings yet

- Characteristics of The Money MarketDocument8 pagesCharacteristics of The Money Marketshubhmeshram2100No ratings yet

- Union Bank Company Profile: Brief HistoryDocument4 pagesUnion Bank Company Profile: Brief HistoryMark Philip AldabaNo ratings yet

- Fuqua Casebook 2019-2020 PDFDocument244 pagesFuqua Casebook 2019-2020 PDFSashi Shankar100% (7)

- Askari AssignmentDocument7 pagesAskari AssignmentSabih TariqNo ratings yet

- Affidavit of BankingDocument2 pagesAffidavit of BankingArlin J. Wallace100% (1)

- Citibanks Indian Business ModelDocument14 pagesCitibanks Indian Business ModeljeganrajrajNo ratings yet

- Faculty of Commerce Department of Business ManagementDocument17 pagesFaculty of Commerce Department of Business ManagementInnocent TakorekanaNo ratings yet

- Railway Train Ticket Generation Through ATM Machine: A Business Application For Indian RailwaysDocument5 pagesRailway Train Ticket Generation Through ATM Machine: A Business Application For Indian RailwaysSatish ChavanNo ratings yet

- Introduction To Securitization: Stuart M. Litwin Mayer, Brown, Rowe & Maw LLPDocument65 pagesIntroduction To Securitization: Stuart M. Litwin Mayer, Brown, Rowe & Maw LLPVipin GuptaNo ratings yet

- Arithmetic Sequence 2Document3 pagesArithmetic Sequence 2Ana Cristina SanchezNo ratings yet

- Retail Banking Sample Questions by Murugan-June 19 ExamsDocument193 pagesRetail Banking Sample Questions by Murugan-June 19 ExamsN Mahesh0% (1)

- Exim BankDocument79 pagesExim Banklaxmi sambre0% (1)

- Prospects of Digital Banking in BangladeshDocument6 pagesProspects of Digital Banking in BangladeshSayemNo ratings yet

- Gomal University: Journal of ResearchDocument13 pagesGomal University: Journal of ResearchsdsNo ratings yet

- Leac201 PDFDocument73 pagesLeac201 PDFSubhamoy PradhanNo ratings yet

- Martha S. Poe, Individually and As of The Estate of Ansel Poe, Deceased, and Ansel Poe & Associates, Inc. v. The First National Bank of Dekalb County, 597 F.2d 895, 1st Cir. (1979)Document3 pagesMartha S. Poe, Individually and As of The Estate of Ansel Poe, Deceased, and Ansel Poe & Associates, Inc. v. The First National Bank of Dekalb County, 597 F.2d 895, 1st Cir. (1979)Scribd Government DocsNo ratings yet

- Loan and Advances of Rupali Bank LimitedDocument55 pagesLoan and Advances of Rupali Bank Limitedhomaira40% (5)

- Idbi Federal InsuranceDocument37 pagesIdbi Federal InsuranceJanani Rani100% (1)

- Income From Other SourcesDocument15 pagesIncome From Other SourcesBhuvaneswari karuturiNo ratings yet

- SBI Launches New Scheme For NPA SettlementDocument2 pagesSBI Launches New Scheme For NPA Settlementelinakanungo83425450% (2)

- Newest Offshore To Offshore Pounds Cheque (PEDRO) - 560-GBP-1Document6 pagesNewest Offshore To Offshore Pounds Cheque (PEDRO) - 560-GBP-1Wallet LeoNo ratings yet

- Vak Jan. 17 PDFDocument28 pagesVak Jan. 17 PDFMuralidharan78% (9)

- Coface Handbook Country Risk 2017Document241 pagesCoface Handbook Country Risk 2017David CumbajinNo ratings yet