You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- PayGate PayWebv2 v1.15Document23 pagesPayGate PayWebv2 v1.15gmk0% (1)

- WCAMLF 2019 Distribution ListDocument11 pagesWCAMLF 2019 Distribution ListShubendu DeyNo ratings yet

- Bank Payment ObligationDocument8 pagesBank Payment ObligationKhan Majlis ReshadNo ratings yet

- Reyes Vs Grey, Bautista Vs MarcosDocument4 pagesReyes Vs Grey, Bautista Vs MarcosRZ ZamoraNo ratings yet

- E Frauds in BankingDocument5 pagesE Frauds in BankingRajivNo ratings yet

- BillDocument11 pagesBillKat SriramNo ratings yet

- Railway Establishment RulesDocument127 pagesRailway Establishment Rulesjijina100% (1)

- As We All Are AwareDocument17 pagesAs We All Are AwaremgrfanNo ratings yet

- NCPAR Sample Review QuestionsDocument7 pagesNCPAR Sample Review QuestionsJonathan Tumamao FernandezNo ratings yet

- IFR Magazine - June 13, 2020Document114 pagesIFR Magazine - June 13, 2020Gaby LopezNo ratings yet

- Central Bank of India: New Business GroupDocument7 pagesCentral Bank of India: New Business GroupAbhishek BoseNo ratings yet

- Downloads-Examination Centre List For Aug Sep 2012Document7 pagesDownloads-Examination Centre List For Aug Sep 2012Patrick AdamsNo ratings yet

- Richard M Gergel Financial Disclosure Report For Gergel, Richard MDocument16 pagesRichard M Gergel Financial Disclosure Report For Gergel, Richard MJudicial Watch, Inc.No ratings yet

- Noda Vs Cruz-Arnaldo 1987Document2 pagesNoda Vs Cruz-Arnaldo 1987Krizzia GojarNo ratings yet

- Barkatullah Vishwavidyalaya Migration Cert - Format FilledupDocument5 pagesBarkatullah Vishwavidyalaya Migration Cert - Format FilledupRojukurthi SudhakarNo ratings yet

- Infosys Finacle Overview 101202224911 Phpapp01Document8 pagesInfosys Finacle Overview 101202224911 Phpapp01Alexander WeaverNo ratings yet

- Elliott Wave Analysis Works Like Magic PDFDocument6 pagesElliott Wave Analysis Works Like Magic PDFpmg3067100% (1)

- Chapter 13 The Human Resources Management and Payroll CycleDocument67 pagesChapter 13 The Human Resources Management and Payroll CycleislamelshahatNo ratings yet

- Peoples Bank Vs Dahican Lumber DigestDocument2 pagesPeoples Bank Vs Dahican Lumber DigestNOLLIE CALISINGNo ratings yet

- Nit inDocument2 pagesNit inNitin ChauhanNo ratings yet

- Brosur Pinjaman Bank CIMB NIAGA November 2019Document1 pageBrosur Pinjaman Bank CIMB NIAGA November 2019Abdan SyakuroNo ratings yet

- Assessing Fund Performance:: Using Benchmarks in Venture CapitalDocument13 pagesAssessing Fund Performance:: Using Benchmarks in Venture CapitalNamek Zu'biNo ratings yet

- Daftar DisporaDocument10 pagesDaftar DisporaElena RosintaNo ratings yet

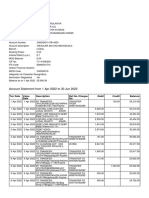

- Account Statement From 1 Apr 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesAccount Statement From 1 Apr 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceParveen SainiNo ratings yet

- RTGS NEFT Multiple Transaction FormDocument2 pagesRTGS NEFT Multiple Transaction FormElegante World50% (2)

- QestionnaireDocument4 pagesQestionnairePreet AmanNo ratings yet

- Acc Project 2021 22Document14 pagesAcc Project 2021 22Piyush GoyalNo ratings yet

- Case StudyDocument8 pagesCase StudyGideon KimariNo ratings yet

- Sec. 99 A Reinsurance Is Presumed To Be A Contract of Indemnity Against Liability, and Not Merely Against DamageDocument2 pagesSec. 99 A Reinsurance Is Presumed To Be A Contract of Indemnity Against Liability, and Not Merely Against DamageFlorena CayundaNo ratings yet

- Untitled 1Document1,318 pagesUntitled 1Dence Cris RondonNo ratings yet