You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

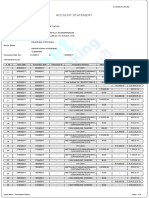

- Account Statement: Transactions ListDocument4 pagesAccount Statement: Transactions Listtawhide_islamicNo ratings yet

- Complete Accounting Cycle ExerciseDocument28 pagesComplete Accounting Cycle ExerciseBrian Dillard94% (17)

- Best in Class Practices - Procure To PayDocument31 pagesBest in Class Practices - Procure To PayAmaldev VasudevanNo ratings yet

- SCM - Session 4 Midwest Office ProductsDocument2 pagesSCM - Session 4 Midwest Office ProductsAbhishek MalhotraNo ratings yet

- Card Premium Bank Open Up For ACH and DD Carder404updateeDocument3 pagesCard Premium Bank Open Up For ACH and DD Carder404updateeoriarector782No ratings yet

- DOA DKC - PCW 50B TT WIDNIREX SP.Z.O.O George Bernard Teichner PDFDocument15 pagesDOA DKC - PCW 50B TT WIDNIREX SP.Z.O.O George Bernard Teichner PDFChika ChikaNo ratings yet

- Krajewski Ism Ch15Document28 pagesKrajewski Ism Ch15echykcytcs67% (3)

- Db-799pof+999-77m-Ecoucd Usa-Raiff-Albania-171117Document2 pagesDb-799pof+999-77m-Ecoucd Usa-Raiff-Albania-171117almawest.llpNo ratings yet

- CPRI Compression (5G RAN6.1 - Draft A)Document41 pagesCPRI Compression (5G RAN6.1 - Draft A)VVLNo ratings yet

- FeeReceipts PrintFeeReceiptParentDocument1 pageFeeReceipts PrintFeeReceiptParentPuneet ChandraNo ratings yet

- One Liner OctDocument18 pagesOne Liner OctPuneet ChandraNo ratings yet

- Niti AyogDocument1 pageNiti AyogPuneet ChandraNo ratings yet

- Pitch Report - BMSB PO 2015-16: Subject No. QSN MarksDocument2 pagesPitch Report - BMSB PO 2015-16: Subject No. QSN MarksPuneet ChandraNo ratings yet

- Interview It Officer Exam SSC CGL Day Date Interview IT Officer SSC CGL 1 9.00-4.00 PM 5.00-7.00 PM 8.00-12.00 2 3 4 5 6 7 8 9 10Document1 pageInterview It Officer Exam SSC CGL Day Date Interview IT Officer SSC CGL 1 9.00-4.00 PM 5.00-7.00 PM 8.00-12.00 2 3 4 5 6 7 8 9 10Puneet ChandraNo ratings yet

- 18 September 2014 Current AffairsDocument2 pages18 September 2014 Current AffairsPuneet ChandraNo ratings yet

- Syllabus BDocument356 pagesSyllabus BNelson NingombamNo ratings yet

- Ppf... Vasu StatementDocument2 pagesPpf... Vasu StatementVasu AmmuluNo ratings yet

- 5G TutorialDocument29 pages5G TutorialaseaudiNo ratings yet

- Direct Deposit Authorization Form - Controlled PDFDocument2 pagesDirect Deposit Authorization Form - Controlled PDFNatilee CampbellNo ratings yet

- Excel FormatDocument38 pagesExcel FormatSaad QureshiNo ratings yet

- LDP md5Document4 pagesLDP md5kyi lwinNo ratings yet

- Moxa Ring Coupling For A Turbo Ring Tech Note v1.0Document5 pagesMoxa Ring Coupling For A Turbo Ring Tech Note v1.0malaka gamageNo ratings yet

- Lembar Kerja Jurnal Ud SentosaDocument11 pagesLembar Kerja Jurnal Ud SentosaMuhammad SandyNo ratings yet

- FAQ Unifi Air - For Consumer - Website Update - 23032020Document6 pagesFAQ Unifi Air - For Consumer - Website Update - 23032020RAZALI BIN AHMAD MoeNo ratings yet

- MPLS-TP: © Tejas Networks Confidential and Proprietary Software Enabled TransformationDocument42 pagesMPLS-TP: © Tejas Networks Confidential and Proprietary Software Enabled TransformationShubham VishwakarmaNo ratings yet

- Yeastar S-Series Voip PBX: Performance and PowerDocument2 pagesYeastar S-Series Voip PBX: Performance and PowerJeronimo ReynosoNo ratings yet

- CMD CommandsDocument27 pagesCMD CommandsAbhishek gargNo ratings yet

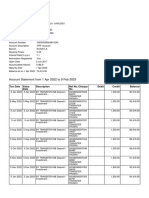

- Acct Statement - XX7952 - 09022023Document21 pagesAcct Statement - XX7952 - 09022023Sagar PatilNo ratings yet

- BL Sub7919120700005 PDFDocument1 pageBL Sub7919120700005 PDFRicky RezaNo ratings yet

- Ecommerce MRTDocument43 pagesEcommerce MRTDominador De GuzmanNo ratings yet

- Raritan Pharmaceuticals Awarded 2018 Supplier of The Year at Walmart CanadaDocument2 pagesRaritan Pharmaceuticals Awarded 2018 Supplier of The Year at Walmart CanadaPR.comNo ratings yet

- Eastwest Practical Mastercard Sample Interest Computation: ST THDocument1 pageEastwest Practical Mastercard Sample Interest Computation: ST THMalabanan-Fulgencio Pauline KristineNo ratings yet

- Presentation On Indian Postal System::-Taminder MamDocument13 pagesPresentation On Indian Postal System::-Taminder MamSantanu KararNo ratings yet

- FAP 3e 2021 PPT CH 9 Accounting For ReceivablesDocument46 pagesFAP 3e 2021 PPT CH 9 Accounting For Receivablestrinhnq22411caNo ratings yet

- 2016 05 28 DRG 2016 CompiledDocument146 pages2016 05 28 DRG 2016 CompiledmirzaNo ratings yet

- LogDocument77 pagesLogtiffanyNo ratings yet

- Specialized Portfolio Servicing Short Sale Approval - Maryville, TennesseeDocument3 pagesSpecialized Portfolio Servicing Short Sale Approval - Maryville, TennesseeknoxvilleareashortsaNo ratings yet