You might also like

- University of Mumbai: Student DeclarationDocument62 pagesUniversity of Mumbai: Student DeclarationRachana Sontakke0% (1)

- LeaseholdDocument6 pagesLeaseholdrichjohnhughesNo ratings yet

- Chapter 9 Governmental and Non-For-profit Accounting Test BankDocument16 pagesChapter 9 Governmental and Non-For-profit Accounting Test BankAngelo Mendez100% (2)

- National Stock Exchange: Financial Market Regulations Project OnDocument11 pagesNational Stock Exchange: Financial Market Regulations Project OnNehmat SethiNo ratings yet

- Nse Project WorkDocument25 pagesNse Project WorkArif Khan100% (1)

- National Stock ExchangeDocument18 pagesNational Stock Exchangeramesh_thorveNo ratings yet

- National Stock ExchangeDocument1 pageNational Stock ExchangeSachin YadavNo ratings yet

- A Presentation On National Stock ExchangeDocument10 pagesA Presentation On National Stock ExchangeMohit SuranaNo ratings yet

- Report PartDocument86 pagesReport PartPratik N. PatelNo ratings yet

- Final Pavi ProjectDocument53 pagesFinal Pavi Projectkumarpraveen42060No ratings yet

- Fact2006 Sec1Document11 pagesFact2006 Sec1meetwithsanjayNo ratings yet

- History & Formation of NSE:: Assignment No.1Document4 pagesHistory & Formation of NSE:: Assignment No.1Anil KoliNo ratings yet

- NseDocument18 pagesNseishan chughNo ratings yet

- The National Stock Exchange of India Limited (NSE) Was Incorporated in November 1992 by IDBI andDocument2 pagesThe National Stock Exchange of India Limited (NSE) Was Incorporated in November 1992 by IDBI andVidhyaa_Mano_3923No ratings yet

- The National Stock Exchange of India LimitedDocument11 pagesThe National Stock Exchange of India LimitedKaushar AlamNo ratings yet

- Assignment of SapmDocument23 pagesAssignment of Sapmanuagarwal1991No ratings yet

- Future and OptionsDocument96 pagesFuture and OptionsAnil VenkatNo ratings yet

- A Report On Visit To National Stock Exchange (Nse) DelhiDocument9 pagesA Report On Visit To National Stock Exchange (Nse) DelhiAshish KathpalNo ratings yet

- National Stock Exchange: Presented by Benson Berlin Jinshy Pranav PunyaDocument14 pagesNational Stock Exchange: Presented by Benson Berlin Jinshy Pranav Punyapranav sharmaNo ratings yet

- "A Comparative Study of Nse &bse": A Project Report ONDocument56 pages"A Comparative Study of Nse &bse": A Project Report ONShailendra Bhatt0% (2)

- Im Module 5 NotesDocument25 pagesIm Module 5 NotesJauhar Ul HaqNo ratings yet

- Presentation ON Stock Exchange Operation: Presented By: Bharat BalduaDocument18 pagesPresentation ON Stock Exchange Operation: Presented By: Bharat BalduaBharat Baldua100% (1)

- NseDocument23 pagesNsesagar22samNo ratings yet

- Project Report On Indian Stock Market - DBFSDocument100 pagesProject Report On Indian Stock Market - DBFSkartikNo ratings yet

- Presentation ON Stock Exchange Operation: Presented By: Bharat BalduaDocument18 pagesPresentation ON Stock Exchange Operation: Presented By: Bharat BalduaNilesh MandlikNo ratings yet

- Chapter 1 NewDocument21 pagesChapter 1 NewAnshu GirdharNo ratings yet

- Mba Trading CapitalDocument20 pagesMba Trading CapitalDinesh RamawatNo ratings yet

- Chapter - IDocument42 pagesChapter - IAasim KhanNo ratings yet

- Online TradingDocument50 pagesOnline TradingKeleti SanthoshNo ratings yet

- Camaprative Study of NSE and BSE PDFDocument100 pagesCamaprative Study of NSE and BSE PDFsobha singhNo ratings yet

- Working On National Stock Exchange - IIFLDocument19 pagesWorking On National Stock Exchange - IIFLMohmmed KhayyumNo ratings yet

- Assignment Smo Stock ExchangeDocument4 pagesAssignment Smo Stock ExchangeYadwinder SinghNo ratings yet

- IIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER ADocument88 pagesIIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER AVajir BajiNo ratings yet

- Nothing Is Wrong With Undertaking Risky Investments As Long As The Investor Understands The Possible Consequences.Document8 pagesNothing Is Wrong With Undertaking Risky Investments As Long As The Investor Understands The Possible Consequences.Richa GoenkaNo ratings yet

- 08 Chapter 1Document42 pages08 Chapter 1motivational videosNo ratings yet

- National Stock Exchange (NSE) of IndiaDocument5 pagesNational Stock Exchange (NSE) of IndialalitbadogaNo ratings yet

- National Stock Exchange of India LTD.: Leadership Through ChangeDocument2 pagesNational Stock Exchange of India LTD.: Leadership Through Changebhaveshkpatel2003No ratings yet

- National Stock ExchangeDocument23 pagesNational Stock Exchangemanishgondhalekar100% (6)

- Industry Overview: Chapter - 1Document36 pagesIndustry Overview: Chapter - 1Rahul VermaNo ratings yet

- The Surat People's College of Business Administration: Presentation On NSE (National Stock Exchange)Document15 pagesThe Surat People's College of Business Administration: Presentation On NSE (National Stock Exchange)nileshkukadiyaNo ratings yet

- TechnologyDocument16 pagesTechnologysuppishikhaNo ratings yet

- Project Report ON Comparative Study OFDocument80 pagesProject Report ON Comparative Study OFBishnu RoyNo ratings yet

- Management Revised SyllabusDocument19 pagesManagement Revised SyllabuskanikaNo ratings yet

- Basis Termin Share MarketDocument31 pagesBasis Termin Share MarketNikNo ratings yet

- InnovationsDocument4 pagesInnovationsMousami BanerjeeNo ratings yet

- Main SynopsisDocument6 pagesMain SynopsisKhushboo S. BrahmankarNo ratings yet

- A Report On National Stock Exchange (Nse)Document22 pagesA Report On National Stock Exchange (Nse)vishaltiwari.21No ratings yet

- SSRN Id2712104Document11 pagesSSRN Id2712104Dhanusg veerNo ratings yet

- "A Comparative Study On NSE & BSE": Mohammad Riyaz Shaikh, Sakriya Nikunj, Patel Yash, Patel FenilDocument8 pages"A Comparative Study On NSE & BSE": Mohammad Riyaz Shaikh, Sakriya Nikunj, Patel Yash, Patel FenilNandita IyerNo ratings yet

- Analysis NSEDocument67 pagesAnalysis NSEMukul RamaniNo ratings yet

- Call Money MarketDocument15 pagesCall Money MarketVatsav GundigaraNo ratings yet

- BSM Project (Stock Exchange)Document15 pagesBSM Project (Stock Exchange)PowerPoint GoNo ratings yet

- Grade Xii FMMDocument11 pagesGrade Xii FMMGulnaz Parveen100% (2)

- Indian Stock MarketDocument24 pagesIndian Stock MarketGRAMY TRADERS SALEMNo ratings yet

- College ReportDocument83 pagesCollege Reportanil_kumar_440No ratings yet

- Organized Stock Exchange and Its FunctionsDocument6 pagesOrganized Stock Exchange and Its Functionsanna merlin sunnyNo ratings yet

- Indian Stock MarketDocument48 pagesIndian Stock MarketAbhay JainNo ratings yet

- Definition of Stock ExchangeDocument21 pagesDefinition of Stock ExchangeSrinu UdumulaNo ratings yet

- History of BSEDocument5 pagesHistory of BSEapuoctNo ratings yet

- Use of Financial Management Information Systems To Improve Financial Management and Accountability in The Public SectorDocument12 pagesUse of Financial Management Information Systems To Improve Financial Management and Accountability in The Public SectorInternational Consortium on Governmental Financial Management100% (13)

- BA 114.1 Handout On PPEDocument5 pagesBA 114.1 Handout On PPEHuarde SophiaNo ratings yet

- Tugas AKL P1-3Document14 pagesTugas AKL P1-3bagong kussetNo ratings yet

- Cox's Bazar International University: Submitted byDocument10 pagesCox's Bazar International University: Submitted byKhanNo ratings yet

- Shubham RaniDocument6 pagesShubham RaniSanchay BhararaNo ratings yet

- Conceptual Framework of Camel Analysis: Chapter-1Document11 pagesConceptual Framework of Camel Analysis: Chapter-1poojaNo ratings yet

- Terms of Reference MFADocument2 pagesTerms of Reference MFAKEEVINNo ratings yet

- Problem 1-1 To 1-3 Intermediate Accounting (Vol 1)Document8 pagesProblem 1-1 To 1-3 Intermediate Accounting (Vol 1)Margarette TumbadoNo ratings yet

- Global Dealmakers 2022:: M&A Market UpdateDocument17 pagesGlobal Dealmakers 2022:: M&A Market UpdateszhaNo ratings yet

- Exercise InvestmentsDocument14 pagesExercise InvestmentsAlizah Lariosa Bucot43% (7)

- Difference Between Management Accounting and Financial AccountingDocument3 pagesDifference Between Management Accounting and Financial AccountingRoshani ChaudhariNo ratings yet

- Diploma in IFRS (Level 1 and 2) : Your Passport To Financial Reporting ExcellenceDocument8 pagesDiploma in IFRS (Level 1 and 2) : Your Passport To Financial Reporting ExcellenceMuhammad Imran JehangirNo ratings yet

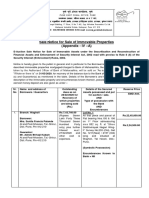

- Sale Notice For Sale of Immovable Properties (Appendix - IV - A)Document7 pagesSale Notice For Sale of Immovable Properties (Appendix - IV - A)Nikhil ShindeNo ratings yet

- Print 1stDocument1 pagePrint 1stChristine Marie RamirezNo ratings yet

- Ratio, Likuiditas, Profitabilitas, Dan Ukuran PerusahaanDocument18 pagesRatio, Likuiditas, Profitabilitas, Dan Ukuran PerusahaanCheri PutriNo ratings yet

- Currency WarsDocument118 pagesCurrency WarsCarnegie Endowment for International Peace83% (6)

- Financial InclusionDocument42 pagesFinancial InclusionNeeta PaiNo ratings yet

- Introduction To Finance: Group Name: The Financial FittersDocument20 pagesIntroduction To Finance: Group Name: The Financial FittersMonera Bhuiyan MimNo ratings yet

- TAX 401 Percentage Tax Part 1Document7 pagesTAX 401 Percentage Tax Part 1Juan Miguel UngsodNo ratings yet

- Palgrave Catalogue Banking FinanceDocument40 pagesPalgrave Catalogue Banking FinanceHadi SumartonoNo ratings yet

- Sample AssignmentDocument45 pagesSample AssignmentfahadNo ratings yet

- Manajemen Ruang Lingkup ITDocument49 pagesManajemen Ruang Lingkup ITSondang Rohmulia SinagaNo ratings yet

- Quiz 3 ADocument4 pagesQuiz 3 AArooj ImranNo ratings yet

- Financial Analysis On Axis BankDocument8 pagesFinancial Analysis On Axis BankNIKHIL PATTNAIKNo ratings yet

- Mawjihan Tsakilla 023001701045 710:13.15 Selpita&LisnaDocument8 pagesMawjihan Tsakilla 023001701045 710:13.15 Selpita&Lisnaadis salsabilaNo ratings yet

- EarnstatementsDocument4 pagesEarnstatementsRafael LeonidesNo ratings yet

- Risk Management Dissertation PDFDocument8 pagesRisk Management Dissertation PDFHelpWithCollegePaperWritingUK100% (1)

- MT FreshDocument5 pagesMT FreshMechergui RamiNo ratings yet