You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Canada Federal CourtDocument27 pagesCanada Federal Courtrupesh.srivastavaNo ratings yet

- Partnership Agreement On InvestmentDocument13 pagesPartnership Agreement On InvestmentAnne Marie-NicholsonNo ratings yet

- San MiguelDocument9 pagesSan MiguelAngel Buitizon100% (1)

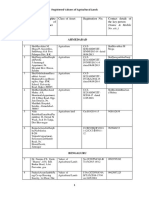

- All India List of Registered Valuers of Different Classes of AssetsDocument55 pagesAll India List of Registered Valuers of Different Classes of Assetsrupesh.srivastavaNo ratings yet

- All India List of Registered Valuers of Different Classes of AssetsDocument55 pagesAll India List of Registered Valuers of Different Classes of Assetsrupesh.srivastavaNo ratings yet

- Bank Audit Check List & Procedure (Concurrent Audit) : IndexDocument12 pagesBank Audit Check List & Procedure (Concurrent Audit) : IndexCA Jay ThakurNo ratings yet

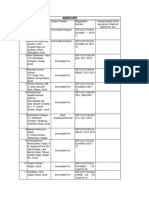

- All India List of Registered Valuers of Different Classes of AssetsDocument292 pagesAll India List of Registered Valuers of Different Classes of Assetsrupesh.srivastava50% (2)

- All India List of Registered Valuers of Different Classes of AssetsDocument292 pagesAll India List of Registered Valuers of Different Classes of Assetsrupesh.srivastava50% (2)

- LC PC ConfigurationDocument2 pagesLC PC ConfigurationmoorthykemNo ratings yet

- Aadhaar Dynamics of Digital Identity 19082016Document17 pagesAadhaar Dynamics of Digital Identity 19082016Harathi VageeshanNo ratings yet

- All India List of Registered Valuers of Different Classes of AssetsDocument92 pagesAll India List of Registered Valuers of Different Classes of Assetsrupesh.srivastavaNo ratings yet

- All India List of Registered Valuers of Different Classes of AssetsDocument92 pagesAll India List of Registered Valuers of Different Classes of Assetsrupesh.srivastavaNo ratings yet

- All India List of Registered Valuers of Different Classes of AssetsDocument11 pagesAll India List of Registered Valuers of Different Classes of Assetsrupesh.srivastavaNo ratings yet

- Invoice RelianceDigitalDocument1 pageInvoice RelianceDigitalspandyno1No ratings yet

- M S Geodis India PVT LTDDocument2 pagesM S Geodis India PVT LTDrupesh.srivastavaNo ratings yet

- M/s Shiv Vani Oil & Gas Exploration Services LTD Vs Income Tax Office (ITO)Document21 pagesM/s Shiv Vani Oil & Gas Exploration Services LTD Vs Income Tax Office (ITO)rupesh.srivastavaNo ratings yet

- Definition of "Employee" U/s 2 (F) of The EPF ActDocument17 pagesDefinition of "Employee" U/s 2 (F) of The EPF Actrupesh.srivastavaNo ratings yet

- MODERN TRANSPORTATION CONSULTATION SERVICES PVT. LTD. & ANR Vs CENTRAL PROVIDENT FUND COMMISSIONER EMPLOYEES PROVIDENT FUND ORGANISATION & ORSDocument30 pagesMODERN TRANSPORTATION CONSULTATION SERVICES PVT. LTD. & ANR Vs CENTRAL PROVIDENT FUND COMMISSIONER EMPLOYEES PROVIDENT FUND ORGANISATION & ORSrupesh.srivastavaNo ratings yet

- Canadian Imperial Bank of CommerceDocument86 pagesCanadian Imperial Bank of Commercerupesh.srivastavaNo ratings yet

- The Professional Courier Vs Employees Provident Fund AppellateDocument16 pagesThe Professional Courier Vs Employees Provident Fund Appellaterupesh.srivastavaNo ratings yet

- Karnataka - Formation of Export Promotion CellsDocument4 pagesKarnataka - Formation of Export Promotion Cellsrupesh.srivastavaNo ratings yet

- KAKRAPAR ANUMATHAK KARMACHARI Vs NUCLEAR POWER CORPORATION OF INDIA LTD.Document19 pagesKAKRAPAR ANUMATHAK KARMACHARI Vs NUCLEAR POWER CORPORATION OF INDIA LTD.rupesh.srivastavaNo ratings yet

- Registered Valuers of Agricultural Land - All India List of Registered Valuers of Different Classes of Assets Registered Valuers of Agricultural LandDocument4 pagesRegistered Valuers of Agricultural Land - All India List of Registered Valuers of Different Classes of Assets Registered Valuers of Agricultural Landrupesh.srivastavaNo ratings yet

- List of Valuers of CCIT Surat Charge - All India List of Registered Valuers of Different Classes of AssetsDocument3 pagesList of Valuers of CCIT Surat Charge - All India List of Registered Valuers of Different Classes of Assetsrupesh.srivastavaNo ratings yet

- List of Valuers of CCIT Surat Charge - All India List of Registered Valuers of Different Classes of AssetsDocument3 pagesList of Valuers of CCIT Surat Charge - All India List of Registered Valuers of Different Classes of Assetsrupesh.srivastavaNo ratings yet

- Guidelines - 35 (2AB) OF IT ACT 1961 - May2014Document29 pagesGuidelines - 35 (2AB) OF IT ACT 1961 - May2014rupesh.srivastavaNo ratings yet

- Public Information OfficerDocument10 pagesPublic Information Officerrupesh.srivastavaNo ratings yet

- Registered Valuers of Agricultural Land - All India List of Registered Valuers of Different Classes of Assets Registered Valuers of Agricultural LandDocument4 pagesRegistered Valuers of Agricultural Land - All India List of Registered Valuers of Different Classes of Assets Registered Valuers of Agricultural Landrupesh.srivastavaNo ratings yet

- Fatca Ides Technical FaqsDocument17 pagesFatca Ides Technical Faqsrupesh.srivastavaNo ratings yet

- M/s Kassar Innovative Foods VS. EPFODocument3 pagesM/s Kassar Innovative Foods VS. EPFOrupesh.srivastavaNo ratings yet

- US Tax Court An Historical AnalysisDocument953 pagesUS Tax Court An Historical Analysisrupesh.srivastavaNo ratings yet

- Company: Paramount Citrus - Mexico Division Location: CD Valles, SLP - MexicoDocument2 pagesCompany: Paramount Citrus - Mexico Division Location: CD Valles, SLP - MexicoArturo Cortes MirandaNo ratings yet

- ACC 101 - Financial Accounting and Reporting 1Document14 pagesACC 101 - Financial Accounting and Reporting 1Rc RocafortNo ratings yet

- Tax Planning With Regard To Capital GainsDocument25 pagesTax Planning With Regard To Capital GainsKamraan QuadriNo ratings yet

- Circular No. 902Document10 pagesCircular No. 902jc cayananNo ratings yet

- Pepsico F&a Assignment UpdatedDocument28 pagesPepsico F&a Assignment UpdatedRatish Kumar mishraNo ratings yet

- Model Question For Account409792809472943360Document8 pagesModel Question For Account409792809472943360yugeshNo ratings yet

- Cir vs. Aichi Forging G.R. No. 184823Document14 pagesCir vs. Aichi Forging G.R. No. 184823Eiv AfirudesNo ratings yet

- Size Value and Momentum in International Stock Returns Fama FrenchDocument38 pagesSize Value and Momentum in International Stock Returns Fama Frenchrisk360No ratings yet

- Getaround's Alleged Earliest Investor Files Suit For Alleged Fraud Against The Carsharing Company, CEO Sam Zaid, CFO Adam KosmickiDocument2 pagesGetaround's Alleged Earliest Investor Files Suit For Alleged Fraud Against The Carsharing Company, CEO Sam Zaid, CFO Adam KosmickiPR.comNo ratings yet

- Cost ManagementDocument5 pagesCost Managementels emsNo ratings yet

- Thuc Hanh Excel - Bai Toan QHTTDocument5 pagesThuc Hanh Excel - Bai Toan QHTTHồng Như NguyễnNo ratings yet

- Beta Leverage Divisional BetaDocument2 pagesBeta Leverage Divisional Betazunaira_riaz3271No ratings yet

- ICAN A2 BMF Mock Answers 2019 v2Document10 pagesICAN A2 BMF Mock Answers 2019 v2AKINYEMI ADISA KAMORUNo ratings yet

- Dmpa 1-4Document39 pagesDmpa 1-4sebas matosNo ratings yet

- Account Receivable ClassDocument30 pagesAccount Receivable ClassBeast aNo ratings yet

- 5 TomCollier SPEE Annual Parameters SurveyDocument20 pages5 TomCollier SPEE Annual Parameters SurveymdshoppNo ratings yet

- Internship ReportDocument9 pagesInternship ReportAssel NakypbekovaNo ratings yet

- ACCOUNTING 12-07 - Audit-Assurance-Ethics-and-GovernanceDocument11 pagesACCOUNTING 12-07 - Audit-Assurance-Ethics-and-GovernanceNico evansNo ratings yet

- Ms. Aye Aye Mar: Work Experience ProfileDocument2 pagesMs. Aye Aye Mar: Work Experience ProfileJob GoNo ratings yet

- "Bank Lending, A Significant Effort To Financing Sme'': Eliona Gremi PHD CandidateDocument6 pages"Bank Lending, A Significant Effort To Financing Sme'': Eliona Gremi PHD CandidateAnduela MemaNo ratings yet

- OFFICIAL RATES 2020 PRINCESS GOLDEN BEACH INDpdfDocument3 pagesOFFICIAL RATES 2020 PRINCESS GOLDEN BEACH INDpdfMocanu AdrianNo ratings yet

- Accounting Principles 10e Chapter 2 NotesDocument18 pagesAccounting Principles 10e Chapter 2 NotesallthefreakypeopleNo ratings yet

- Vol.4 Issue.1-03 Full TextDocument14 pagesVol.4 Issue.1-03 Full TextrifkiboyzNo ratings yet

- Beneish M-Score - Finbox TemplateDocument6 pagesBeneish M-Score - Finbox Templatemichael odiemboNo ratings yet