You might also like

- Algerian Islamic Banks: The Role of Relationships Marketing Tactics and Customer LoyaltyFrom EverandAlgerian Islamic Banks: The Role of Relationships Marketing Tactics and Customer LoyaltyNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Customer Satisfaction Towars Islamic BankingDocument9 pagesCustomer Satisfaction Towars Islamic BankingAli Raza SultaniNo ratings yet

- Article1380722222 Rehman PDFDocument7 pagesArticle1380722222 Rehman PDFMuhammad Irfan MalikNo ratings yet

- Jurnal 3 PemasaranDocument16 pagesJurnal 3 PemasaranAdeLia MareLizaNo ratings yet

- Comparative Analysis of Customer Satisfaction On Islamic and Conventional Banks in MalaysiaDocument8 pagesComparative Analysis of Customer Satisfaction On Islamic and Conventional Banks in MalaysiadhdmudNo ratings yet

- Amin & Isa 2008,3Document19 pagesAmin & Isa 2008,3Geet KukadiyaNo ratings yet

- Islamic Bank Service Quality and It's Impact On Indonesian Customers' Satisfaction and LoyaltyDocument22 pagesIslamic Bank Service Quality and It's Impact On Indonesian Customers' Satisfaction and LoyaltyHariNo ratings yet

- Performance Analysis of Islamic Banks ADocument11 pagesPerformance Analysis of Islamic Banks AGREEN FIELD AGRO HI- TECH SERVICES SANGAMNER.No ratings yet

- SavedrecsDocument388 pagesSavedrecsAshraf KhanNo ratings yet

- 249Document5 pages249Mohamed MustefaNo ratings yet

- Customer Loyalty in Sharia Bank Savings ProductsDocument14 pagesCustomer Loyalty in Sharia Bank Savings Productswaseem ahsanNo ratings yet

- Customer Satisfaction and Awareness of Islamic BANKING in PKDocument10 pagesCustomer Satisfaction and Awareness of Islamic BANKING in PKsalma khandNo ratings yet

- Ahmad Et AlDocument9 pagesAhmad Et AlmiaNo ratings yet

- 1 PB PDFDocument19 pages1 PB PDFArafat SarderNo ratings yet

- Islamic Banking Experience of Pakistan: Comparison Between Islamic and Conventional BanksDocument7 pagesIslamic Banking Experience of Pakistan: Comparison Between Islamic and Conventional BanksYasir AbbasNo ratings yet

- Ascarya EditDocument34 pagesAscarya Editjaharuddin.hannoverNo ratings yet

- Islamic Bank Retail Management Factors and Customer Knowledge ModelDocument5 pagesIslamic Bank Retail Management Factors and Customer Knowledge ModelasrielNo ratings yet

- Consumer Perception of Internet Banking Service QualityDocument10 pagesConsumer Perception of Internet Banking Service QualityparikharistNo ratings yet

- 2 Service Quality Dimensions of Islamic BanksDocument11 pages2 Service Quality Dimensions of Islamic Banksauroob_irshadNo ratings yet

- Final Research ProposalDocument19 pagesFinal Research ProposalAli Safina50% (2)

- 394 843 3 PB PDFDocument11 pages394 843 3 PB PDFFaizan ChNo ratings yet

- Effects of Service Quality, Customer Trust and Customer Religious Commitment On Customer Satisfaction and Loyalty of Islamic Banks in East JavaDocument14 pagesEffects of Service Quality, Customer Trust and Customer Religious Commitment On Customer Satisfaction and Loyalty of Islamic Banks in East JavaPradipta Ari SeptianNo ratings yet

- Akt Syariah Ujian Ica Nabila Shahira 200420183Document11 pagesAkt Syariah Ujian Ica Nabila Shahira 200420183Ica Nabila ShahiraNo ratings yet

- Size and Returns To Scale of The Islamic Banking Industry in Malaysia: Foreign Versus Domestic BanksDocument29 pagesSize and Returns To Scale of The Islamic Banking Industry in Malaysia: Foreign Versus Domestic BanksNoraishah IsmailNo ratings yet

- Customer SatisfactionDocument6 pagesCustomer SatisfactionmsaadnaeemNo ratings yet

- Y 110Document19 pagesY 110Zain Ul AbidinNo ratings yet

- Building Corporate Image Through Integrated Marketing Communication and Service Quality On Islamic Bank in IndonesiaDocument19 pagesBuilding Corporate Image Through Integrated Marketing Communication and Service Quality On Islamic Bank in IndonesiaRey ShantNo ratings yet

- Isl BankDocument15 pagesIsl Bankpie sweetyNo ratings yet

- Islamic Banks Performance: An Assessment Using Sharia, Sharia Conformity and Profitability and CAMELSDocument16 pagesIslamic Banks Performance: An Assessment Using Sharia, Sharia Conformity and Profitability and CAMELSAssyifa NurtiasihNo ratings yet

- Banking Service Quality Impact on Customer SatisfactionDocument12 pagesBanking Service Quality Impact on Customer SatisfactionYashPalNo ratings yet

- The Effect of Religiosity, Service Quality, and Trust On Customer Loyalty in Islamic Banking in Bogor IndonesiaDocument10 pagesThe Effect of Religiosity, Service Quality, and Trust On Customer Loyalty in Islamic Banking in Bogor IndonesiaendahNo ratings yet

- Customer Perception of The Effectiveness of Service Quality Delivery of Islamic Banks in Nigeria: An Evaluation of Jaiz BankDocument8 pagesCustomer Perception of The Effectiveness of Service Quality Delivery of Islamic Banks in Nigeria: An Evaluation of Jaiz BankAngelicaNo ratings yet

- An Empirical Investigation of Islamic Banking in PDocument10 pagesAn Empirical Investigation of Islamic Banking in PRacksun NasimNo ratings yet

- New PDFDocument13 pagesNew PDFRoza RahmanNo ratings yet

- Factors Influencing Customers Loyalty Towards Islamic Banking: A Case Study in Gombak, SelangorDocument10 pagesFactors Influencing Customers Loyalty Towards Islamic Banking: A Case Study in Gombak, SelangorMarryam Abdul RazzaqNo ratings yet

- Islamic Financial System and Conventional Banking: A ComparisonDocument13 pagesIslamic Financial System and Conventional Banking: A ComparisonDenis IoniţăNo ratings yet

- Rimel Internship Report On SJIBL (2003)Document54 pagesRimel Internship Report On SJIBL (2003)arcbzamitNo ratings yet

- 1 SMDocument10 pages1 SMSaad AhmadNo ratings yet

- 406983262-People-Perception-Toward-Islamic-BankingDocument15 pages406983262-People-Perception-Toward-Islamic-BankingMohamed MustefaNo ratings yet

- Attitude and Patronage Factors of Bank Customers inDocument14 pagesAttitude and Patronage Factors of Bank Customers inabaidurrehmanNo ratings yet

- 1437 3214 1 SM PDFDocument8 pages1437 3214 1 SM PDFtaimoorNo ratings yet

- Sharia Banking Performance in Makassar Salmah SaidDocument22 pagesSharia Banking Performance in Makassar Salmah SaidGreenteaThirdNo ratings yet

- A1 Fa18 Bba 185 Hamza Kayani BDocument5 pagesA1 Fa18 Bba 185 Hamza Kayani BMuhammad Ameer Hamza KayanNo ratings yet

- The Performance of Malaysian Islamic Bank During 1984-1997: An Exploratory StudyDocument14 pagesThe Performance of Malaysian Islamic Bank During 1984-1997: An Exploratory StudySanorita ShyingNo ratings yet

- 7425 24932 2 PBDocument18 pages7425 24932 2 PBShofa SalsabilaNo ratings yet

- People Perception Toward Islamic BankingDocument15 pagesPeople Perception Toward Islamic BankingHaroonNo ratings yet

- Evaluating The Likelihood of Switching Among Cimb Bank's Existing CustomersDocument64 pagesEvaluating The Likelihood of Switching Among Cimb Bank's Existing Customersnhazwanimhay_2642732No ratings yet

- 0 ICICI Journal2010Document8 pages0 ICICI Journal2010VANSHITA SHUKLANo ratings yet

- 497-Research Results-1872-1-10-20180410Document4 pages497-Research Results-1872-1-10-20180410FredNo ratings yet

- Analysis of Indonesian Islamic and Conventional Banking Before and After 2008Document7 pagesAnalysis of Indonesian Islamic and Conventional Banking Before and After 2008zhafirah nurhasanahNo ratings yet

- 246 655 1 SMDocument20 pages246 655 1 SMsarthakNo ratings yet

- Rujukan Alternatif 1 - Do - Customers' - Perceptions - of - IDocument19 pagesRujukan Alternatif 1 - Do - Customers' - Perceptions - of - IMotivasion GoNo ratings yet

- Islamic-Bank Selection Criteria in Malaysia: An Ahp ApproachDocument11 pagesIslamic-Bank Selection Criteria in Malaysia: An Ahp ApproachAnonymous ZpxXGPNo ratings yet

- Nurhayati & Fatmasaris Sukesti Universitas Muhammadiyah SemarangDocument13 pagesNurhayati & Fatmasaris Sukesti Universitas Muhammadiyah Semarangazzani fifi lutfiawatiNo ratings yet

- SavedrecsDocument422 pagesSavedrecsAshraf KhanNo ratings yet

- 5 PDFDocument13 pages5 PDFVictoria MaciasNo ratings yet

- Factors Influencing Adoption of Islamic Banking: A Study From PakistanDocument16 pagesFactors Influencing Adoption of Islamic Banking: A Study From PakistanamatulmateennoorNo ratings yet

- Analysis of Customer Satisfaction With The Islamic Banking Sector: Case of Brunei DarussalamDocument14 pagesAnalysis of Customer Satisfaction With The Islamic Banking Sector: Case of Brunei DarussalamMegy AwanNo ratings yet

- Banking Governance, Performance and Risk-Taking: Conventional Banks vs Islamic BanksFrom EverandBanking Governance, Performance and Risk-Taking: Conventional Banks vs Islamic BanksNo ratings yet

- TM Set Up & Operate A Camp Site 240715Document134 pagesTM Set Up & Operate A Camp Site 240715Friti FritiNo ratings yet

- Provide Arrival and Departure Assistance D2.TTG - CL3.17 Trainee ManualDocument75 pagesProvide Arrival and Departure Assistance D2.TTG - CL3.17 Trainee ManualFriti FritiNo ratings yet

- Visa 140426060918 Phpapp01Document48 pagesVisa 140426060918 Phpapp01Friti FritiNo ratings yet

- Applying for Management Consultant CertificationDocument4 pagesApplying for Management Consultant CertificationFriti Friti80% (10)

- TM Conduct Pre-Departure Checks 270415Document94 pagesTM Conduct Pre-Departure Checks 270415Friti FritiNo ratings yet

- AET55 - Ethiopia Semien Mt. TrekkingDocument7 pagesAET55 - Ethiopia Semien Mt. TrekkingFriti FritiNo ratings yet

- Event Management Guide (Apr 2011)Document27 pagesEvent Management Guide (Apr 2011)Friti FritiNo ratings yet

- Festival and Event Planning Tool Kit Tcm40 223120Document25 pagesFestival and Event Planning Tool Kit Tcm40 223120Brandy ThomasNo ratings yet

- International Travel Documents-eBook 2015-TravefyDocument21 pagesInternational Travel Documents-eBook 2015-TravefyMaryiNo ratings yet

- Important Notes For Taxi DriversDocument9 pagesImportant Notes For Taxi DriversFriti FritiNo ratings yet

- Employee Transfer and Promotion PolicyDocument31 pagesEmployee Transfer and Promotion PolicyFriti Friti100% (1)

- Historic Route - 10 Days - Zagwe Ethiopia Tours and Travel - Tour in Ethiopia - Ethiopia Tour Travel - Ethiopia Tour & Travel - Tour and Travel Ethiopia - Tour To EthiopiaDocument2 pagesHistoric Route - 10 Days - Zagwe Ethiopia Tours and Travel - Tour in Ethiopia - Ethiopia Tour Travel - Ethiopia Tour & Travel - Tour and Travel Ethiopia - Tour To EthiopiaFriti FritiNo ratings yet

- Concepts of National IncomeDocument3 pagesConcepts of National IncomeFriti FritiNo ratings yet

- Principles of Event ManagementDocument77 pagesPrinciples of Event ManagementCarlos Espinoza89% (9)

- Historical Development of TourismDocument7 pagesHistorical Development of TourismFriti Friti100% (1)

- Elements of Effective Workplace CommunicationDocument4 pagesElements of Effective Workplace CommunicationFriti FritiNo ratings yet

- Catering and Tourism Training Center RegulationDocument6 pagesCatering and Tourism Training Center RegulationFriti FritiNo ratings yet

- Campsite SelectionDocument7 pagesCampsite SelectionFriti FritiNo ratings yet

- Customer CareDocument7 pagesCustomer CareFriti FritiNo ratings yet

- Intro 2 Customer ServiceDocument3 pagesIntro 2 Customer ServiceFriti FritiNo ratings yet

- Plan Skill DevelopmentDocument15 pagesPlan Skill DevelopmentFriti FritiNo ratings yet

- Lo 2 Coaching ColleaguesDocument5 pagesLo 2 Coaching ColleaguesFriti FritiNo ratings yet

- Customer CareDocument7 pagesCustomer CareFriti FritiNo ratings yet

- Wcms 218329Document20 pagesWcms 218329inyasiNo ratings yet

- Two Slave Brothers Birthed Africa's O.....Document7 pagesTwo Slave Brothers Birthed Africa's O.....Friti FritiNo ratings yet

- African Union Conference CenterDocument2 pagesAfrican Union Conference CenterFriti FritiNo ratings yet

- Topic Page:: Ankh, An Ancient Egyptian Symbol Of... in Encyclopedia of African ReligionDocument3 pagesTopic Page:: Ankh, An Ancient Egyptian Symbol Of... in Encyclopedia of African ReligionFriti FritiNo ratings yet

- World Heritages - EthiopiaDocument36 pagesWorld Heritages - EthiopiaFriti FritiNo ratings yet

- Integrating Business Skills Into Ecotourism Operations: Tourism MarketingDocument42 pagesIntegrating Business Skills Into Ecotourism Operations: Tourism MarketingFriti FritiNo ratings yet

- Develop and Update Tourism Industry Knowledge: D2.TCC - CL1.07 Trainer GuideDocument182 pagesDevelop and Update Tourism Industry Knowledge: D2.TCC - CL1.07 Trainer GuideFriti FritiNo ratings yet

- Opentuition Com: Project and Relationship ManagementDocument102 pagesOpentuition Com: Project and Relationship Managementakirevski001No ratings yet

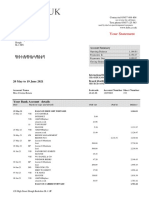

- Your Statement: 20 May To 19 June 2021Document3 pagesYour Statement: 20 May To 19 June 2021Cristina Rotaru100% (1)

- BibliografieDocument2 pagesBibliografieAndrei IonescuNo ratings yet

- Buy Back of SharesDocument71 pagesBuy Back of Sharesmastionline121No ratings yet

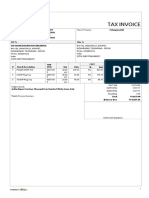

- InvoiceDocument1 pageInvoicemanishbisht014No ratings yet

- NISM SERIES XV - RESEARCH ANALYST CERTIFICATION EXAMDocument40 pagesNISM SERIES XV - RESEARCH ANALYST CERTIFICATION EXAMjack75% (4)

- This Study Resource WasDocument3 pagesThis Study Resource Waschiji chzzzmeowNo ratings yet

- Gina L Tingday, Quiz 6 - MarketingDocument1 pageGina L Tingday, Quiz 6 - MarketingGina TingdayNo ratings yet

- PR ConsultantDocument40 pagesPR ConsultantMelinda ParamithaNo ratings yet

- Aryan Sirohi - STPR - 2100290700038Document115 pagesAryan Sirohi - STPR - 2100290700038Bharti KatyanNo ratings yet

- Managing Human Resources Challenges for Small BusinessesDocument8 pagesManaging Human Resources Challenges for Small Businessesajay goudNo ratings yet

- PEG Bible Sanitized Version v2Document157 pagesPEG Bible Sanitized Version v2Luke Constable100% (2)

- Case Study NetworkingDocument15 pagesCase Study Networkingmaulana anjasmaraNo ratings yet

- Chapter IV Capital Structure and Long Term Financing DecisionDocument117 pagesChapter IV Capital Structure and Long Term Financing DecisionLaren KayeNo ratings yet

- Indirect Taxes: Income TaxDocument9 pagesIndirect Taxes: Income TaxDanial ShadNo ratings yet

- SOCAP15 Program Book FINAL PDFDocument104 pagesSOCAP15 Program Book FINAL PDFadrianne342No ratings yet

- Hard Currency & Soft CurrencyDocument2 pagesHard Currency & Soft CurrencyPratik PatilNo ratings yet

- Adam RevoDocument2 pagesAdam RevoSaima AliNo ratings yet

- Real Estate Gazette Issue 37Document44 pagesReal Estate Gazette Issue 37FaraiKangwendeNo ratings yet

- Theory and PracticeDocument27 pagesTheory and PracticeJulynna Victoria Sodsod Belleza83% (6)

- Investment Law Projec - SANDESHNIRANJANDocument22 pagesInvestment Law Projec - SANDESHNIRANJANSandeshNiranjanNo ratings yet

- MSBPDocument19 pagesMSBPFahim KhanNo ratings yet

- mc30 Mutual Funds PDFDocument3 pagesmc30 Mutual Funds PDFAnkur ShahNo ratings yet

- Nanyang Technological University Nanyang Business School BH3301 - Employment Law Seminar 2 - Contract of EmploymentDocument2 pagesNanyang Technological University Nanyang Business School BH3301 - Employment Law Seminar 2 - Contract of EmploymentAccount SpamNo ratings yet

- 5708 RadhakrishnanDocument2 pages5708 RadhakrishnanAvishek GhosalNo ratings yet

- Inv-0059 Sri Maheshwari EngineeringDocument1 pageInv-0059 Sri Maheshwari EngineeringSRIKAR DHANOORINo ratings yet

- Child Labour and Education UKDocument78 pagesChild Labour and Education UKDina DawoodNo ratings yet

- Decision Trees Background NoteDocument14 pagesDecision Trees Background NoteibrahimNo ratings yet

- MASTER-BUDGETDocument36 pagesMASTER-BUDGETRafols AnnabelleNo ratings yet

- NISM Paper 1 To 5 MOCK Test - Vry ImpDocument26 pagesNISM Paper 1 To 5 MOCK Test - Vry ImpKumarGaurav50% (2)