You might also like

- Sample Answer Foreclosure Defense New JerseyDocument15 pagesSample Answer Foreclosure Defense New Jerseyjack1929100% (23)

- Income TaxationDocument211 pagesIncome Taxationfritz100% (2)

- Income TaxationDocument211 pagesIncome Taxationfritz100% (5)

- Intermediate Accounting 2 Theories Final ExaminationDocument10 pagesIntermediate Accounting 2 Theories Final ExaminationRheu Reyes100% (1)

- BlueVine Small-Business Loans - 2020 Review - 1 NerdWalletDocument5 pagesBlueVine Small-Business Loans - 2020 Review - 1 NerdWalletfosamorNo ratings yet

- Modes of Acquiring Land TitlesDocument3 pagesModes of Acquiring Land TitlesJune Alapa100% (1)

- Guide To The Selling Process of Real Estate Properties in The PhilippinesDocument5 pagesGuide To The Selling Process of Real Estate Properties in The PhilippinesJohnson SambranoNo ratings yet

- Documentary Stamp Tax GuideDocument44 pagesDocumentary Stamp Tax GuideTokis Saba100% (1)

- Comparative Analysis On Non Performing Assets of Private and Public Sector BanksDocument32 pagesComparative Analysis On Non Performing Assets of Private and Public Sector Bankssai thesis33% (3)

- Net Worth Tracking SheetDocument1 pageNet Worth Tracking SheetNestor GonzalezNo ratings yet

- Real Esate Going Global: VietnamDocument11 pagesReal Esate Going Global: VietnamNguyen Quang MinhNo ratings yet

- Quick Sell Repossessed Properties FNB: WWW - Quicksell.co - ZaDocument9 pagesQuick Sell Repossessed Properties FNB: WWW - Quicksell.co - ZaChristian MakandeNo ratings yet

- Indonesia3 GTDT Real Estate 2014Document8 pagesIndonesia3 GTDT Real Estate 2014jokotoniNo ratings yet

- Property Revision Notes - FINALDocument30 pagesProperty Revision Notes - FINALNajmul HasanNo ratings yet

- ReraDocument17 pagesReraChitrartha Gupta50% (2)

- UK Residential Property GuideDocument5 pagesUK Residential Property Guidemiceguelci100% (1)

- Philippines property purchase costs guideDocument2 pagesPhilippines property purchase costs guideAnonymous rVFG5CNo ratings yet

- Land Law 2Document8 pagesLand Law 2Rock LocksleyNo ratings yet

- CommLaw Prelims ReviewerDocument13 pagesCommLaw Prelims Reviewertigerlilyicedtea1No ratings yet

- RERA Act, 2016: It Seeks To Protect Home-Buyers As Well As Help Boost Investments in The Rea L Estate SectorDocument4 pagesRERA Act, 2016: It Seeks To Protect Home-Buyers As Well As Help Boost Investments in The Rea L Estate SectorAnurag ChaudhariNo ratings yet

- Property Registration in GurgaonDocument4 pagesProperty Registration in GurgaonSSKohliNo ratings yet

- Capital Gains Tax GuideDocument24 pagesCapital Gains Tax GuideJezza Mae Gomba RegidorNo ratings yet

- Understanding Real Estate TaxationDocument4 pagesUnderstanding Real Estate TaxationCashmoney AlaskaNo ratings yet

- Chapter 6 Capital Gains TaxationDocument34 pagesChapter 6 Capital Gains TaxationJason Mables100% (1)

- Legal Aspects of SaleDocument7 pagesLegal Aspects of SaleShine Revilla - MontefalconNo ratings yet

- Rescission Refers To The Cancellation of An Agreement or Contract Either Through Mutual Agreement of The Parties or For CauseDocument4 pagesRescission Refers To The Cancellation of An Agreement or Contract Either Through Mutual Agreement of The Parties or For CauseJosephine BercesNo ratings yet

- Chapter 4-Final Income TaxationDocument17 pagesChapter 4-Final Income TaxationPrincesa RoqueNo ratings yet

- LAND LAW CPJMMMMDocument15 pagesLAND LAW CPJMMMMketan cpjNo ratings yet

- CommLaw Compiled ReviewerDocument31 pagesCommLaw Compiled Reviewertigerlilyicedtea1No ratings yet

- General Principles and Income TaxationDocument7 pagesGeneral Principles and Income TaxationLucy HeartfiliaNo ratings yet

- Villanueva V City of IloiloDocument48 pagesVillanueva V City of Iloiloamun dinNo ratings yet

- Module 5 TaxationDocument3 pagesModule 5 Taxationking diyawNo ratings yet

- TAX-Chap 2-3 Question and AnswerDocument9 pagesTAX-Chap 2-3 Question and AnswerPoison Ivy0% (1)

- Unit 4 Land Law CheatingDocument4 pagesUnit 4 Land Law Cheatingketan cpjNo ratings yet

- Module IIDocument47 pagesModule IIxakij19914No ratings yet

- Re RADocument29 pagesRe RAHARSHITA SHUKLA100% (1)

- The Steps To Buying A House in Spain PDFDocument2 pagesThe Steps To Buying A House in Spain PDFLucas FoxNo ratings yet

- Taxes in Real Estate SaleDocument5 pagesTaxes in Real Estate SaleJorgeNo ratings yet

- 51 Fyfield Road, Rainham, Essex RM13 7TX: Strettons - 16 Sep 2020 - Lot Number: 32Document7 pages51 Fyfield Road, Rainham, Essex RM13 7TX: Strettons - 16 Sep 2020 - Lot Number: 32Femi AdeosunNo ratings yet

- Real Estate Sale Taxes ExplainedDocument7 pagesReal Estate Sale Taxes ExplainedJessa CaberteNo ratings yet

- Land Acquisition Act 1894Document11 pagesLand Acquisition Act 1894Vaibhav PanchalNo ratings yet

- Assignment - 2 (Unit Iii & Iv)Document7 pagesAssignment - 2 (Unit Iii & Iv)Ampire AimNo ratings yet

- CIR vs. THE ESTATE OF BENIGNO P. TODA, JR.Document9 pagesCIR vs. THE ESTATE OF BENIGNO P. TODA, JR.Rhett Vincent De La rosaNo ratings yet

- Sem 9 PP Question Bank 17ar18 Anjali KolangaraDocument11 pagesSem 9 PP Question Bank 17ar18 Anjali KolangaraAnjali KolangaraNo ratings yet

- COMM PROP Week 1 Specimen AnswersDocument7 pagesCOMM PROP Week 1 Specimen Answersvyysbfxvg2No ratings yet

- REM ProcessDocument11 pagesREM ProcessAAPHBRSNo ratings yet

- Tax On Corporate Transactions in Portugal Overview - 1 - 1Document27 pagesTax On Corporate Transactions in Portugal Overview - 1 - 1doegoodNo ratings yet

- Module 6 CGT - 1Document3 pagesModule 6 CGT - 1Marklein DumangengNo ratings yet

- Land Acquisition Act: Understanding the ProcedureDocument5 pagesLand Acquisition Act: Understanding the ProcedureNythal GS Kailash100% (1)

- TPOE22-7 Code of Practice For Residential Letting Agents in England - Effective 1 June 2019Document14 pagesTPOE22-7 Code of Practice For Residential Letting Agents in England - Effective 1 June 2019century1000No ratings yet

- Income Taxation T or F ReviewerDocument13 pagesIncome Taxation T or F ReviewerZalaR0cksNo ratings yet

- Real Estate in IndiaDocument9 pagesReal Estate in IndiaVandan SapariaNo ratings yet

- Northern CPAR Chapter on Capital Gains TaxDocument11 pagesNorthern CPAR Chapter on Capital Gains TaxEarth PirapatNo ratings yet

- Chapter 6 Income Tax by BanggawanDocument11 pagesChapter 6 Income Tax by BanggawanEarth PirapatNo ratings yet

- Commercial Lease Fundamentals PhilippinesDocument6 pagesCommercial Lease Fundamentals PhilippinesJonathan Pungtilan MallareNo ratings yet

- Implication of Tax On LeasesDocument5 pagesImplication of Tax On Leaseswankhidr@yahoo.comNo ratings yet

- Week 6Document8 pagesWeek 6Richelle GraceNo ratings yet

- Rblex QuestionDocument17 pagesRblex QuestionIsaac CursoNo ratings yet

- 08 Dealings in Property - BigskyDocument5 pages08 Dealings in Property - BigskyKIM GABRIEL PAMITTANNo ratings yet

- BUSTAXA Business Tax FundamentalsDocument9 pagesBUSTAXA Business Tax FundamentalsTitania ErzaNo ratings yet

- Real Estate Law ProjectDocument8 pagesReal Estate Law Projectsparsh9634No ratings yet

- Docs of Real Estate FinanceDocument3 pagesDocs of Real Estate Financenk9951No ratings yet

- Lesson 12 - Conducting Property SalesDocument64 pagesLesson 12 - Conducting Property SalesmariesharmilaravindranNo ratings yet

- Chapter One: Tax on Commercial & Industrial ProfitsDocument18 pagesChapter One: Tax on Commercial & Industrial ProfitsMāhmõūd ĀhmēdNo ratings yet

- Kail Paul A C An Introduction To ForthDocument123 pagesKail Paul A C An Introduction To Forthyoman777No ratings yet

- Class Rec Theory 0Document179 pagesClass Rec Theory 0yoman777No ratings yet

- PolyaDocument4 pagesPolyaapi-211170679No ratings yet

- The Cosmic EquationDocument7 pagesThe Cosmic Equationyoman777No ratings yet

- GNU Emacs Reference Card: Motion Multiple WindowsDocument2 pagesGNU Emacs Reference Card: Motion Multiple WindowsAlejandro Díaz-CaroNo ratings yet

- What is BNF and how does it define syntaxDocument5 pagesWhat is BNF and how does it define syntaxyoman777No ratings yet

- 1912 11095 PDFDocument11 pages1912 11095 PDFyoman777No ratings yet

- Programmers GuideDocument372 pagesProgrammers GuideELVIS100% (2)

- What is BNF and how does it define syntaxDocument5 pagesWhat is BNF and how does it define syntaxyoman777No ratings yet

- PF Prospectus PDFDocument112 pagesPF Prospectus PDFyoman777No ratings yet

- A Method For Electric Bass Improvisation Via A Detailed AnalysisDocument81 pagesA Method For Electric Bass Improvisation Via A Detailed Analysisrla97623No ratings yet

- A Method For Electric Bass Improvisation Via A Detailed AnalysisDocument81 pagesA Method For Electric Bass Improvisation Via A Detailed Analysisrla97623No ratings yet

- Unified Relationships TheoryDocument14 pagesUnified Relationships Theoryyoman777No ratings yet

- 1912 11095 PDFDocument11 pages1912 11095 PDFyoman777No ratings yet

- 817-08-403E IL Brochure EN 04-07-15 PDFDocument20 pages817-08-403E IL Brochure EN 04-07-15 PDFyoman777No ratings yet

- PF Prospectus PDFDocument112 pagesPF Prospectus PDFyoman777No ratings yet

- 817-08-403E IL Brochure EN 04-07-15 PDFDocument20 pages817-08-403E IL Brochure EN 04-07-15 PDFyoman777No ratings yet

- Ba Yes Intro Class Epi 2018Document43 pagesBa Yes Intro Class Epi 2018yoman777No ratings yet

- Chords Diagrams Closed PDFDocument1 pageChords Diagrams Closed PDFyoman777No ratings yet

- Deep Body Opening One Breath at A Time: Duna Park Beach Club Mon, Wed, Friday 19:15 20:45 10 Euros A ClassDocument1 pageDeep Body Opening One Breath at A Time: Duna Park Beach Club Mon, Wed, Friday 19:15 20:45 10 Euros A Classyoman777No ratings yet

- What is BNF and how does it define syntaxDocument5 pagesWhat is BNF and how does it define syntaxyoman777No ratings yet

- Tiddly LispDocument4 pagesTiddly Lispyoman777No ratings yet

- Ba Yes Intro Class Epi 2018Document43 pagesBa Yes Intro Class Epi 2018yoman777No ratings yet

- GNU Emacs Reference Card: Motion Multiple WindowsDocument2 pagesGNU Emacs Reference Card: Motion Multiple WindowsAlejandro Díaz-CaroNo ratings yet

- CH 1 Contrat PDFDocument33 pagesCH 1 Contrat PDFDarkyyyNo ratings yet

- Ba Yes Intro Class Epi 2018Document43 pagesBa Yes Intro Class Epi 2018yoman777No ratings yet

- Swiftforth Win32Document250 pagesSwiftforth Win32yoman777100% (1)

- Exhibit A SAMPLE CONTRACT PDFDocument11 pagesExhibit A SAMPLE CONTRACT PDFSuppliers ptyNo ratings yet

- Sapiance Closure LetterDocument1 pageSapiance Closure Letteryoman777No ratings yet

- Dpans 94Document224 pagesDpans 94eunomic_readerNo ratings yet

- All SD PacDocument5 pagesAll SD PacPat PowersNo ratings yet

- Frustrated at Age 32: QuestionsDocument1 pageFrustrated at Age 32: QuestionsPradeep Gautam100% (1)

- OBLICON-2nd Exam - 1245 (Dation) and 1252 (Application)Document2 pagesOBLICON-2nd Exam - 1245 (Dation) and 1252 (Application)Karen Joy MasapolNo ratings yet

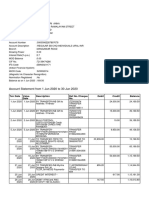

- Account Statement From 1 Jun 2020 To 30 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Jun 2020 To 30 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAnil KumarNo ratings yet

- SBB - Renewal Propsoal - R. S. A. Knit India - Ludhiana - June 2017Document23 pagesSBB - Renewal Propsoal - R. S. A. Knit India - Ludhiana - June 2017tejasj171484No ratings yet

- Guide To: Credit Rating EssentialsDocument19 pagesGuide To: Credit Rating EssentialseduardohfariasNo ratings yet

- Introduction of Banking SystemDocument10 pagesIntroduction of Banking SystemMasy1210% (1)

- Bejoc, RA 2nd Case DigestDocument5 pagesBejoc, RA 2nd Case DigestRonah Abigail BejocNo ratings yet

- Property Cases PDFDocument186 pagesProperty Cases PDFNyl John Caesar GenobiagonNo ratings yet

- 3 - Financial InstitutionsDocument7 pages3 - Financial InstitutionsArmeen KhanNo ratings yet

- Corp Account - Liquidators StatementDocument3 pagesCorp Account - Liquidators StatementAnanth RohithNo ratings yet

- Securitisation - The Indian PerspectiveDocument29 pagesSecuritisation - The Indian PerspectivePriya Ranjan Singh100% (1)

- FN323 - Debt Capital MarketDocument10 pagesFN323 - Debt Capital MarketNapat InseeyongNo ratings yet

- AFAR - Corp LiqDocument1 pageAFAR - Corp LiqJoanna Rose Deciar0% (1)

- Problems in Ppsa and FriaDocument6 pagesProblems in Ppsa and FriaYanaKarununganNo ratings yet

- Due Diligence in Project Finance - Corporate Finance InstituteDocument6 pagesDue Diligence in Project Finance - Corporate Finance Instituteavinash singhNo ratings yet

- IDBI Bank Home LoanDocument11 pagesIDBI Bank Home Loansahil7827No ratings yet

- Informal Financial InstitutionsDocument7 pagesInformal Financial InstitutionsDarwin SolanoyNo ratings yet

- Obli Finals NotesDocument35 pagesObli Finals Notes_cjtenederoNo ratings yet

- Law On P, M, A ActivityDocument2 pagesLaw On P, M, A ActivityLFGS Finals100% (2)

- Contract of LoanDocument2 pagesContract of LoanJanny Carlo SerranoNo ratings yet

- Form - AOC-4 Sign PDFDocument13 pagesForm - AOC-4 Sign PDFamit kumarNo ratings yet

- Discharge of Surety From LiabilityDocument10 pagesDischarge of Surety From LiabilityAAKANKSHA BHATIANo ratings yet

- Sps Vilbar vs. Opinion (Jan 2014) DigestDocument2 pagesSps Vilbar vs. Opinion (Jan 2014) DigestKrissa Jennesca TulloNo ratings yet

- Provisional Remedies (57-61) by Prof. George S.D. AquinoDocument58 pagesProvisional Remedies (57-61) by Prof. George S.D. AquinoPnix HortinelaNo ratings yet