You might also like

- 'It's A Ghost Town' - City of London Market Reacts To Covid Slump - Business - The GuardianDocument4 pages'It's A Ghost Town' - City of London Market Reacts To Covid Slump - Business - The GuardianEly PNo ratings yet

- The Race To Replace The City of London Begins - The Japan TimesDocument3 pagesThe Race To Replace The City of London Begins - The Japan TimesEly PNo ratings yet

- Lloyd's of London - IBS Student BlogDocument7 pagesLloyd's of London - IBS Student BlogEly PNo ratings yet

- Brexit - The Race To Replace The City of London Begins - BloombergDocument4 pagesBrexit - The Race To Replace The City of London Begins - BloombergEly PNo ratings yet

- ST Paul's Cathedral Evacuated As Gas Leak Forces 250 Visitors and Workers Away From Iconic Landmark - London Evening StandardDocument8 pagesST Paul's Cathedral Evacuated As Gas Leak Forces 250 Visitors and Workers Away From Iconic Landmark - London Evening StandardEly PNo ratings yet

- Brexit News - The City of London's Banker Exodus Is Gaining Momentum - BloombergDocument4 pagesBrexit News - The City of London's Banker Exodus Is Gaining Momentum - BloombergEly PNo ratings yet

- Infodriver IDR Token MetricsDocument1 pageInfodriver IDR Token MetricsEly PNo ratings yet

- Emerging Urban Food Governance - The Case of London - LabGovDocument8 pagesEmerging Urban Food Governance - The Case of London - LabGovEly PNo ratings yet

- City of London's Brexit Departures Are Speeding Up - The Washington PostDocument2 pagesCity of London's Brexit Departures Are Speeding Up - The Washington PostEly PNo ratings yet

- Council Post - Three Tips For Running A Successful Family Business PDFDocument4 pagesCouncil Post - Three Tips For Running A Successful Family Business PDFEly PNo ratings yet

- Presidential Debates The Challenge of Creating An Informed Electorate by Kathleen Hall Jamieson, David S. Birdsell PDFDocument273 pagesPresidential Debates The Challenge of Creating An Informed Electorate by Kathleen Hall Jamieson, David S. Birdsell PDFEly PNo ratings yet

- Developing Mental Toughness Gold Medal Strategies For Transforming Your Business PerformanceDocument207 pagesDeveloping Mental Toughness Gold Medal Strategies For Transforming Your Business PerformanceMichael Lazar100% (1)

- Monthly Unicorn Report - Sep 2020Document31 pagesMonthly Unicorn Report - Sep 2020Ely P100% (1)

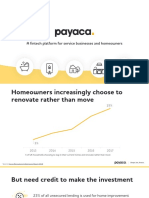

- A Fintech Platform For Service Businesses and HomeownersDocument23 pagesA Fintech Platform For Service Businesses and HomeownersEly PNo ratings yet

- Douglas Walton - Argumentation Methods For Artificial Intelligence and Law-Springer (2005)Document283 pagesDouglas Walton - Argumentation Methods For Artificial Intelligence and Law-Springer (2005)Ely P100% (1)

- Kevin D. Ashley - Artificial Intelligence and Legal AnalyticsDocument451 pagesKevin D. Ashley - Artificial Intelligence and Legal AnalyticsMarco Zubieta100% (4)

- Philosophy in The Flesh PDFDocument590 pagesPhilosophy in The Flesh PDFVolha Hapeyeva92% (26)

- Opinion - Is Huawei Really More Dangerous Than Facebook - Caixin GlobalDocument5 pagesOpinion - Is Huawei Really More Dangerous Than Facebook - Caixin GlobalEly PNo ratings yet

- Ukraine Q1 2018Document1 pageUkraine Q1 2018Ely PNo ratings yet

- Lecture Notes in Computer Science 1806: Edited by G. Goos, J. Hartmanis and J. Van LeeuwenDocument398 pagesLecture Notes in Computer Science 1806: Edited by G. Goos, J. Hartmanis and J. Van LeeuwenEly PNo ratings yet

- Lecture Notes in Computer Science 1806: Edited by G. Goos, J. Hartmanis and J. Van LeeuwenDocument398 pagesLecture Notes in Computer Science 1806: Edited by G. Goos, J. Hartmanis and J. Van LeeuwenEly PNo ratings yet

- 2019-06-17 Bloomberg BusinessweekDocument76 pages2019-06-17 Bloomberg BusinessweekEly PNo ratings yet

- Us TMT 2019 Technology Industry OutlookDocument8 pagesUs TMT 2019 Technology Industry OutlookPingNo ratings yet

- Quick ReferenceDocument19 pagesQuick ReferenceEly PNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Math 7 LAS W1&W2Document9 pagesMath 7 LAS W1&W2Friendsly TamsonNo ratings yet

- BIGDATA LAB MANUALDocument27 pagesBIGDATA LAB MANUALjohn wickNo ratings yet

- The Baldur's Gate Series 1 - Baldur GateDocument125 pagesThe Baldur's Gate Series 1 - Baldur GateJustin MooreNo ratings yet

- Type Italian Characters - Online Italian KeyboardDocument3 pagesType Italian Characters - Online Italian KeyboardGabriel PereiraNo ratings yet

- Directorate of Pension, Provident Fund & Group Insurance: WWW - Wbepension.gov - inDocument37 pagesDirectorate of Pension, Provident Fund & Group Insurance: WWW - Wbepension.gov - inSandipan RoyNo ratings yet

- Mad-Lib ExerciseDocument2 pagesMad-Lib Exercisejbk23100% (2)

- Dallas Symphony Orchestra 2009 Annual ReportDocument14 pagesDallas Symphony Orchestra 2009 Annual ReportCharlie StephensonNo ratings yet

- Dual Shield 7100 Ultra: Typical Tensile PropertiesDocument3 pagesDual Shield 7100 Ultra: Typical Tensile PropertiesDino Paul Castro HidalgoNo ratings yet

- Literature Review Topics RadiographyDocument8 pagesLiterature Review Topics Radiographyea7w32b0100% (1)

- 66 Essential Phrasal Verbs EnglishDocument6 pages66 Essential Phrasal Verbs EnglishNarcisVega100% (15)

- Service Manual: MS-A18WV - MS-A24WV - MS-A30WVDocument32 pagesService Manual: MS-A18WV - MS-A24WV - MS-A30WVCesc BonetNo ratings yet

- JSA of Materila Handling ApproviedDocument2 pagesJSA of Materila Handling Approviedsakthi venkatNo ratings yet

- Turkey GO (896-22)Document1 pageTurkey GO (896-22)shrabon001No ratings yet

- Last Voyage of Somebody The Sailor The SailorDocument581 pagesLast Voyage of Somebody The Sailor The SailorDelia Ungureanu50% (2)

- Passive Voice PDFDocument5 pagesPassive Voice PDFJohan FloresNo ratings yet

- Group 10 - Stem 11 ST - DominicDocument34 pagesGroup 10 - Stem 11 ST - Dominicchristine ancheta100% (1)

- CHAPTER 5 Work MeasurementDocument24 pagesCHAPTER 5 Work MeasurementAiman SupniNo ratings yet

- Europe MapDocument13 pagesEurope MapNguyên ĐỗNo ratings yet

- PIRCHLDocument227 pagesPIRCHLapi-3703916No ratings yet

- TDBFP - Gear Pump API 676 PDFDocument42 pagesTDBFP - Gear Pump API 676 PDFRamon A. Ruiz O.No ratings yet

- Customised Effective Resumes: Content & ChronologyDocument10 pagesCustomised Effective Resumes: Content & ChronologyRishi JhaNo ratings yet

- Server Preparation Details LinuxDocument9 pagesServer Preparation Details Linuxbharatreddy9No ratings yet

- Agrasar Lecture and Demonstration Programme On Water, Food and Climate ChangeDocument20 pagesAgrasar Lecture and Demonstration Programme On Water, Food and Climate ChangeMinatiBindhaniNo ratings yet

- DLP1Document6 pagesDLP1Ben Joseph CapistranoNo ratings yet

- Catalogue For TubingDocument1 pageCatalogue For Tubingprabhakaran.cNo ratings yet

- Government and BusinessDocument2 pagesGovernment and BusinessJoshua BrownNo ratings yet

- Levers of Control Analysis of Management Control SDocument17 pagesLevers of Control Analysis of Management Control SApriana RahmawatiNo ratings yet

- Phy Interface Pci Express Sata Usb31 Architectures Ver43 PDFDocument99 pagesPhy Interface Pci Express Sata Usb31 Architectures Ver43 PDFRaj Shekhar ReddyNo ratings yet

- Survey Questionnaire 3 - Student EngagementDocument2 pagesSurvey Questionnaire 3 - Student EngagementDAN MARK CAMINGAWANNo ratings yet

- CV KM Roy Supit 01 April 2019Document3 pagesCV KM Roy Supit 01 April 2019Ephanama TehnikNo ratings yet