You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The External Rate of Return MethodDocument5 pagesThe External Rate of Return MethodEllen Kay Cacatian80% (5)

- Cost and Revenue of Production: Dr. S P SinghDocument36 pagesCost and Revenue of Production: Dr. S P SinghDuma DumaiNo ratings yet

- MWJ March 2017Document12 pagesMWJ March 2017Duma DumaiNo ratings yet

- Accepted TestsDocument1 pageAccepted TestsDuma DumaiNo ratings yet

- Exim Bank AODocument4 pagesExim Bank AODuma DumaiNo ratings yet

- Current Affairs January 2018 PDFDocument51 pagesCurrent Affairs January 2018 PDFDuma DumaiNo ratings yet

- Accepted TestsDocument1 pageAccepted TestsDuma DumaiNo ratings yet

- Syllabus PGQP42Document1 pageSyllabus PGQP42Duma DumaiNo ratings yet

- Madras School of Economics: & Central University of Tamil NaduDocument8 pagesMadras School of Economics: & Central University of Tamil NaduDuma DumaiNo ratings yet

- MWJ March 2017Document12 pagesMWJ March 2017Duma DumaiNo ratings yet

- Schedule 17 Significant Accounting Policies 1. General Basis of PreparationDocument6 pagesSchedule 17 Significant Accounting Policies 1. General Basis of PreparationDuma DumaiNo ratings yet

- Import Export Code (IEC) India: What You Should KnowDocument7 pagesImport Export Code (IEC) India: What You Should KnowDuma DumaiNo ratings yet

- BELG 28 TechRiskMgmtPolicyForwardContractsDocument36 pagesBELG 28 TechRiskMgmtPolicyForwardContractsDuma DumaiNo ratings yet

- Palak's Doodle-Odes: Tiss NetDocument17 pagesPalak's Doodle-Odes: Tiss NetDuma DumaiNo ratings yet

- "Role of DGFT in Foreign Trade Policy": Group 2Document29 pages"Role of DGFT in Foreign Trade Policy": Group 2Duma DumaiNo ratings yet

- Role of DGFT in Foreign Trade Policy: BY Gaurav Chandra Dev Sahoo Bhoomi Solanki Yashopriya Bhartiya Omkar BhosleDocument13 pagesRole of DGFT in Foreign Trade Policy: BY Gaurav Chandra Dev Sahoo Bhoomi Solanki Yashopriya Bhartiya Omkar BhosleDuma DumaiNo ratings yet

- Thesis JJ HamalainenDocument64 pagesThesis JJ HamalainenDuma DumaiNo ratings yet

- Option Symposium AgendaDocument16 pagesOption Symposium AgendaraveeNo ratings yet

- MS-97 International Business: Emerging IssuesDocument68 pagesMS-97 International Business: Emerging IssuesDhruv DattaNo ratings yet

- Competition Law Notes: UNIT I: IntroductionDocument34 pagesCompetition Law Notes: UNIT I: Introduction2050101 A YUVRAJNo ratings yet

- Performance Measurement in Decentralized OrganizationsDocument9 pagesPerformance Measurement in Decentralized OrganizationsLAZINA AZRINNo ratings yet

- Distributions To Shareholders Dividends and RepurchasesDocument34 pagesDistributions To Shareholders Dividends and RepurchasesSiwar Hakim0% (1)

- Process Flow AnalysisDocument17 pagesProcess Flow AnalysisSiti Hawa SamaluddinNo ratings yet

- Project - CVP AnalysisDocument58 pagesProject - CVP AnalysisRajeevanand Kulkarni100% (1)

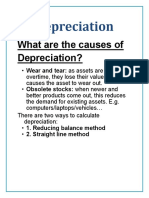

- What Are The Causes of Depreciation?Document10 pagesWhat Are The Causes of Depreciation?Everyday LearnNo ratings yet

- This Study Resource WasDocument1 pageThis Study Resource WasEskwelaSeryeNo ratings yet

- Alina THE BUY NOTHING MOVEMENTDocument5 pagesAlina THE BUY NOTHING MOVEMENTRenataSkuNo ratings yet

- Company LawDocument6 pagesCompany LawTremaine AllenNo ratings yet

- In The USA, Personal Income Tax IllegalDocument10 pagesIn The USA, Personal Income Tax IllegalArnulfo Yu LanibaNo ratings yet

- Buffe BussDocument49 pagesBuffe BussAbhi TiwariNo ratings yet

- Cost of Capital 2Document29 pagesCost of Capital 2BSA 1A100% (2)

- Account Type % Allocation: Retirement/ Total DisabilityDocument1 pageAccount Type % Allocation: Retirement/ Total DisabilityBer Salazar JrNo ratings yet

- Institute of Hospitality Ebooks 2013Document21 pagesInstitute of Hospitality Ebooks 2013PusintuNo ratings yet

- E-Bulletin Foundation Sept 2019Document45 pagesE-Bulletin Foundation Sept 2019Vijay SharmaNo ratings yet

- Adidas OriginalsDocument13 pagesAdidas Originalssarthak bhawnaniNo ratings yet

- 0561-Marketing Theory & PracticeDocument11 pages0561-Marketing Theory & PracticeMuhammad NazirNo ratings yet

- Fiat MoneyDocument10 pagesFiat MoneyGaurav MeenaNo ratings yet

- Passbookstmt 1671020682146Document4 pagesPassbookstmt 1671020682146pravin awalkondeNo ratings yet

- Honey Center Beekeeping Farm Project Proposal For Donor FundingDocument9 pagesHoney Center Beekeeping Farm Project Proposal For Donor FundingRaymondNo ratings yet

- Ministry of Finance - Sri Lanka - Annual Report - 2017Document412 pagesMinistry of Finance - Sri Lanka - Annual Report - 2017lkwriterNo ratings yet

- Organisation Structure and Design Wildfire Entertainent: Presented By-Group 3 (Sec-D)Document6 pagesOrganisation Structure and Design Wildfire Entertainent: Presented By-Group 3 (Sec-D)Sidhant NayakNo ratings yet

- The Concept of Gross Income - Cir vs. Filinvest Development CorporationDocument4 pagesThe Concept of Gross Income - Cir vs. Filinvest Development CorporationKath LeenNo ratings yet

- Taxation Philippines Leasehold Improvements PDF FreeDocument17 pagesTaxation Philippines Leasehold Improvements PDF FreejjNo ratings yet

- Product Life CycleDocument15 pagesProduct Life CycleSonali ChoudharyNo ratings yet

- Investinournewyork BillionairepandemicprofitDocument9 pagesInvestinournewyork BillionairepandemicprofitZacharyEJWilliamsNo ratings yet

- Railways PresentationDocument33 pagesRailways PresentationshambhoiNo ratings yet