You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5811)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

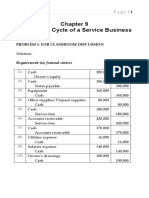

- Sol. Man. - Chapter 9 - Acctg Cycle of A Service BusinessDocument52 pagesSol. Man. - Chapter 9 - Acctg Cycle of A Service Businesscan't yujout80% (5)

- Establishment of Dhaba Project ReportDocument2 pagesEstablishment of Dhaba Project Reportjyotikokate83% (6)

- Assessment Pack-BSBMKG501-OD (26) - 3.en - Id.id - enDocument16 pagesAssessment Pack-BSBMKG501-OD (26) - 3.en - Id.id - enihda0farhatun0nisakNo ratings yet

- PESTLE Analysis CIPDDocument1 pagePESTLE Analysis CIPDAhmed RaajNo ratings yet

- LIC (Life Insurance Corporation)Document14 pagesLIC (Life Insurance Corporation)Abhishek KumarNo ratings yet

- Financial Analysis of Morrisons-UK Retailer (Accounting)Document16 pagesFinancial Analysis of Morrisons-UK Retailer (Accounting)kirtikakkar23No ratings yet

- Latest Intern ReportDocument26 pagesLatest Intern ReportParveshNo ratings yet

- Economic Analysis of Banking Regulation: © 2005 Pearson Education Canada IncDocument15 pagesEconomic Analysis of Banking Regulation: © 2005 Pearson Education Canada IncMuntazir HussainNo ratings yet

- Paper: 08, International Business Operations: ManagementDocument14 pagesPaper: 08, International Business Operations: ManagementMonika SainiNo ratings yet

- Introduction To Media and Advertising in PakistanDocument2 pagesIntroduction To Media and Advertising in PakistanShahzaib SadiqNo ratings yet

- Bahir Dar Universty: Ethiopian Institute of Textile and Fashion Technology (Eitex)Document88 pagesBahir Dar Universty: Ethiopian Institute of Textile and Fashion Technology (Eitex)Mênfës Mgb GèdēchãNo ratings yet

- Management AccountingDocument108 pagesManagement AccountingBATUL ABBAS DEVASWALANo ratings yet

- Chapter 3Document11 pagesChapter 3Taskia SarkarNo ratings yet

- Melroy Miranda Ximr Mms 2 Roll No. 527: Impact On Organisation PerformanceDocument8 pagesMelroy Miranda Ximr Mms 2 Roll No. 527: Impact On Organisation PerformanceMelroy MirandaNo ratings yet

- CO CK80 99 JPN Generate Cost Components ReportDocument18 pagesCO CK80 99 JPN Generate Cost Components ReportnguyencaohuyNo ratings yet

- National Association For Business Resources Names 2023 List of Best and Brightest Companies To Work For in The NationDocument3 pagesNational Association For Business Resources Names 2023 List of Best and Brightest Companies To Work For in The NationD'Errah ScottNo ratings yet

- Chapter 8: Distribution Strategies: AnswerDocument9 pagesChapter 8: Distribution Strategies: AnswerLinh LêNo ratings yet

- Chapter FourDocument14 pagesChapter FourMuzamel AbdellaNo ratings yet

- DCOR 1 0 Design Chain Operations Reference Model DCOR 1 0 1Document245 pagesDCOR 1 0 Design Chain Operations Reference Model DCOR 1 0 1VladTraculNo ratings yet

- Incomplete RecordsDocument2 pagesIncomplete RecordsOkasha AliNo ratings yet

- BA (JMC) 305: Organisation ChartDocument25 pagesBA (JMC) 305: Organisation ChartuiioslNo ratings yet

- This Study Resource WasDocument4 pagesThis Study Resource WasKim TanNo ratings yet

- Insurance Company Cuts Cycle Time by 20% and Saves Nearly $5 Million Using Agile Project Management PracticesDocument1 pageInsurance Company Cuts Cycle Time by 20% and Saves Nearly $5 Million Using Agile Project Management PracticesShahbaz HussainNo ratings yet

- Oil India Limited: Rajasthan Project JodhpurDocument146 pagesOil India Limited: Rajasthan Project Jodhpurhoangminh nguyenhuynhNo ratings yet

- Topic 6 Poma - PPT - Slides-Ch. 8 - 164290Document33 pagesTopic 6 Poma - PPT - Slides-Ch. 8 - 164290YAANESHWARAN A/L CHANDRAN STUDENTNo ratings yet

- MGMT in OrganisationDocument11 pagesMGMT in OrganisationNidhi AtreNo ratings yet

- Proposal On IFB Product Maintenance Within Existing CBSDocument2 pagesProposal On IFB Product Maintenance Within Existing CBSSolomon TekalignNo ratings yet

- Post Quiz 4 - AF101Document11 pagesPost Quiz 4 - AF101Moira Emma N. EdmondNo ratings yet

- Suncorp FAQ FinalDocument2 pagesSuncorp FAQ FinalSam AbdulrahimNo ratings yet

- Quality in Supply Chain: Case Study of Indian Cement IndustryDocument6 pagesQuality in Supply Chain: Case Study of Indian Cement IndustryJoemon John KurishumootillNo ratings yet