You might also like

- Accounting Errors 8-9 (Answers)Document2 pagesAccounting Errors 8-9 (Answers)angela pajelNo ratings yet

- Discontinued Operations Acctg. Test BankDocument12 pagesDiscontinued Operations Acctg. Test BankDalrymple CasballedoNo ratings yet

- Crane Hoist Sling Safety ProgramDocument14 pagesCrane Hoist Sling Safety Programomar sadiqNo ratings yet

- Three Finger TechniqueDocument8 pagesThree Finger Techniquekukoo100% (1)

- Toaz - Info Second Examination With Suggested Answers 1 PRDocument6 pagesToaz - Info Second Examination With Suggested Answers 1 PRJomarNo ratings yet

- Doh A.O. 2011-0005Document24 pagesDoh A.O. 2011-0005HumanRights_Ph100% (2)

- Basic Uc1 Participate in Workplace CommuDocument90 pagesBasic Uc1 Participate in Workplace CommuLourdes ArguellesNo ratings yet

- Basic Eps Praac Valix 2018pdf DDDocument20 pagesBasic Eps Praac Valix 2018pdf DDCaptain ObviousNo ratings yet

- MODULE FinalTerm FAR 3 Cash and Accrual and Single EntryDocument23 pagesMODULE FinalTerm FAR 3 Cash and Accrual and Single EntryKezNo ratings yet

- Accruals & PrepaymentsDocument16 pagesAccruals & Prepaymentswajeeha.arfat008No ratings yet

- Mobile Platform Safety RequirementDocument56 pagesMobile Platform Safety Requirementtnsv222No ratings yet

- BP1800 D Extended Rock Spare Parts Manual Edition - Aug '08Document162 pagesBP1800 D Extended Rock Spare Parts Manual Edition - Aug '08komalinternational5No ratings yet

- Cupola FurnaceDocument27 pagesCupola FurnaceVijay Ganapathy50% (2)

- Chapter 14: Cash and Accrual BasisDocument60 pagesChapter 14: Cash and Accrual BasissofiaNo ratings yet

- ACCGT7 CHP13 PPTDocument7 pagesACCGT7 CHP13 PPTJohn Lester C AlagNo ratings yet

- Valix Book Chapt 1 5 Probs PDFDocument34 pagesValix Book Chapt 1 5 Probs PDFRengeline LucasNo ratings yet

- Errors and Irregularities in The Transaction CycleDocument22 pagesErrors and Irregularities in The Transaction CycleVatchdemonNo ratings yet

- PRE BATTERY EXAM 2018 Part 1 FARDocument11 pagesPRE BATTERY EXAM 2018 Part 1 FARFrl RizalNo ratings yet

- 13 Alvarez II vs. Sun Life of CanadaDocument1 page13 Alvarez II vs. Sun Life of CanadaPaolo AlarillaNo ratings yet

- Cash and Acrrual Basis QUIZDocument2 pagesCash and Acrrual Basis QUIZMarii M.100% (1)

- Gold Company Provided The Following Trial Balance On June 30 PDFDocument3 pagesGold Company Provided The Following Trial Balance On June 30 PDFRengeline LucasNo ratings yet

- Manitou PDF DVD 3 15 8 GB Service and Parts ManualDocument27 pagesManitou PDF DVD 3 15 8 GB Service and Parts Manualgeraldshaffer020389gdb100% (1)

- Accounting For Liabilities Part 1Document5 pagesAccounting For Liabilities Part 1방탄트와이스 짱No ratings yet

- Problem 2: Gondola Company Showed The Following Charges and Credits To Retained Earnings For 2021Document2 pagesProblem 2: Gondola Company Showed The Following Charges and Credits To Retained Earnings For 2021Katrina Dela CruzNo ratings yet

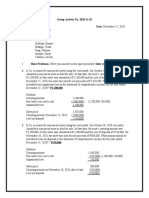

- Group Activity No. 2-Noncurrent Asset Held For Sale-2Document3 pagesGroup Activity No. 2-Noncurrent Asset Held For Sale-2Jericho VillalonNo ratings yet

- Petite Company Reported The Following Current Assets On December 31Document1 pagePetite Company Reported The Following Current Assets On December 31Katrina Dela CruzNo ratings yet

- IA3 Chapter 22 29Document5 pagesIA3 Chapter 22 29ZicoNo ratings yet

- QuestionsDocument16 pagesQuestionsRuby JaneNo ratings yet

- Week 6 Basic Earnings Per ShareDocument4 pagesWeek 6 Basic Earnings Per SharePearlle Ivana TavarroNo ratings yet

- AE18.1 Financial Markets and Financial SystemDocument23 pagesAE18.1 Financial Markets and Financial SystemTrishia Mae OliverosNo ratings yet

- 07 Interim Reporting FinalDocument3 pages07 Interim Reporting FinalMakoy BixenmanNo ratings yet

- Smes - Assets Inventories Basic Financial Instruments Investment in Associate Investment PropertyDocument21 pagesSmes - Assets Inventories Basic Financial Instruments Investment in Associate Investment PropertyToni Rose Hernandez LualhatiNo ratings yet

- ? IA3 SIM Answers Week 12-13 ULO123 Hyperinflation & Current Cost AccountingDocument6 pages? IA3 SIM Answers Week 12-13 ULO123 Hyperinflation & Current Cost AccountingJeric TorionNo ratings yet

- This Study Resource Was: Exercise 3-2Document2 pagesThis Study Resource Was: Exercise 3-2Tanyelle LouvNo ratings yet

- Operating Segment.Document14 pagesOperating Segment.Honey LimNo ratings yet

- Cash Basis Accrual BasisDocument4 pagesCash Basis Accrual BasisForkenstein0% (1)

- Tax 321 Chap 13Document7 pagesTax 321 Chap 13Team MindanaoNo ratings yet

- AE 17 M8 ExercisesDocument46 pagesAE 17 M8 ExercisesKim FloresNo ratings yet

- Pre Week MaterialsDocument44 pagesPre Week MaterialsMarjorie PalmaNo ratings yet

- I Am Sharing 'SIM-ANSWERS - 6th-Exam-Topics - Hyperinflation - PABRES' With YouDocument9 pagesI Am Sharing 'SIM-ANSWERS - 6th-Exam-Topics - Hyperinflation - PABRES' With YouJeric TorionNo ratings yet

- SMALL AND MEDIUM EntitiesDocument19 pagesSMALL AND MEDIUM Entitiesmarx marolinaNo ratings yet

- Chapter 20 - Current Cost Acctg. Valix ReviewerDocument11 pagesChapter 20 - Current Cost Acctg. Valix ReviewerDesiree Sogo-an PolicarpioNo ratings yet

- Chapter 10 - Cash To Accrual Basis of AccountingDocument3 pagesChapter 10 - Cash To Accrual Basis of AccountingXienaNo ratings yet

- Chapter 1Document13 pagesChapter 1Ella Marie WicoNo ratings yet

- Chapter 14Document164 pagesChapter 14Alvina Baquiran100% (1)

- Single Entry MethodDocument6 pagesSingle Entry MethodNhel AlvaroNo ratings yet

- Reading 36: Cost of CapitalDocument41 pagesReading 36: Cost of CapitalEmiraslan MhrrovNo ratings yet

- Cdsga MISSIONDocument2 pagesCdsga MISSIONRm Gorero0% (1)

- Notes Quiz PDFDocument2 pagesNotes Quiz PDFkim cheNo ratings yet

- Statement of Comprehensive Income Part 2 StudentDocument7 pagesStatement of Comprehensive Income Part 2 StudentAG VenturesNo ratings yet

- Auditing Problem 2Document1 pageAuditing Problem 2jhobs100% (1)

- In Docs Files PDFDocument51 pagesIn Docs Files PDFLemhar DayaoenNo ratings yet

- Operating Segment StudentsDocument4 pagesOperating Segment StudentsAG VenturesNo ratings yet

- Financial Accounting Vol.3 ADocument10 pagesFinancial Accounting Vol.3 ALovely Lorelie Del Mundo Planos29% (14)

- This Study Resource Was: Notes To Financial Statement Problem 3-1Document6 pagesThis Study Resource Was: Notes To Financial Statement Problem 3-1Kim FloresNo ratings yet

- Chap 36 - Land and Building Fin Acct 1 - Barter Summary Team PDFDocument4 pagesChap 36 - Land and Building Fin Acct 1 - Barter Summary Team PDFJunneth Pearl HomocNo ratings yet

- Title of Module: Intermediate Accounting 3 Topic: I. Book Value Per Share Learning ObjectivesDocument19 pagesTitle of Module: Intermediate Accounting 3 Topic: I. Book Value Per Share Learning ObjectivesDenmark CabadduNo ratings yet

- HFDSDHDocument8 pagesHFDSDHMary Grace Castillo AlmonedaNo ratings yet

- IA3 Chapter 15 AnswersDocument1 pageIA3 Chapter 15 AnswersBea TumulakNo ratings yet

- Intermediate Accounting Chapters 13,14Document50 pagesIntermediate Accounting Chapters 13,14Jonathan NavalloNo ratings yet

- Activity: Basic Earnings Per ShareDocument2 pagesActivity: Basic Earnings Per Sharebi23450% (1)

- Chapter 4: Fraud: Jovit G. Cain, CPADocument23 pagesChapter 4: Fraud: Jovit G. Cain, CPAJao FloresNo ratings yet

- NU - Correction of Errors Single Entry Cash To AccrualDocument8 pagesNU - Correction of Errors Single Entry Cash To AccrualJem ValmonteNo ratings yet

- Chapter 14 Answer PDF FreeDocument24 pagesChapter 14 Answer PDF FreeAang GrandeNo ratings yet

- Key Quiz 3 1st 2022 20223Document4 pagesKey Quiz 3 1st 2022 20223Leslie Mae Vargas ZafeNo ratings yet

- Dia Mae A. Generoso - Learning Activity 3Document10 pagesDia Mae A. Generoso - Learning Activity 3Dia Mae Ablao GenerosoNo ratings yet

- Assignment 7 - RosalDocument4 pagesAssignment 7 - RosalGinie Lyn RosalNo ratings yet

- Interim Financial Reporting: Problem 45-1: True or FalseDocument9 pagesInterim Financial Reporting: Problem 45-1: True or FalseAudrey AganNo ratings yet

- Interim Financial Reporting: Problem 45-1: True or FalseDocument9 pagesInterim Financial Reporting: Problem 45-1: True or FalseAudrey AganNo ratings yet

- VALVEDocument2 pagesVALVEmadesh mNo ratings yet

- Schema de Instalare Sitem Presurizare 1Document1 pageSchema de Instalare Sitem Presurizare 1Cujba CodrinNo ratings yet

- Barangay Disaster Risk Reduction and Management Investment Plan C.Y. 2018-2022Document1 pageBarangay Disaster Risk Reduction and Management Investment Plan C.Y. 2018-2022Cristina MelloriaNo ratings yet

- Bliss: Blind Source Separation and ApplicationsDocument4 pagesBliss: Blind Source Separation and ApplicationspostscriptNo ratings yet

- Sample MCQ - Facility Location and LayoutDocument3 pagesSample MCQ - Facility Location and LayoutJITENDRA SINGHNo ratings yet

- Visa Direct General Funds Disbursement Sellsheet PDFDocument2 pagesVisa Direct General Funds Disbursement Sellsheet PDFPablo González de PazNo ratings yet

- Human Resource Management in Case of Hawassa Industry ParkDocument11 pagesHuman Resource Management in Case of Hawassa Industry ParkFiker Er MarkNo ratings yet

- Bangladesh Institute of Management BimDocument52 pagesBangladesh Institute of Management Bimmohsin hannan72No ratings yet

- Legal Writing Reviewer Atty Arnold Cacho PDFDocument11 pagesLegal Writing Reviewer Atty Arnold Cacho PDFPaul ValerosNo ratings yet

- Sociol 2z03, Spring 2022, Z. LuoDocument6 pagesSociol 2z03, Spring 2022, Z. LuoGarcía MarlinhoNo ratings yet

- Method Statement: Telecommunication & Security System (TCSS)Document2 pagesMethod Statement: Telecommunication & Security System (TCSS)mochacino68No ratings yet

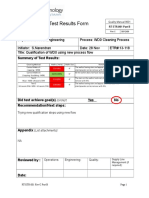

- Engineering Test Results FormDocument1 pageEngineering Test Results FormVijay RajaindranNo ratings yet

- COST: It May Be Defined As The Monetary Value of All Sacrifices Made To Achieve An Objective (I.e. To Produce Goods and Services)Document18 pagesCOST: It May Be Defined As The Monetary Value of All Sacrifices Made To Achieve An Objective (I.e. To Produce Goods and Services)अक्षय शर्माNo ratings yet

- Report of Pepsi CompanyDocument35 pagesReport of Pepsi CompanyEmiNo ratings yet

- General Specifications Ventilation and Monitoring ParametersDocument2 pagesGeneral Specifications Ventilation and Monitoring ParametersThiết bị Điện Tử Y Sinh0% (1)

- Converting V7 Filesto V8 MR3 in Micro StationDocument8 pagesConverting V7 Filesto V8 MR3 in Micro StationerikestrelaNo ratings yet

- Lemonade Stall Version 1 - 4Document19 pagesLemonade Stall Version 1 - 4Alan LibertNo ratings yet

- VIVAPUR Alginate CH: White CheeseDocument4 pagesVIVAPUR Alginate CH: White CheeseKhaoula GougniNo ratings yet

- Measuring National IncomeDocument26 pagesMeasuring National IncomeSaidur Rahman Sid100% (1)

- Assessment Ans 4eDocument12 pagesAssessment Ans 4eLeeBruceNo ratings yet

- Wa0015.Document9 pagesWa0015.Santosh Kumar GuptaNo ratings yet