0% found this document useful (0 votes)

3K views7 pagesSME's

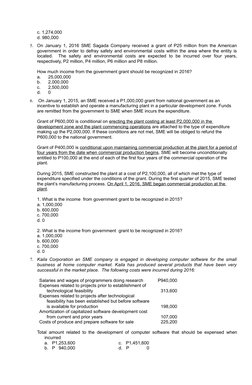

This document contains 11 multiple choice questions related to accounting concepts for small and medium enterprises (SMEs). The questions cover topics such as capitalizing interest, asset revaluation, gains/losses on disposal of assets, government grants, impairment of intangible assets, accounting for investments, and accounting for share-based payments.

Uploaded by

JiezelEstebeCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

3K views7 pagesSME's

This document contains 11 multiple choice questions related to accounting concepts for small and medium enterprises (SMEs). The questions cover topics such as capitalizing interest, asset revaluation, gains/losses on disposal of assets, government grants, impairment of intangible assets, accounting for investments, and accounting for share-based payments.

Uploaded by

JiezelEstebeCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd