You might also like

- Chapter 4 Exempt SalesDocument23 pagesChapter 4 Exempt SalesHazel Jane Esclamada0% (2)

- Accounting 9th Canadian Edition Volume 1 Test BankDocument66 pagesAccounting 9th Canadian Edition Volume 1 Test BankgloriyaNo ratings yet

- Estate Tax PayableDocument8 pagesEstate Tax PayableHazel Jane Esclamada100% (2)

- Chapter 17 Donor's TaxDocument7 pagesChapter 17 Donor's TaxHazel Jane Esclamada100% (3)

- Course Financial Management Developer and Their Background: See Assignment / Agreement SectionDocument33 pagesCourse Financial Management Developer and Their Background: See Assignment / Agreement SectionHazel Jane Esclamada100% (1)

- Chapter 9 Input VatDocument10 pagesChapter 9 Input VatHazel Jane EsclamadaNo ratings yet

- Chapter 10 Vat Still DueDocument7 pagesChapter 10 Vat Still DueHazel Jane EsclamadaNo ratings yet

- Chapter 3 Introduction To Business TaxationDocument27 pagesChapter 3 Introduction To Business TaxationHazel Jane Esclamada100% (1)

- Chapter 2 Tax 2Document7 pagesChapter 2 Tax 2Hazel Jane EsclamadaNo ratings yet

- Elan Guides Formula Sheet CFA 2013 Level 2Document91 pagesElan Guides Formula Sheet CFA 2013 Level 2Igor Tchounkovskii100% (2)

- Microsoft Word - FAR01 - Accounting For Equity InvestmentsDocument4 pagesMicrosoft Word - FAR01 - Accounting For Equity InvestmentsDisguised owlNo ratings yet

- Investment in Equity Securities Intacc1Document3 pagesInvestment in Equity Securities Intacc1GIRLNo ratings yet

- Quiz 3 PDFDocument20 pagesQuiz 3 PDFGirly CrisostomoNo ratings yet

- Quiz 4 - Unit 4 - Investment in Equity Securities Quiz InstructionsDocument22 pagesQuiz 4 - Unit 4 - Investment in Equity Securities Quiz InstructionsCharmaine Mari OlmosNo ratings yet

- CASH QuestionsDocument9 pagesCASH QuestionsKenncyNo ratings yet

- Year Sales Actual Warranty ExpendituresDocument5 pagesYear Sales Actual Warranty ExpendituresMinie KimNo ratings yet

- Intermacc Inventories and Bio Assets Prelec WaDocument1 pageIntermacc Inventories and Bio Assets Prelec WaClarice Awa-aoNo ratings yet

- Chapter 34Document17 pagesChapter 34Mike SerafinoNo ratings yet

- Week 4 - Lesson 4 Cash and Cash EquivalentsDocument21 pagesWeek 4 - Lesson 4 Cash and Cash EquivalentsRose RaboNo ratings yet

- Chapter 18 - Investment in Associate (Other Accounting Issues)Document3 pagesChapter 18 - Investment in Associate (Other Accounting Issues)Liana LopezNo ratings yet

- Retirement Method and Replacement MethodDocument1 pageRetirement Method and Replacement MethodQueenie ValleNo ratings yet

- Inventories Quiz NotesDocument7 pagesInventories Quiz NotesMikaella Nicole PechardoNo ratings yet

- Investment in Equity SecuritiesDocument19 pagesInvestment in Equity SecuritiesNicholai NonanNo ratings yet

- Acc-106 Sas 3Document12 pagesAcc-106 Sas 3hello millieNo ratings yet

- Chapter 1&2 Introduction To Business Taxes & Vat On Sale of Goods or PropertiesDocument6 pagesChapter 1&2 Introduction To Business Taxes & Vat On Sale of Goods or PropertiesBSA3Tagum Marilet100% (1)

- QUIZ 4.1 Investments PDFDocument4 pagesQUIZ 4.1 Investments PDFGirly CrisostomoNo ratings yet

- IAcctg1 Accounts Receivable ActivitiesDocument10 pagesIAcctg1 Accounts Receivable ActivitiesYulrir Alesteyr HiroshiNo ratings yet

- IntAcc-1 Accounting For ReceivablesDocument13 pagesIntAcc-1 Accounting For ReceivablesShekainah BNo ratings yet

- Midterm FarDocument7 pagesMidterm FarShannen D. CalimagNo ratings yet

- Multiple Choice:: Solution 21-1 Answer CDocument5 pagesMultiple Choice:: Solution 21-1 Answer Cleshz zynNo ratings yet

- Problem 4-29 To 31Document1 pageProblem 4-29 To 31maryaniNo ratings yet

- PROBLEM 1 RESA Anna Corp. Uses The Direct Method To Prepare Its Statement of Cash Flows. Anna Corp.'s TrialDocument16 pagesPROBLEM 1 RESA Anna Corp. Uses The Direct Method To Prepare Its Statement of Cash Flows. Anna Corp.'s TrialJomar Villena100% (2)

- Module 5Document14 pagesModule 5Sittie Nihaya MangondayaNo ratings yet

- Illustrative Problem On Acquisition of Net Assets: Entity XY Entity ABDocument2 pagesIllustrative Problem On Acquisition of Net Assets: Entity XY Entity ABjerald cerezaNo ratings yet

- IntAcc Quiz 1 PDFDocument9 pagesIntAcc Quiz 1 PDFMyles Ninon LazoNo ratings yet

- Gross Profit Method CVDocument18 pagesGross Profit Method CVRigine Pobe MorgadezNo ratings yet

- Chapter 5Document20 pagesChapter 5Clyette Anne Flores Borja100% (1)

- Part I: Theory of AccountsDocument6 pagesPart I: Theory of AccountsJanna Mari FriasNo ratings yet

- MAS 8 FS Analysis AnswersDocument15 pagesMAS 8 FS Analysis AnswersKatherine Cabading InocandoNo ratings yet

- Corporate LiquidationDocument7 pagesCorporate LiquidationAcads PurposesNo ratings yet

- Financial Asset at Fair Value Problem 21-1 (IFRS) : Solution 21-1 Answer CDocument15 pagesFinancial Asset at Fair Value Problem 21-1 (IFRS) : Solution 21-1 Answer CAngelo PayawalNo ratings yet

- Integrated Topic 1 (Far-004a)Document4 pagesIntegrated Topic 1 (Far-004a)lyndon delfinNo ratings yet

- Ia3 Review On Notes To FSDocument11 pagesIa3 Review On Notes To FSErich Posillo AranasNo ratings yet

- Accounting For Joint Arrangements Material 1Document5 pagesAccounting For Joint Arrangements Material 1Erika Mae BarizoNo ratings yet

- Prelim Exam - Intermediate Accounting Part 1Document13 pagesPrelim Exam - Intermediate Accounting Part 1Vincent AbellaNo ratings yet

- Examination About Investment 1Document3 pagesExamination About Investment 1BLACKPINKLisaRoseJisooJennieNo ratings yet

- MASTERY CLASS IN AUDITING PROBLEMS Part 1 Prob 1 9Document35 pagesMASTERY CLASS IN AUDITING PROBLEMS Part 1 Prob 1 9Mark Gelo WinchesterNo ratings yet

- Exam in Accounting-FinalsDocument5 pagesExam in Accounting-FinalsIyarna YasraNo ratings yet

- An Entity Reported Current Receivables On December 31Document1 pageAn Entity Reported Current Receivables On December 31pompomNo ratings yet

- Answer:: TotalDocument2 pagesAnswer:: TotalCarla Jane ApolinarioNo ratings yet

- Quiz Chapter 10 Investments in Debt Securities Ia 1 2020 EditionDocument7 pagesQuiz Chapter 10 Investments in Debt Securities Ia 1 2020 EditionChristine Jean MajestradoNo ratings yet

- Financial Assets at Fair Value (Investments) Basic ConceptsDocument2 pagesFinancial Assets at Fair Value (Investments) Basic ConceptsMonica Monica0% (1)

- Exam Results: Question #1Document3 pagesExam Results: Question #1LouiseNo ratings yet

- Quiz in Intacc 1 & 2 (Finals)Document1 pageQuiz in Intacc 1 & 2 (Finals)Sandra100% (1)

- Reviewer in Intermediate Accounting (Midterm)Document9 pagesReviewer in Intermediate Accounting (Midterm)Czarhiena SantiagoNo ratings yet

- Which Statement Is Incorrect Regarding The Application of The Equity Method of Accounting For Investments in AssociatesDocument1 pageWhich Statement Is Incorrect Regarding The Application of The Equity Method of Accounting For Investments in Associatesjahnhannalei marticio0% (1)

- Strategic Cost Management: Short-Term BudgetingDocument12 pagesStrategic Cost Management: Short-Term BudgetingAdrian RoxasNo ratings yet

- Topic 1 Corporate Liquidation - ModuleDocument11 pagesTopic 1 Corporate Liquidation - ModuleJenny LelisNo ratings yet

- ProblemsDocument28 pagesProblemsYou Knock On My DoorNo ratings yet

- Problem 1Document10 pagesProblem 1Shannen D. CalimagNo ratings yet

- Reviewer 1st PB P1 1920Document7 pagesReviewer 1st PB P1 1920Therese AcostaNo ratings yet

- Problem 7 - 22Document3 pagesProblem 7 - 22Jao FloresNo ratings yet

- Nature and Background of The Specialized IndustryDocument3 pagesNature and Background of The Specialized IndustryEly RiveraNo ratings yet

- Chapter 04 SDocument41 pagesChapter 04 SDavid DavidNo ratings yet

- Business Combination1Document5 pagesBusiness Combination1Mae Ciarie YangcoNo ratings yet

- INVESTMENTS W Matrix PFRS 9 PDFDocument7 pagesINVESTMENTS W Matrix PFRS 9 PDFAra DucusinNo ratings yet

- Lupisan-Baysa PDFDocument206 pagesLupisan-Baysa PDFRicart Von LauretaNo ratings yet

- Module Far1 Unit-1 Part-1c.4Document2 pagesModule Far1 Unit-1 Part-1c.4KezNo ratings yet

- Chapter 36 Financial InstrumentsDocument5 pagesChapter 36 Financial InstrumentsEllen MaskariñoNo ratings yet

- Financial Assets at Fair Value CH 15Document14 pagesFinancial Assets at Fair Value CH 15Cheska AgrabioNo ratings yet

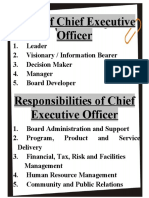

- Report - Roles of CEODocument2 pagesReport - Roles of CEOHazel Jane EsclamadaNo ratings yet

- Photography 2Document48 pagesPhotography 2Hazel Jane EsclamadaNo ratings yet

- Mas 3 Module 1 Fs AnalysisDocument19 pagesMas 3 Module 1 Fs AnalysisHazel Jane EsclamadaNo ratings yet

- MAS-3-Roque - Answer KeyDocument6 pagesMAS-3-Roque - Answer KeyHazel Jane Esclamada100% (1)

- Photography 3 (Updated)Document28 pagesPhotography 3 (Updated)Hazel Jane EsclamadaNo ratings yet

- Introduction To Financial ManagementDocument43 pagesIntroduction To Financial ManagementHazel Jane EsclamadaNo ratings yet

- Introduction To Donor's TaxDocument7 pagesIntroduction To Donor's TaxHazel Jane EsclamadaNo ratings yet

- Inventory Management: Multiple Choice QuestionsDocument3 pagesInventory Management: Multiple Choice QuestionsHazel Jane Esclamada33% (3)

- Reclassification: of Financial AssetsDocument15 pagesReclassification: of Financial AssetsHazel Jane EsclamadaNo ratings yet

- Working Capital FinanceDocument12 pagesWorking Capital FinanceYeoh Mae100% (4)

- Warranties, Provisions and Contingent LiabilitiesDocument31 pagesWarranties, Provisions and Contingent LiabilitiesHazel Jane EsclamadaNo ratings yet

- Topic 4 - EXERCISES6 - Capital Current Liabilities ManagementDocument36 pagesTopic 4 - EXERCISES6 - Capital Current Liabilities ManagementHazel Jane Esclamada100% (1)

- Module Far1 Unit-1 Part-1c.1Document6 pagesModule Far1 Unit-1 Part-1c.1Hazel Jane EsclamadaNo ratings yet

- Introduction To Transfer TaxationDocument6 pagesIntroduction To Transfer TaxationHazel Jane EsclamadaNo ratings yet

- MODULE FinalTerm FAR 3 Operating Segment Interim Reporting Events After Reporting Period 1Document19 pagesMODULE FinalTerm FAR 3 Operating Segment Interim Reporting Events After Reporting Period 1Hazel Jane EsclamadaNo ratings yet

- Concept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Document12 pagesConcept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Hazel Jane Esclamada100% (1)

- Topic 7 Transfer PricingDocument3 pagesTopic 7 Transfer PricingHazel Jane EsclamadaNo ratings yet

- Module 2.1 (Property, Plant, and Equipment)Document15 pagesModule 2.1 (Property, Plant, and Equipment)Hazel Jane EsclamadaNo ratings yet

- What To Do With Perceived Environmental ViolationsDocument15 pagesWhat To Do With Perceived Environmental ViolationsHazel Jane EsclamadaNo ratings yet

- TSU PNP New Rank Classification The Meaning of The Symbols in The Seal and Badge of The PNPDocument3 pagesTSU PNP New Rank Classification The Meaning of The Symbols in The Seal and Badge of The PNPHazel Jane EsclamadaNo ratings yet

- Topic 4 - Current Liabilities Sample ProblemsDocument8 pagesTopic 4 - Current Liabilities Sample ProblemsHazel Jane EsclamadaNo ratings yet

- Chapter 1 Tax 2Document5 pagesChapter 1 Tax 2Hazel Jane EsclamadaNo ratings yet

- Ch3 InvestmentsDocument70 pagesCh3 InvestmentsLiyo MakNo ratings yet

- Notes To Consolidated Financial Statements: Department of EducationDocument65 pagesNotes To Consolidated Financial Statements: Department of EducationEmosNo ratings yet

- Accounting Theory Chapter 6Document5 pagesAccounting Theory Chapter 6nabila IkaNo ratings yet

- Summary of Accounting Standards From Cfas Book CompressDocument34 pagesSummary of Accounting Standards From Cfas Book Compressofficial.kwentoniagimatNo ratings yet

- Fixed AssetsDocument77 pagesFixed AssetsRizkya Kusuma PutriNo ratings yet

- Accounting in IBDocument23 pagesAccounting in IBAbdur RajakNo ratings yet

- Case 4 1Document20 pagesCase 4 1Lamont Clinton100% (3)

- CHAPTER - 3 Conceptual FrameworkDocument14 pagesCHAPTER - 3 Conceptual FrameworkSarva ShivaNo ratings yet

- Accounting 404BDocument2 pagesAccounting 404BMelicah Chantel SantosNo ratings yet

- Amcis Cfs1215 Apex Mining Co SecDocument99 pagesAmcis Cfs1215 Apex Mining Co Sec1234No ratings yet

- Artis Reit - Accounting For Investment Properties Under IfrsDocument3 pagesArtis Reit - Accounting For Investment Properties Under IfrsKatieYoungNo ratings yet

- Yasir ProjectDocument58 pagesYasir Projectaminullah muslimNo ratings yet

- Unit 5 - Financial Reporting and Analysis PDFDocument118 pagesUnit 5 - Financial Reporting and Analysis PDFEstefany MariáteguiNo ratings yet

- The Cpa Licensure Examination Syllabus Financial Accounting and ReportingDocument6 pagesThe Cpa Licensure Examination Syllabus Financial Accounting and ReportingNicole Anne CornejaNo ratings yet

- Conceptual Framework and Accounting Standards 1 Overview of Accounting (Quiz 1)Document6 pagesConceptual Framework and Accounting Standards 1 Overview of Accounting (Quiz 1)Damayan XeroxanNo ratings yet

- Columbus's First VoyageDocument16 pagesColumbus's First VoyagepiyuNo ratings yet

- CFAS Summary Overview, Conceptual Framework, All PasDocument7 pagesCFAS Summary Overview, Conceptual Framework, All PasAiza Bernadette NahialNo ratings yet

- Financial Accounting Tools For Business Decision Making Canadian 6th Edition Kimmel Test BankDocument45 pagesFinancial Accounting Tools For Business Decision Making Canadian 6th Edition Kimmel Test Bankalexanderpetersjtsrqzxacb100% (10)

- Liabilities: Chidelyn Aguado, Marian Andrage, Wincer Alonzaga, Chincel AniDocument57 pagesLiabilities: Chidelyn Aguado, Marian Andrage, Wincer Alonzaga, Chincel AniChincel AniNo ratings yet

- FAMA Individual Assignment: Maruti SuzukiDocument3 pagesFAMA Individual Assignment: Maruti SuzukiRishabh MishraNo ratings yet

- Basics of Book-Keeping and AccountingDocument27 pagesBasics of Book-Keeping and AccountingCA Deepak EhnNo ratings yet

- Toa 1Document9 pagesToa 1Earl Russell S PaulicanNo ratings yet

- Application: Unit 1 - Module 1.1 Topic 1: The Accountancy ProfessionDocument7 pagesApplication: Unit 1 - Module 1.1 Topic 1: The Accountancy ProfessionLi LiNo ratings yet

- Dabur Notes To Consolidated Financial Statements PDFDocument67 pagesDabur Notes To Consolidated Financial Statements PDFRupasinghNo ratings yet

- Assessment Ii,,,,prince's GroupDocument14 pagesAssessment Ii,,,,prince's GroupTafadzwaNo ratings yet

- Accounting Practices and International AccountingDocument23 pagesAccounting Practices and International AccountingAlbert Carl Baltazar IINo ratings yet

- MGT 402 Midterm Solved Papers MCQS File BY MISHAL IQBALDocument21 pagesMGT 402 Midterm Solved Papers MCQS File BY MISHAL IQBALmishal iqbalNo ratings yet

- Date AND Time Learning Area Learning Competencie S Learning Tasks Mode of DeliveryDocument4 pagesDate AND Time Learning Area Learning Competencie S Learning Tasks Mode of DeliveryAvegail SayonNo ratings yet