You might also like

- Law On Public OfficersDocument51 pagesLaw On Public OfficersJetJuárez100% (1)

- Land Transportation Office Vs City of ButuanDocument2 pagesLand Transportation Office Vs City of ButuanJesse MoranteNo ratings yet

- 0275970345Document164 pages0275970345Ana NovovicNo ratings yet

- (Pubcorp Case Digests Part I) : Aquino Vs Mun. of Malay GR NO. 211356, SEPT. 29, 2014Document36 pages(Pubcorp Case Digests Part I) : Aquino Vs Mun. of Malay GR NO. 211356, SEPT. 29, 2014Tet Vergara100% (1)

- Pil & Law On Pub Corpo - San Beda 2013 PDFDocument81 pagesPil & Law On Pub Corpo - San Beda 2013 PDFGonzales Juliefer AnnNo ratings yet

- Beluso Vs Panay Capiz GR 153974Document1 pageBeluso Vs Panay Capiz GR 153974GrefoNo ratings yet

- Penera VS ComelecDocument3 pagesPenera VS Comelecjofred8No ratings yet

- Talaga Jr. v. Sandiganbayan - RA 31019-Contending That The Information-No OffenseDocument7 pagesTalaga Jr. v. Sandiganbayan - RA 31019-Contending That The Information-No OffenseMarlon WankeyNo ratings yet

- 11 - SJS v. LimDocument1 page11 - SJS v. LimMarie ChieloNo ratings yet

- Quezon Vs BayantelDocument3 pagesQuezon Vs BayantelMailah AwingNo ratings yet

- Alinsug Vs RTCDocument3 pagesAlinsug Vs RTCRaymond RoqueNo ratings yet

- City of Manila V IACDocument2 pagesCity of Manila V IACYieMaghirangNo ratings yet

- Calma Vs Lachica and Fudot Vs CattleyaDocument6 pagesCalma Vs Lachica and Fudot Vs CattleyaMikkaEllaAnclaNo ratings yet

- Public Schools District Supervisors Associate Vs de Jesus, GR No. 157299, June 19, 2006Document1 pagePublic Schools District Supervisors Associate Vs de Jesus, GR No. 157299, June 19, 2006geni_pearlc50% (2)

- Demaala v. CoaDocument11 pagesDemaala v. CoaMassabielle100% (1)

- Governor of CagayanDocument4 pagesGovernor of CagayanMykee NavalNo ratings yet

- Corporation Law Case Digests 1Document113 pagesCorporation Law Case Digests 1Arah Mae BonillaNo ratings yet

- 05 City Government of Quezon City V Bayan Telecommunications PDFDocument2 pages05 City Government of Quezon City V Bayan Telecommunications PDFCarla CucuecoNo ratings yet

- Cordillera Board Coalition V Coa CDDocument2 pagesCordillera Board Coalition V Coa CDsharoncerro81No ratings yet

- 46-Quezon City Vs BayantelDocument3 pages46-Quezon City Vs BayantelIshNo ratings yet

- Talaga Jr. V. Sandiganbayan, Et Al., G.R. No. 169888, Nov. 11, 2008Document10 pagesTalaga Jr. V. Sandiganbayan, Et Al., G.R. No. 169888, Nov. 11, 2008Shiela BrownNo ratings yet

- 78.) Farinas vs. Barba (1996)Document3 pages78.) Farinas vs. Barba (1996)AlexandraSoledadNo ratings yet

- Admin - I - 20. Isa Vs CA 249 Scra 538Document2 pagesAdmin - I - 20. Isa Vs CA 249 Scra 538Christine Joy Estropia100% (1)

- Fierro v. Seguiran G.R. No. 152141Document3 pagesFierro v. Seguiran G.R. No. 152141rodel talabaNo ratings yet

- Basco Vs Philippine Amusements and Gaming Corp.Document3 pagesBasco Vs Philippine Amusements and Gaming Corp.Nathalie YapNo ratings yet

- Team Energy CorporationDocument2 pagesTeam Energy CorporationTheodore0176No ratings yet

- City of Lapu-Lapu Vs PezaDocument3 pagesCity of Lapu-Lapu Vs PezaAerwin Abesamis100% (2)

- National Power Corporation vs. The Provincial Treasurer of Benguet, Et Al.Document13 pagesNational Power Corporation vs. The Provincial Treasurer of Benguet, Et Al.red gynNo ratings yet

- Cordillera Board Coalition V COADocument2 pagesCordillera Board Coalition V COAPio MathayNo ratings yet

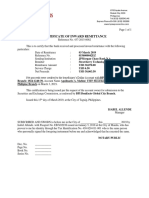

- Certificate of Inward RemittanceDocument1 pageCertificate of Inward RemittanceLauriz EsquivelNo ratings yet

- Bengzon V Senate Blue RibbonDocument3 pagesBengzon V Senate Blue Ribbon上原クリスNo ratings yet

- Cawaling V ComelecDocument2 pagesCawaling V ComelecKarla KanashiiNo ratings yet

- Pablico Vs Villapando Case DigestDocument2 pagesPablico Vs Villapando Case DigestJan Kenrick SagumNo ratings yet

- Almonte v. Vasquez Case DigestDocument3 pagesAlmonte v. Vasquez Case DigestNxxxNo ratings yet

- Digest BodyDocument79 pagesDigest BodyLauriz EsquivelNo ratings yet

- LTO v. City of ButuanDocument2 pagesLTO v. City of ButuanChariNo ratings yet

- Acord V Zamora DigestDocument2 pagesAcord V Zamora DigestMis DeeNo ratings yet

- Penera Vs Comelec Nov 25Document2 pagesPenera Vs Comelec Nov 25Naldy John Delos SantosNo ratings yet

- Ong v. AlegreDocument2 pagesOng v. AlegreNoreenesse SantosNo ratings yet

- Malaga vs. Penachos, 213 SCRA 516Document12 pagesMalaga vs. Penachos, 213 SCRA 516Mak Francisco100% (1)

- THE UNITED STATES, Plaintiff-Appellee, vs. PRUDENCIO SALAVERIA, DefendantDocument8 pagesTHE UNITED STATES, Plaintiff-Appellee, vs. PRUDENCIO SALAVERIA, DefendantLauriz EsquivelNo ratings yet

- Pub Corp - Case Digests 06 (Word)Document40 pagesPub Corp - Case Digests 06 (Word)Odette JumaoasNo ratings yet

- Administrative Investigations and Appeals: GR No. 160791 - Sales v. Carreon JRDocument1 pageAdministrative Investigations and Appeals: GR No. 160791 - Sales v. Carreon JRjci028No ratings yet

- Certificate of Inward RemittanceDocument1 pageCertificate of Inward RemittanceLauriz EsquivelNo ratings yet

- CD - 20. RCPI v. Provincial AssessorDocument1 pageCD - 20. RCPI v. Provincial AssessorAlyssa Alee Angeles JacintoNo ratings yet

- City Gov't of QC vs. Bayan Telecom, Inc Tax1 #49 KPGDocument2 pagesCity Gov't of QC vs. Bayan Telecom, Inc Tax1 #49 KPGKenneth GeolinaNo ratings yet

- Villegas vs. SubidoDocument6 pagesVillegas vs. Subidorols villanezaNo ratings yet

- Camarines Norte Electric Cooperative Vs TorresDocument8 pagesCamarines Norte Electric Cooperative Vs TorresTats YumulNo ratings yet

- Pub Cor Reviewer PDFDocument14 pagesPub Cor Reviewer PDFnomercykillingNo ratings yet

- 2943 PDFDocument368 pages2943 PDFSaturnina100% (2)

- Final - C5 and C6 de Leon - Concepts in The Law On Public OfficersDocument27 pagesFinal - C5 and C6 de Leon - Concepts in The Law On Public OfficersTep DomingoNo ratings yet

- Administrative Law Cases Chapter 1 PDFDocument14 pagesAdministrative Law Cases Chapter 1 PDFNiel Edar BallezaNo ratings yet

- Tuzon V CA - CMDocument3 pagesTuzon V CA - CMjustinegalangNo ratings yet

- G.R. No. 166102Document1 pageG.R. No. 166102kaye choiNo ratings yet

- Diaz V Secretary of FinanceDocument2 pagesDiaz V Secretary of FinanceTrxc MagsinoNo ratings yet

- 10 Manila Electric v. The City Assessor and City Treasurer of Lucena City PDFDocument47 pages10 Manila Electric v. The City Assessor and City Treasurer of Lucena City PDFClarinda MerleNo ratings yet

- Land Bank of The Philippines, Petitioner, Court of AppealsDocument7 pagesLand Bank of The Philippines, Petitioner, Court of AppealsPaulo De SilvaNo ratings yet

- 203 Macalincag v. ChangDocument1 page203 Macalincag v. ChangAlexa LeeNo ratings yet

- 42.taule Vs Sec - of Local GovDocument2 pages42.taule Vs Sec - of Local GovRey David LimNo ratings yet

- Disomangcop v. Datumanong-444 SCRA 203 (2004)Document1 pageDisomangcop v. Datumanong-444 SCRA 203 (2004)Jeorge Ryan MangubatNo ratings yet

- Favis Vs City of BaguioDocument1 pageFavis Vs City of BaguioKIMMYNo ratings yet

- G.R. No. L-5279Document11 pagesG.R. No. L-5279kai lumagueNo ratings yet

- Case Digest Consti!Document2 pagesCase Digest Consti!Roger John Caballero Fariñas IINo ratings yet

- PubCorp Case Digest Incomplete Sept 20 2018Document38 pagesPubCorp Case Digest Incomplete Sept 20 2018Celestino LawNo ratings yet

- Public Corporations - Sotelo ReviewerDocument8 pagesPublic Corporations - Sotelo ReviewerSean HinolanNo ratings yet

- 6 Eastern Telecom vs. ICC Case DigestDocument3 pages6 Eastern Telecom vs. ICC Case DigestJaja GkNo ratings yet

- The Law of Allotments and Allotment Gardens (England and Wales)From EverandThe Law of Allotments and Allotment Gardens (England and Wales)No ratings yet

- Ii. Quasi-Delict A. Elements: FactsDocument2 pagesIi. Quasi-Delict A. Elements: FactsLauriz EsquivelNo ratings yet

- 5 Consti 6th - Funda Powers TableDocument1 page5 Consti 6th - Funda Powers TableLauriz EsquivelNo ratings yet

- Separation of Church and StateDocument3 pagesSeparation of Church and StateLauriz EsquivelNo ratings yet

- 4B Consti 5th True RaemondDocument2 pages4B Consti 5th True RaemondLauriz EsquivelNo ratings yet

- Determination of Probable Cause: GR 171465 (8 June 2007) J. Ynares-SantiagoDocument8 pagesDetermination of Probable Cause: GR 171465 (8 June 2007) J. Ynares-SantiagoLauriz EsquivelNo ratings yet

- Bill of Rights FDocument7 pagesBill of Rights FLauriz EsquivelNo ratings yet

- Facts:: Austria - Cuanan - Dupaya - Liwanag - Manuel - Paguio - Pion - Santiago - Untalan - ZaragozaDocument10 pagesFacts:: Austria - Cuanan - Dupaya - Liwanag - Manuel - Paguio - Pion - Santiago - Untalan - ZaragozaLauriz EsquivelNo ratings yet

- I and II Cases - Full TextDocument703 pagesI and II Cases - Full TextLauriz EsquivelNo ratings yet

- Facts:: Bill of Rights A. Fundamental Powers of The StateDocument12 pagesFacts:: Bill of Rights A. Fundamental Powers of The StateLauriz EsquivelNo ratings yet

- NPC Drivers and Mechanics Association (NPC-DAMA) Versus National Power CorporationDocument26 pagesNPC Drivers and Mechanics Association (NPC-DAMA) Versus National Power CorporationLauriz EsquivelNo ratings yet

- An Act Providing For The Revised Corporation Code of The PhilippinesDocument55 pagesAn Act Providing For The Revised Corporation Code of The PhilippinesLauriz EsquivelNo ratings yet

- Ruks Konsult vs. Adworld SignDocument11 pagesRuks Konsult vs. Adworld SignLauriz EsquivelNo ratings yet

- Clariza A. Reyes Atty. Crisostomo Uribe Civil Law Review II Sunday 1:00-5:00pm April 7, 2019Document4 pagesClariza A. Reyes Atty. Crisostomo Uribe Civil Law Review II Sunday 1:00-5:00pm April 7, 2019Lauriz EsquivelNo ratings yet

- Frequency of Scores: Jose Abad Santos High School Quarter: Grade Level: School Year: HpsDocument23 pagesFrequency of Scores: Jose Abad Santos High School Quarter: Grade Level: School Year: HpsLauriz EsquivelNo ratings yet

- NPC Drivers and Mechanics Association (NPC-DAMA) vs. National Power Corporation (NPC), 503 SCRA 138, G.R. No. 156208 September 26, 2006Document8 pagesNPC Drivers and Mechanics Association (NPC-DAMA) vs. National Power Corporation (NPC), 503 SCRA 138, G.R. No. 156208 September 26, 2006Lauriz EsquivelNo ratings yet

- Poli Rev Digest GeneralDocument4 pagesPoli Rev Digest GeneralLauriz EsquivelNo ratings yet

- Deal Maeled SLTDocument3 pagesDeal Maeled SLTLauriz EsquivelNo ratings yet

- Frozen Ice Prod. CostDocument2 pagesFrozen Ice Prod. CostLauriz EsquivelNo ratings yet

- Sample - 26 Escol, Hanzel GraceDocument31 pagesSample - 26 Escol, Hanzel GraceLauriz EsquivelNo ratings yet

- Orms of Usiness Rganisation: HapterDocument31 pagesOrms of Usiness Rganisation: HapterPrabakaran V.No ratings yet

- Income Tax Planning in India With Respect To Individual AssesseeDocument100 pagesIncome Tax Planning in India With Respect To Individual AssesseeMosam AliNo ratings yet

- Oncell G3111/G3151/G3211/G3251 Series User'S Manual: Edition 3.1, October 2016Document147 pagesOncell G3111/G3151/G3211/G3251 Series User'S Manual: Edition 3.1, October 2016elvis1281No ratings yet

- Content and Contextual Analysis of Selected Primary Sources: Intended Learning OutcomeDocument21 pagesContent and Contextual Analysis of Selected Primary Sources: Intended Learning OutcomeJAN VEN CONRAD DE VILLANo ratings yet

- INE721A08DE4 Shriram Transport Finance Company Limited 2024Document3 pagesINE721A08DE4 Shriram Transport Finance Company Limited 2024speedenquiryNo ratings yet

- Assignment Percentage Tax ComputationDocument2 pagesAssignment Percentage Tax ComputationAngelyn SamandeNo ratings yet

- Rfa 2018 en nl0000349488Document184 pagesRfa 2018 en nl0000349488hoiruNo ratings yet

- Municipality of BayambangDocument2 pagesMunicipality of BayambangMPDO LGU San AndresNo ratings yet

- Leaving The Euro A Practical Guide SummaryDocument3 pagesLeaving The Euro A Practical Guide SummaryTee RexNo ratings yet

- Form PDFDocument2 pagesForm PDFTahseena WaseemNo ratings yet

- ScribdDocument10 pagesScribdJon StewartNo ratings yet

- Lecture 1 LawDocument23 pagesLecture 1 LawLanestosa Ernest Rey B.No ratings yet

- Bank Ganesha TBKDocument3 pagesBank Ganesha TBKTam sneakersNo ratings yet

- AssignmentDocument2 pagesAssignmentMichael AllenNo ratings yet

- Axis BankDocument16 pagesAxis Bankalokascribd60% (5)

- Berkshire HathawayDocument25 pagesBerkshire HathawayRohit SNo ratings yet

- Unaudited Financial Statements - March 2022Document27 pagesUnaudited Financial Statements - March 2022Aryan MahajanNo ratings yet

- 1-7 Buck Ruxton & The Jigsaw Murders Case v1Document9 pages1-7 Buck Ruxton & The Jigsaw Murders Case v1Francisco GonzálezNo ratings yet

- AaccDocument8 pagesAaccapi-243316402No ratings yet

- Discharge of ContractDocument6 pagesDischarge of ContractShahzad BhattiNo ratings yet

- Triton VGT EuroDocument9 pagesTriton VGT EuroEncik AzmieNo ratings yet

- JJ-SP-PL-0002-JJ Human RightsDocument3 pagesJJ-SP-PL-0002-JJ Human RightsJulian SandovalNo ratings yet

- Gimc 2017 Researcher TestDocument12 pagesGimc 2017 Researcher TestRaghavendra SinghNo ratings yet

- Revised Cont - Asses - Grade (13.11.14, 2.31 AM)Document115 pagesRevised Cont - Asses - Grade (13.11.14, 2.31 AM)Aminul RanaNo ratings yet

- Code of Ethics SlacDocument41 pagesCode of Ethics SlacJasmin Move-Ramirez67% (3)

- Income Under The Head "Salary"Document15 pagesIncome Under The Head "Salary"NITESH SINGHNo ratings yet

- FR Phase 2 - TestDocument5 pagesFR Phase 2 - TestMayank GoyalNo ratings yet