You might also like

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hoshin Kanri - From Strategy To Individual Goal Planning: Julie Miller Integrys Energy Services Session M26Document33 pagesHoshin Kanri - From Strategy To Individual Goal Planning: Julie Miller Integrys Energy Services Session M26rarevalo11No ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- SCM 1Document16 pagesSCM 1glcpaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Strategy & Strategic PlanningDocument9 pagesStrategy & Strategic PlanningThe Natak CompanyNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- SamsungDocument38 pagesSamsungkihtraka50% (2)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

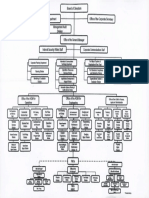

- PPA Organizational ChartDocument1 pagePPA Organizational ChartJohn Wendell Fontanilla FerrerNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Marketing Management Sample 2024Document32 pagesMarketing Management Sample 2024Vibrant PublishersNo ratings yet

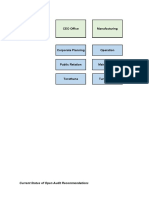

- Internal Audit Dashboard Ver. 1Document18 pagesInternal Audit Dashboard Ver. 1Fazal KarimNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team Effectiveness Survey Workbook - Bauer - Robert W. (Author)Document161 pagesTeam Effectiveness Survey Workbook - Bauer - Robert W. (Author)JOHAN FERNANDO QUIROZ SERNAQUE100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Validation of SAP R/3 in Compliance With Part 11 RequirementsDocument46 pagesValidation of SAP R/3 in Compliance With Part 11 RequirementsSuraj Pratap PhalkeNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- AmazonDocument19 pagesAmazonAli Al KaabiNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- At MCQ Salogsacol Auditing Theory Multiple ChoiceDocument32 pagesAt MCQ Salogsacol Auditing Theory Multiple Choicealmira garciaNo ratings yet

- AdvertisementsDocument71 pagesAdvertisementsRohanNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Abor & Adjasi, 2007Document14 pagesAbor & Adjasi, 2007novie endi nugrohoNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Employer Branding: What and How?Document10 pagesEmployer Branding: What and How?Cătălin HuștiuNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Strategic Management and AnalysisDocument7 pagesStrategic Management and AnalysisLisaNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Business Analyst Interview Questions With AnswersDocument4 pagesBusiness Analyst Interview Questions With AnswersSathish Selvaraj67% (3)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Thesis Warehouse Management SystemDocument4 pagesThesis Warehouse Management Systemmvlnfvfig100% (2)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- VP ResumeDocument5 pagesVP Resumekenosab0hok3100% (1)

- Supply Chain ManagementDocument13 pagesSupply Chain Managementvimal100% (1)

- LA020504 Ass1 BSBMGT517 Ed2Document6 pagesLA020504 Ass1 BSBMGT517 Ed2ghasepNo ratings yet

- CEO President Risk Management in Atlanta GA Resume Charles "Bill" FordDocument3 pagesCEO President Risk Management in Atlanta GA Resume Charles "Bill" FordCharlesBillFordNo ratings yet

- Training and Development Policy and ProceduresDocument1 pageTraining and Development Policy and ProceduresJOSPHAT ETALE B.E AERONAUTICAL ENGINEERNo ratings yet

- Strategic Outsourcing at Bharti Airtel: Should Network and IT Infrastructure be OutsourcedDocument9 pagesStrategic Outsourcing at Bharti Airtel: Should Network and IT Infrastructure be OutsourcedNIKHILA TUMMALANo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- B2B Commerce GuideDocument19 pagesB2B Commerce GuideivanpmnNo ratings yet

- Human Resource Management: Sub Code 556Document330 pagesHuman Resource Management: Sub Code 556jugal bariNo ratings yet

- HR Outsourcing, Outplacement and Pre - TrainingDocument14 pagesHR Outsourcing, Outplacement and Pre - TrainingSreedharan MadhuramattamNo ratings yet

- 2494-Article Text-7214-1-10-20230228Document14 pages2494-Article Text-7214-1-10-20230228ImWatch YouNo ratings yet

- Piata Publicatiilor 2012-2020 - Prezentare RezumativaDocument5 pagesPiata Publicatiilor 2012-2020 - Prezentare RezumativamanageranticrizaNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Competitiveness, Strategy, and ProductivityDocument9 pagesCompetitiveness, Strategy, and ProductivityblankNo ratings yet

- Value Merchants Anderson eDocument5 pagesValue Merchants Anderson esarah123No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)