You might also like

- 13 o Entrepreneurial Govt Attitude To PerformaceDocument14 pages13 o Entrepreneurial Govt Attitude To PerformaceTerryDemetrioCesarNo ratings yet

- ABC and CashFlow QuestionDocument11 pagesABC and CashFlow QuestionTerryDemetrioCesarNo ratings yet

- International BusinessDocument10 pagesInternational BusinessTerryDemetrioCesarNo ratings yet

- Strategic Business Plan For An Innovative Tutoring and Study CenterDocument32 pagesStrategic Business Plan For An Innovative Tutoring and Study CenterTerryDemetrioCesar0% (1)

- Car Loan ProcedureDocument3 pagesCar Loan ProcedureTerryDemetrioCesarNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Jagadguru Dattatray College of TechnologyDocument8 pagesJagadguru Dattatray College of TechnologyRitesh MishraNo ratings yet

- JKSW Annual Report 2017Document54 pagesJKSW Annual Report 2017Riski Nurida RahmawatiNo ratings yet

- Himatsingka Seida LTD.: Valuation Summary SheetDocument6 pagesHimatsingka Seida LTD.: Valuation Summary SheetNeetesh DohareNo ratings yet

- Equity Valuation of MaricoDocument18 pagesEquity Valuation of MaricoPriyanka919100% (1)

- Globalisation BrochureDocument43 pagesGlobalisation Brochurerobertod2003No ratings yet

- AuditingDocument19 pagesAuditingUsman Khalid100% (1)

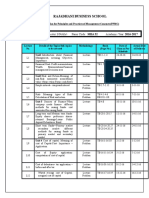

- Rajadhani Business School: Programme: MBA Trimester:3 (Noble) Paper Code: MBA 32 Academic Year: 2016-2017Document3 pagesRajadhani Business School: Programme: MBA Trimester:3 (Noble) Paper Code: MBA 32 Academic Year: 2016-2017Manoj AnandNo ratings yet

- VFC Lee Wrangler Separation Spin Deck PPT PDF Investor Presentation Aug 2018Document25 pagesVFC Lee Wrangler Separation Spin Deck PPT PDF Investor Presentation Aug 2018Ala BasterNo ratings yet

- Seg Funds N Annuities PDFDocument258 pagesSeg Funds N Annuities PDFTaz0007No ratings yet

- 26 International Financial Reporting StandardsDocument3 pages26 International Financial Reporting StandardsClyleo Eddard YoupaNo ratings yet

- Business Taxation: History of Income Tax Law in PakistanDocument26 pagesBusiness Taxation: History of Income Tax Law in PakistanMUHAMMAD UMARNo ratings yet

- Cash Flow EstimationDocument10 pagesCash Flow EstimationRohit BajpaiNo ratings yet

- Topic 1Document59 pagesTopic 1anesuNo ratings yet

- 8 Capital Budgeting - Problems - With AnswersDocument15 pages8 Capital Budgeting - Problems - With AnswersIamnti domnateNo ratings yet

- Chapter 4Document24 pagesChapter 4FăÍż SăįYąðNo ratings yet

- Nasty Gal Case Paper Evaluation HD - High Distinction 80%+ For Student ReferenceDocument133 pagesNasty Gal Case Paper Evaluation HD - High Distinction 80%+ For Student ReferenceJe Bobo100% (1)

- Chapter 2 Part 1 - Ratio AnalysisDocument23 pagesChapter 2 Part 1 - Ratio AnalysisMohamed HosnyNo ratings yet

- Investor Presentation (Company Update)Document34 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Exam - Chapter 006Document19 pagesExam - Chapter 006abdullahsikander4237No ratings yet

- General Form 57 ADocument2 pagesGeneral Form 57 AMIKHAELA CZHARENE75% (4)

- Round 1 Written TestDocument24 pagesRound 1 Written Testapi-344837074No ratings yet

- Big C Supercenter: Tough Year AheadDocument10 pagesBig C Supercenter: Tough Year AheadVishan SharmaNo ratings yet

- New Central Bank ActDocument39 pagesNew Central Bank ActdollyccruzNo ratings yet

- Interest RatesDocument8 pagesInterest RatesMuhammad Sanawar ChaudharyNo ratings yet

- CE Principles of Accounts 1999 PaperDocument8 pagesCE Principles of Accounts 1999 Paperapi-3747191No ratings yet

- Salaries and WagesDocument37 pagesSalaries and WagesJay Ey Betchaida100% (3)

- MAS - 1.2.5 Integrated Review & Refresher in Accountancy R.D.BalocatingDocument6 pagesMAS - 1.2.5 Integrated Review & Refresher in Accountancy R.D.BalocatingLOUISE ELIJAH GACUANNo ratings yet

- (2011) Markstrat Final Report - Team ADocument21 pages(2011) Markstrat Final Report - Team AFilippo Vescovo33% (3)

- CHP 5 - De&ohDocument25 pagesCHP 5 - De&ohBhargav UpadhyayNo ratings yet

- Eco Final ProjectDocument20 pagesEco Final ProjectvedangmishraNo ratings yet