You might also like

- TRPB 1 0764821306 PDFDocument6 pagesTRPB 1 0764821306 PDFcarizaNo ratings yet

- Customer Loyalty & Private Label Products: KPMG Global Consumer MarketsDocument36 pagesCustomer Loyalty & Private Label Products: KPMG Global Consumer Marketsramjee prasad jaiswalNo ratings yet

- Cost Accounting Matz & Usry 7 EditionDocument24 pagesCost Accounting Matz & Usry 7 Editionsaira22pafNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument7 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledJuan Carlos BorbonNo ratings yet

- Foreign Investment ActDocument5 pagesForeign Investment ActMichelle Joy ItableNo ratings yet

- R.A. 7042 Foreign Investments ActDocument5 pagesR.A. 7042 Foreign Investments ActAngela Marie AlmalbisNo ratings yet

- PHilippines Foreign Investments ActDocument6 pagesPHilippines Foreign Investments ActRafael JuicoNo ratings yet

- Ra 7042Document4 pagesRa 7042Paulo SantosNo ratings yet

- Foreign Investments ActDocument10 pagesForeign Investments ActIah LincoNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument42 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledWayne Nathaneal E. ParulanNo ratings yet

- Foreign Investment Act of 1991Document11 pagesForeign Investment Act of 1991Francis M. TabajondaNo ratings yet

- Corporation Organized Under The Laws of The PhilippinesDocument5 pagesCorporation Organized Under The Laws of The PhilippinesMasa LynNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument8 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledParis LisonNo ratings yet

- Foreign Investments Act of 1991Document10 pagesForeign Investments Act of 1991Catherine DavidNo ratings yet

- The Role of Multinational Corporation in The Global EconomnyDocument30 pagesThe Role of Multinational Corporation in The Global EconomnyJmNo ratings yet

- RA 7042 Foreign Investments Act 1991Document9 pagesRA 7042 Foreign Investments Act 1991Lien PatrickNo ratings yet

- Foreign Investment Act of 1991 - Implementing RulesDocument9 pagesForeign Investment Act of 1991 - Implementing RulesCrislene Cruz100% (1)

- Foreign Investment ActDocument8 pagesForeign Investment ActJámie LatNo ratings yet

- Commercial LawsDocument70 pagesCommercial LawsHoneylyn Jiza WaycoNo ratings yet

- Philippines - Foreign Investment Act (English)Document9 pagesPhilippines - Foreign Investment Act (English)Starr WeigandNo ratings yet

- Foreign Investments Act of 1991Document5 pagesForeign Investments Act of 1991Marien Gonzales LopezNo ratings yet

- 4.22.23 Foreign Investment ActDocument4 pages4.22.23 Foreign Investment ActANTHONY REY BAYHONNo ratings yet

- Foreign Investments Act of 1991Document12 pagesForeign Investments Act of 1991JovyNo ratings yet

- Foreign Investment ActDocument9 pagesForeign Investment ActCiri-an TabiraoNo ratings yet

- R.A. 7042 (Foreign Investments Act)Document5 pagesR.A. 7042 (Foreign Investments Act)Ya Ni TaNo ratings yet

- R.A. 7042 - "Foreign Investments Act of 1991Document5 pagesR.A. 7042 - "Foreign Investments Act of 1991Dena ValdezNo ratings yet

- R.A. 7042 Foreign Investments Act of 1991. Board of InvestmentsDocument7 pagesR.A. 7042 Foreign Investments Act of 1991. Board of InvestmentsMARIA LOURDES NITA FAUSTONo ratings yet

- Republic Act No. 7042Document55 pagesRepublic Act No. 7042Prasef Karl Andres Cortes IIINo ratings yet

- Foreign Investment 1991 RA 7042Document44 pagesForeign Investment 1991 RA 7042MikhailFAbzNo ratings yet

- Republic Act NoDocument42 pagesRepublic Act NoZandrina RatertaNo ratings yet

- Foreign Investments Act of 1991Document6 pagesForeign Investments Act of 1991AnDrew Bautista CayabyabNo ratings yet

- Foreign Investment ActDocument5 pagesForeign Investment ActkobechowNo ratings yet

- Foreign Investments ActDocument3 pagesForeign Investments ActAmanda ButtkissNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument4 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress Assembledalyza arra mallareNo ratings yet

- Official Gazette of The Republic of The PhilippinesDocument10 pagesOfficial Gazette of The Republic of The PhilippinesHestia VestaNo ratings yet

- Outline in Corporation LDocument91 pagesOutline in Corporation LmkabNo ratings yet

- Asia Pacific Marketing Forum - Doing Business in The PhilippinesDocument10 pagesAsia Pacific Marketing Forum - Doing Business in The PhilippinesDan CastilloNo ratings yet

- Foreign Investments ActDocument14 pagesForeign Investments ActPattyNo ratings yet

- Fia 1991Document13 pagesFia 1991Lady Paul SyNo ratings yet

- Foreign Investment ActDocument4 pagesForeign Investment ActPBWGNo ratings yet

- Ra 7042 Foreign Investment ActDocument2 pagesRa 7042 Foreign Investment ActMark Hiro NakagawaNo ratings yet

- An Act To Promote Foreign Investments, Prescribe THE Procedures FOR Registering Enterprises Doing Business in The Philippines, and For Other PurposesDocument7 pagesAn Act To Promote Foreign Investments, Prescribe THE Procedures FOR Registering Enterprises Doing Business in The Philippines, and For Other PurposesMary.Rose RosalesNo ratings yet

- Assignment No.2-Retail-implementing Rules and RegulationsDocument15 pagesAssignment No.2-Retail-implementing Rules and RegulationscefyNo ratings yet

- Week 6 LawsDocument2 pagesWeek 6 LawsAnonymous 6suAq5rWENo ratings yet

- IRR of Republic Act No 7042Document21 pagesIRR of Republic Act No 7042andrea ibanezNo ratings yet

- Foreign Investments ActDocument3 pagesForeign Investments ActPrisiclla C CarfelNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument20 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledKrissa Jennesca TulloNo ratings yet

- Omnibus Investment Code of 1987Document8 pagesOmnibus Investment Code of 1987Mary Nespher DelfinNo ratings yet

- Foreign Investment Act of 1991 - : 1. Concept of Negative ListDocument4 pagesForeign Investment Act of 1991 - : 1. Concept of Negative ListrheyneNo ratings yet

- Written Report IILDocument4 pagesWritten Report IILMilesNo ratings yet

- Spec. Com - FIA and Magna Carta For MSMEsDocument11 pagesSpec. Com - FIA and Magna Carta For MSMEsShannon WilkinsNo ratings yet

- Doing Business in The PhilippinesDocument29 pagesDoing Business in The Philippinestakyous100% (1)

- Foreign Investments Acts)Document9 pagesForeign Investments Acts)BABYLEN BAHALANo ratings yet

- 2018 Doing Business in The PhilippinesDocument37 pages2018 Doing Business in The PhilippinesRojbNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument4 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledALEXANDRIA RABANESNo ratings yet

- Eo 226Document25 pagesEo 226givemeasign24No ratings yet

- Foreign CorporationsDocument11 pagesForeign Corporationsjoyiveeong0% (1)

- Foreign Investment Act RA 7042 As Amended by RA 8179 RA 11647Document2 pagesForeign Investment Act RA 7042 As Amended by RA 8179 RA 11647devillaleizel12No ratings yet

- Omnibus Investment Code of 1987Document8 pagesOmnibus Investment Code of 1987Negros Solar PHNo ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- PSCO 2020 Small Town Lottery Revised Implementing Rules and RegulationsDocument30 pagesPSCO 2020 Small Town Lottery Revised Implementing Rules and RegulationsDiorVelasquezNo ratings yet

- Outline in Credit Transactions 2016-2017Document13 pagesOutline in Credit Transactions 2016-2017DiorVelasquezNo ratings yet

- Hmo PPT Part 1 and 2Document31 pagesHmo PPT Part 1 and 2DiorVelasquez100% (1)

- HmoDocument35 pagesHmoDiorVelasquezNo ratings yet

- Easement: Valisno v. Adriano G.R. No. L-37409, May 23, 1988, 161 SCRA 398 Grino - Aquino, JDocument43 pagesEasement: Valisno v. Adriano G.R. No. L-37409, May 23, 1988, 161 SCRA 398 Grino - Aquino, JDiorVelasquezNo ratings yet

- Central Phil. University v. CA 246 SCRA 511 DoctrineDocument13 pagesCentral Phil. University v. CA 246 SCRA 511 DoctrineDiorVelasquezNo ratings yet

- Easement: Valisno v. Adriano G.R. No. L-37409, May 23, 1988, 161 SCRA 398 Grino - Aquino, JDocument47 pagesEasement: Valisno v. Adriano G.R. No. L-37409, May 23, 1988, 161 SCRA 398 Grino - Aquino, JDiorVelasquezNo ratings yet

- Feminist Legal Methods by BartlettDocument46 pagesFeminist Legal Methods by BartlettDiorVelasquezNo ratings yet

- Reports To Treaty Bodies: Lyceum of The Philippines University College of LawDocument20 pagesReports To Treaty Bodies: Lyceum of The Philippines University College of LawDiorVelasquezNo ratings yet

- Flipkart Customer Care Mail PDFDocument2 pagesFlipkart Customer Care Mail PDFAvik DasNo ratings yet

- SR No. Component Data Type Length Sort DescriptionDocument4 pagesSR No. Component Data Type Length Sort DescriptionAnonymous EB4o01No ratings yet

- Exampundit - In: Insurance Awareness Expected Questions - Part 1Document3 pagesExampundit - In: Insurance Awareness Expected Questions - Part 1ANNENo ratings yet

- Nervous Markets: Morning ReportDocument3 pagesNervous Markets: Morning Reportnaudaslietas_lvNo ratings yet

- Camaprative Study of NSE and BSE PDFDocument100 pagesCamaprative Study of NSE and BSE PDFsobha singhNo ratings yet

- Emaar ScamDocument14 pagesEmaar ScamSidharth GuptaNo ratings yet

- Deloitte 2019 Global Impact ReportDocument46 pagesDeloitte 2019 Global Impact ReportDeloitte MaltaNo ratings yet

- SFM Past 10 Year PapersDocument450 pagesSFM Past 10 Year PapersAkash Kumar100% (1)

- EP India 2013-14Document191 pagesEP India 2013-14dbircs1981No ratings yet

- Working Capital Management in Tata Steel LimitedDocument8 pagesWorking Capital Management in Tata Steel LimitedImpact JournalsNo ratings yet

- No 14 - The Late Lino Gutierrez V Collector of Internal RevenueDocument2 pagesNo 14 - The Late Lino Gutierrez V Collector of Internal RevenueA Paula Cruz FranciscoNo ratings yet

- A Typology of Strategic Alliances in The Airline IndustryDocument13 pagesA Typology of Strategic Alliances in The Airline IndustrynantateaNo ratings yet

- Closed Corporation PowerpointDocument18 pagesClosed Corporation PowerpointLen-Len CobsilenNo ratings yet

- ObligationsDocument1 pageObligationsPearl AudeNo ratings yet

- Project Report - Study and Comparative Analysis of Special Loyalty Program Run by Telecom Operator - Vodafone - Jaipur (Raj.)Document103 pagesProject Report - Study and Comparative Analysis of Special Loyalty Program Run by Telecom Operator - Vodafone - Jaipur (Raj.)Ritesh GoyalNo ratings yet

- 6J Store - WPDocument99 pages6J Store - WPAngelo LabiosNo ratings yet

- Tan Tiong Bio V CIRDocument8 pagesTan Tiong Bio V CIRParis LisonNo ratings yet

- Power, Function and Duties of Directors andDocument20 pagesPower, Function and Duties of Directors andHimanshu JainNo ratings yet

- Defensive Tactic M&ADocument4 pagesDefensive Tactic M&AMapleKoleksiNo ratings yet

- Debtors' Motion For Entry of An Order Authorization and Approving The Debtors 2018 IncentiveDocument75 pagesDebtors' Motion For Entry of An Order Authorization and Approving The Debtors 2018 IncentiveDigital Music NewsNo ratings yet

- EU Company Law-Introduction and SourcesDocument40 pagesEU Company Law-Introduction and SourcesTeodor MilanovićNo ratings yet

- 1 An Overview of Financial ManagementDocument14 pages1 An Overview of Financial ManagementSadia AfrinNo ratings yet

- Daisy Lifebasix PDFDocument8 pagesDaisy Lifebasix PDFCharlene G GalesNo ratings yet

- GT Gold Corp. Corporate-PresentationDocument31 pagesGT Gold Corp. Corporate-PresentationkaiselkNo ratings yet

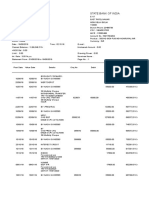

- Statement of Account: State Bank of IndiaDocument2 pagesStatement of Account: State Bank of Indiagaurav sharmaNo ratings yet

- Salehi - 2011 - Audit Expectation Gap - Concept, Nature and TraceDocument17 pagesSalehi - 2011 - Audit Expectation Gap - Concept, Nature and TracethoritruongNo ratings yet

- Directive 4.23 Ensuring Audit QualityDocument3 pagesDirective 4.23 Ensuring Audit QualityAsjad MobeenNo ratings yet