You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Sweeney in MaDocument21 pagesSweeney in Maashes_xNo ratings yet

- Financial Accounting Chapter 1Document67 pagesFinancial Accounting Chapter 1Ana BustoNo ratings yet

- Company ProfileDocument5 pagesCompany ProfileLester BugosNo ratings yet

- GT Gold Corp. Corporate-PresentationDocument31 pagesGT Gold Corp. Corporate-PresentationkaiselkNo ratings yet

- ePCS DOC 01 3Document17 pagesePCS DOC 01 3iker88No ratings yet

- AP Debt WaiverDocument10 pagesAP Debt WaiverChandra ReddyNo ratings yet

- Report of Chandrasekhar Committee On Venture CapitalDocument43 pagesReport of Chandrasekhar Committee On Venture CapitalA SenthilkumarNo ratings yet

- Code of Business Conduct and EthicsDocument2 pagesCode of Business Conduct and EthicsSam GitongaNo ratings yet

- EP India 2013-14Document191 pagesEP India 2013-14dbircs1981No ratings yet

- Power, Function and Duties of Directors andDocument20 pagesPower, Function and Duties of Directors andHimanshu JainNo ratings yet

- Phoenix Coyotes Season Ticket License Terms and ConditionsDocument2 pagesPhoenix Coyotes Season Ticket License Terms and ConditionsArizona CoyotesNo ratings yet

- Sales Availability For Hayyan VillasDocument4 pagesSales Availability For Hayyan VillaspanishaalaNo ratings yet

- Tan Tiong Bio V CIRDocument8 pagesTan Tiong Bio V CIRParis LisonNo ratings yet

- TCL Sales Vs CADocument9 pagesTCL Sales Vs CAasnia07No ratings yet

- Issuances & Rulings Revenue Regulations (RRS) : Digest Full TextDocument65 pagesIssuances & Rulings Revenue Regulations (RRS) : Digest Full Textmalea82No ratings yet

- Soneri Bank LTDDocument33 pagesSoneri Bank LTDishfaq_allahNo ratings yet

- Global Shell Games Book Launch PresentationDocument42 pagesGlobal Shell Games Book Launch PresentationGlobal Financial Integrity100% (2)

- Note-Ferrero India Pvt. Ltd.Document1 pageNote-Ferrero India Pvt. Ltd.Akhtar SiddiqueNo ratings yet

- Biscuits Market Trends: By: Moira HilliamDocument5 pagesBiscuits Market Trends: By: Moira HilliamAnurag IyerNo ratings yet

- Defensive Tactic M&ADocument4 pagesDefensive Tactic M&AMapleKoleksiNo ratings yet

- The Dassler Brothers: Made By: Prathmesh Kore Class: FD-7 (Mechanical)Document13 pagesThe Dassler Brothers: Made By: Prathmesh Kore Class: FD-7 (Mechanical)Prathmesh Kore100% (1)

- Emaar ScamDocument14 pagesEmaar ScamSidharth GuptaNo ratings yet

- CRG 660 Past Year Question CollectionsDocument5 pagesCRG 660 Past Year Question CollectionsZulaikha HananiNo ratings yet

- Introduction of Securities Commission MalaysiaDocument5 pagesIntroduction of Securities Commission MalaysiaGayathri KumarNo ratings yet

- Train TimingsDocument4 pagesTrain TimingsZim ShahNo ratings yet

- Garden City To GeneroCity Facilitated by United Way of BengaluruDocument4 pagesGarden City To GeneroCity Facilitated by United Way of BengaluruPRHUBNo ratings yet

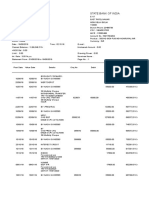

- Statement of Account: State Bank of IndiaDocument2 pagesStatement of Account: State Bank of Indiagaurav sharmaNo ratings yet

- CH 4 Non-Generic SwapsDocument31 pagesCH 4 Non-Generic SwapsEd ZNo ratings yet

- Barreto Et Al V La Previsora Filipina DigestDocument1 pageBarreto Et Al V La Previsora Filipina Digestᜇᜒᜀᜈ᜔ᜈ ᜋᜓᜈ᜔ᜆᜓᜌNo ratings yet

- SEBI ActDocument2 pagesSEBI ActPankaj2c100% (1)