You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- IntraDocument1 pageIntraHarshit AgarwalNo ratings yet

- 8e of The Millennium Development Goals, Acknowledge That The Availability and AffordabilityDocument5 pages8e of The Millennium Development Goals, Acknowledge That The Availability and AffordabilityHarshit AgarwalNo ratings yet

- Assignment On Indian Penal Court (Forgery)Document27 pagesAssignment On Indian Penal Court (Forgery)Harshit AgarwalNo ratings yet

- Dissertation MAINDocument126 pagesDissertation MAINHarshit AgarwalNo ratings yet

- Assignment No.16Document1 pageAssignment No.16Harshit AgarwalNo ratings yet

- Ipr HarDocument14 pagesIpr HarHarshit AgarwalNo ratings yet

- Faculty of Law, Jamia Millia Islamia Project Report On Hindu Joint Family 2018-2019Document17 pagesFaculty of Law, Jamia Millia Islamia Project Report On Hindu Joint Family 2018-2019Harshit AgarwalNo ratings yet

- Dying Declaration: Accused: Jaishree Anant Khandekar Vs State of Maharashtra On 23 March, 2009Document2 pagesDying Declaration: Accused: Jaishree Anant Khandekar Vs State of Maharashtra On 23 March, 2009Harshit AgarwalNo ratings yet

- Arbitral Award and Termination of Proceeding: Jamia Millia IslamiaDocument42 pagesArbitral Award and Termination of Proceeding: Jamia Millia IslamiaHarshit AgarwalNo ratings yet

- Index: S.No Topic Pg. NoDocument17 pagesIndex: S.No Topic Pg. NoHarshit AgarwalNo ratings yet

- Equal Pay For Equal Work Labour LawsDocument23 pagesEqual Pay For Equal Work Labour LawsHarshit AgarwalNo ratings yet

- Dubey EnvDocument14 pagesDubey EnvHarshit AgarwalNo ratings yet

- Legal AidDocument65 pagesLegal AidHarshit AgarwalNo ratings yet

- Tax LawDocument13 pagesTax LawHarshit AgarwalNo ratings yet

- Corporate PersonalityDocument21 pagesCorporate PersonalityHarshit AgarwalNo ratings yet

- Interpretation of StatutesDocument17 pagesInterpretation of StatutesHarshit Agarwal100% (1)

- Paper On Analysis of Refugee Law and Exigency of Domestic Refugee Laws in IndiaDocument7 pagesPaper On Analysis of Refugee Law and Exigency of Domestic Refugee Laws in IndiaHarshit AgarwalNo ratings yet

- Jamia Millia Islamia: Project On Salaries (Session-2018-2019)Document21 pagesJamia Millia Islamia: Project On Salaries (Session-2018-2019)Harshit AgarwalNo ratings yet

- Environmental EssayDocument8 pagesEnvironmental EssayHarshit AgarwalNo ratings yet

- NPA Final For SubmissionDocument37 pagesNPA Final For SubmissionHarshit AgarwalNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Gregory Feb 2020 Wells StatementDocument4 pagesGregory Feb 2020 Wells StatementYoooNo ratings yet

- Pci Dss Faqs: We Suggest That You Contact Your AcquirerDocument9 pagesPci Dss Faqs: We Suggest That You Contact Your Acquirerchaouch.najehNo ratings yet

- 1980Document1 page1980Kennedy KabukaNo ratings yet

- Tender Notice: Free Tenders For Almirahs, Antique Almirahs by Ministry of Home Affairs-7220024097Document3 pagesTender Notice: Free Tenders For Almirahs, Antique Almirahs by Ministry of Home Affairs-7220024097SanatNo ratings yet

- Oneblade Invoice PDFDocument1 pageOneblade Invoice PDFSuman DharaNo ratings yet

- Project On Value Added TaxDocument38 pagesProject On Value Added TaxKavita NadarNo ratings yet

- Chapter-1: Principles of Income-Tax Law Self Assessment QuestionsDocument46 pagesChapter-1: Principles of Income-Tax Law Self Assessment QuestionsJasmeet SinghNo ratings yet

- 031 Circular For FeesDocument26 pages031 Circular For FeesRupchandika DasNo ratings yet

- MG 3027 TAXATION - Week 10 Income From Self-Employment-Computation of IncomeDocument34 pagesMG 3027 TAXATION - Week 10 Income From Self-Employment-Computation of IncomeSyed SafdarNo ratings yet

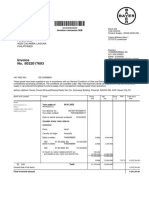

- Invoice No. 8032017603: Bayer Cropscience Inc. 3rd Flr. Bayer House PO Box 4600 4028 Calamba Laguna PhilippinesDocument2 pagesInvoice No. 8032017603: Bayer Cropscience Inc. 3rd Flr. Bayer House PO Box 4600 4028 Calamba Laguna PhilippinesGlezilda LoberianoNo ratings yet

- Revenue Memorandum Circular 36-2021 v2Document32 pagesRevenue Memorandum Circular 36-2021 v2lizzyNo ratings yet

- Use The Data For The Next Four QuestionsDocument8 pagesUse The Data For The Next Four QuestionsNo FaceNo ratings yet

- Deposit Confirmation/Renewal AdviceDocument1 pageDeposit Confirmation/Renewal AdviceRitu PatelNo ratings yet

- Corporation: Page 1 of 23Document21 pagesCorporation: Page 1 of 23Danica ConcepcionNo ratings yet

- TDS 23-24Document2 pagesTDS 23-24Taharat Ahmed ChowdhuryNo ratings yet

- Statement of Account: State Bank of IndiaDocument10 pagesStatement of Account: State Bank of IndiaSree ValsanNo ratings yet

- Bank Reconciliation StatementDocument20 pagesBank Reconciliation Statement1t4No ratings yet

- SWIFT MT103 202 Cover Payment Analysis - Part 3 - PaiementorDocument12 pagesSWIFT MT103 202 Cover Payment Analysis - Part 3 - Paiementorswift adminNo ratings yet

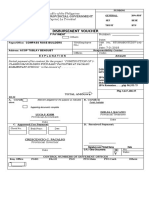

- Disbursement Voucher 2Document1 pageDisbursement Voucher 2janseninsta insta100% (1)

- Citizens Bank Statements Format PDFDocument3 pagesCitizens Bank Statements Format PDFErvin Scsad60% (5)

- WebconnectDocument1 pageWebconnectThottempudi VyshnaviNo ratings yet

- Wella Koleston 20220114.20Document4 pagesWella Koleston 20220114.20Be HeroSmartNo ratings yet

- Invoice #1 - 179-PNQDELQP114822102306294-oFXDocument1 pageInvoice #1 - 179-PNQDELQP114822102306294-oFXManish NairNo ratings yet

- PaySlips - June 2021 - May 2022Document12 pagesPaySlips - June 2021 - May 2022ahmed arifNo ratings yet

- Features & Functionality StatementDocument8 pagesFeatures & Functionality Statementvijay narwadeNo ratings yet

- IT CertificateDocument2 pagesIT CertificatePrashant TiwariNo ratings yet

- Swift MT700Document4 pagesSwift MT700FTU.CS2 Lê Phương ThảoNo ratings yet

- ST2023062601012473724Document1 pageST2023062601012473724alikhanmusa302No ratings yet

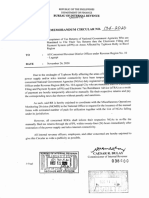

- RMC No. 134-2020Document1 pageRMC No. 134-2020nathalie velasquezNo ratings yet

- Basic Concepts of VATDocument20 pagesBasic Concepts of VATspchheda4996No ratings yet