You might also like

- Mini Case 3 Ppe-1Document5 pagesMini Case 3 Ppe-1ying huiNo ratings yet

- Tutorial 4 - Industrial Building AllowanceDocument3 pagesTutorial 4 - Industrial Building AllowanceChan YingNo ratings yet

- Mid-Term Test Tax517 June 2022Document8 pagesMid-Term Test Tax517 June 2022FeahRafeah KikiNo ratings yet

- Tax517 Test June 2022Document5 pagesTax517 Test June 2022Marlina RashidNo ratings yet

- Abfa1513 220518Document6 pagesAbfa1513 220518CRYSTAL NGNo ratings yet

- Cost of Land, Buildings, Equipment for Aliaga CorporationDocument4 pagesCost of Land, Buildings, Equipment for Aliaga CorporationLeisleiRagoNo ratings yet

- Mini-Case 1 Ppe AnswerDocument11 pagesMini-Case 1 Ppe Answeryu choong100% (2)

- Far270 February 22 FaDocument8 pagesFar270 February 22 FarumaisyaNo ratings yet

- June 2019 QDocument8 pagesJune 2019 Q2024786333No ratings yet

- Faculty - Accountancy - 2022 - Session 1 - Diploma - Far210Document8 pagesFaculty - Accountancy - 2022 - Session 1 - Diploma - Far210Bil hutNo ratings yet

- Far270 Q Feb2021 FaDocument9 pagesFar270 Q Feb2021 Fa2024786333No ratings yet

- Final Assessment Far210 Feb2021Document8 pagesFinal Assessment Far210 Feb2021Lampard AimanNo ratings yet

- Fin Accounting 3-A1-12-2022Document4 pagesFin Accounting 3-A1-12-2022Benjamin Banda100% (1)

- Tutorial Chapter 3 (IBA)Document4 pagesTutorial Chapter 3 (IBA)Nashrul IqmalNo ratings yet

- Acc May 2023-Past YearDocument7 pagesAcc May 2023-Past Yearcandywy0719No ratings yet

- Module 5 - PpsDocument4 pagesModule 5 - PpsMIGUEL JOSHUA VILLANUEVANo ratings yet

- Faculty Accountancy 2022 Session 1 - Degree Far510Document13 pagesFaculty Accountancy 2022 Session 1 - Degree Far510Wahida AmalinNo ratings yet

- MC 1-PPE (Students) - A202Document5 pagesMC 1-PPE (Students) - A202lim qsNo ratings yet

- Exercise - Mooc - 2022Document3 pagesExercise - Mooc - 2022ZULKHAIRY AFFANDY MOHD ZAKINo ratings yet

- Fe 202209 Dbca1113Document7 pagesFe 202209 Dbca1113Rabbi FazlaNo ratings yet

- Taxation II Tutorial 8: Calculating Industrial Building AllowanceDocument3 pagesTaxation II Tutorial 8: Calculating Industrial Building Allowanceathirah jamaludinNo ratings yet

- A231 - MC 3 PPE-StudentsDocument4 pagesA231 - MC 3 PPE-StudentsHafiza ZahidNo ratings yet

- TAX317 TEST Q Dec2021Document10 pagesTAX317 TEST Q Dec2021sharifah nurshahira sakinaNo ratings yet

- ACC2054 MTS Tutorial 6 QDocument2 pagesACC2054 MTS Tutorial 6 QTharvind KumarNo ratings yet

- Accounting for PPE AcquisitionsDocument3 pagesAccounting for PPE AcquisitionsAmirul Hakim Nor AzmanNo ratings yet

- 2020 Mar - 2020 July - QDocument11 pages2020 Mar - 2020 July - Qnur hazirahNo ratings yet

- Ctnov22 - Maf201 QDocument5 pagesCtnov22 - Maf201 QAinin SofiyaNo ratings yet

- CPA Paper 1 Financial Accounting 2Document9 pagesCPA Paper 1 Financial Accounting 2philipisingomaNo ratings yet

- RE Exam FA Sem I MFM MMM MHRDMDocument4 pagesRE Exam FA Sem I MFM MMM MHRDMPARAM CLOTHINGNo ratings yet

- PTX - Past Year Set ADocument8 pagesPTX - Past Year Set ANUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)No ratings yet

- Jan22 QQ PDFDocument5 pagesJan22 QQ PDFSYAZWINA SUHAILINo ratings yet

- CT May 2021Document5 pagesCT May 2021Star Wind Flower SunNo ratings yet

- Final Examination Personal TaxationDocument9 pagesFinal Examination Personal TaxationNUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)No ratings yet

- Q - Test Far270 Nov 2022 PDFDocument5 pagesQ - Test Far270 Nov 2022 PDFNUR QAMARINANo ratings yet

- Tutorial With Guided Explanation - MFRS116 StudentDocument19 pagesTutorial With Guided Explanation - MFRS116 StudentDont RushNo ratings yet

- FAR460 - Feb 2021 - Q - Set 1Document7 pagesFAR460 - Feb 2021 - Q - Set 1Ahmad Adlan Bin RosliNo ratings yet

- Far270 July2022Document8 pagesFar270 July2022Nur Fatin AmirahNo ratings yet

- Tax317 Ctmay2022Document10 pagesTax317 Ctmay2022sharifah nurshahira sakinaNo ratings yet

- Question Far270 Feb2021Document9 pagesQuestion Far270 Feb2021Nur Fatin AmirahNo ratings yet

- CT Maf201 May2022 - QDocument5 pagesCT Maf201 May2022 - Qdatu mohd aslamNo ratings yet

- Far270 - Q Test May 2023Document5 pagesFar270 - Q Test May 20232022896776No ratings yet

- Ppe ExerciseDocument8 pagesPpe ExerciseNajihah NordinNo ratings yet

- Property Plant and Equipment AuditDocument7 pagesProperty Plant and Equipment AuditKristine Jewel MirandaNo ratings yet

- M.B.A (2019 Pattern)Document291 pagesM.B.A (2019 Pattern)SurajNo ratings yet

- Assignment FarDocument5 pagesAssignment FarALIESYA FARHANA ALI HUSSAIN GHAZALINo ratings yet

- Fma PaperDocument2 pagesFma Paperfishy18No ratings yet

- SELF TEST 7 PROPERTY, PLANT AND EQUIPMENTDocument4 pagesSELF TEST 7 PROPERTY, PLANT AND EQUIPMENTJose Conrad Nupia BagonNo ratings yet

- Accounting for PPE, Inventory and ReceivablesDocument7 pagesAccounting for PPE, Inventory and Receivables谦谦君子No ratings yet

- Test 5Document4 pagesTest 5suzalaggarwalllNo ratings yet

- Universiti Teknologi Mara Final Examination: Confidential 1 AC/FEB 2022/FAR320Document7 pagesUniversiti Teknologi Mara Final Examination: Confidential 1 AC/FEB 2022/FAR3202021202082No ratings yet

- Dado BpsDocument6 pagesDado BpsmcannielNo ratings yet

- Construction FranchiseDocument7 pagesConstruction FranchisetheresaazuresNo ratings yet

- UntitledDocument3 pagesUntitledCarylChooNo ratings yet

- 185 Mid Term Exam 2020Document2 pages185 Mid Term Exam 2020khushali goharNo ratings yet

- Audit Problem UzDocument7 pagesAudit Problem UzRaies JumawanNo ratings yet

- Audit of PPE ExercisesDocument3 pagesAudit of PPE ExercisesMARCUAP Flora Mel Joy H.No ratings yet

- SME Investment Property Carrying AmountDocument9 pagesSME Investment Property Carrying AmountHarvey Dienne QuiambaoNo ratings yet

- MC 3 - PPE - A201 - StudentDocument4 pagesMC 3 - PPE - A201 - Studentlim qsNo ratings yet

- Bbfa1103 Assigment Question 2023Document13 pagesBbfa1103 Assigment Question 2023Bdq ArrogantNo ratings yet

- Managing Successful Projects with PRINCE2 2009 EditionFrom EverandManaging Successful Projects with PRINCE2 2009 EditionRating: 4 out of 5 stars4/5 (3)

- Slideshare Typesofstrategies 130903042429 Phpapp01Document43 pagesSlideshare Typesofstrategies 130903042429 Phpapp01Zati TyNo ratings yet

- Advanced Financial Accounting and Reporting: Appendix ADocument5 pagesAdvanced Financial Accounting and Reporting: Appendix AZati TyNo ratings yet

- Default DarkDocument2 pagesDefault DarkMir SylNo ratings yet

- Notes EvidenceDocument3 pagesNotes EvidenceZati TyNo ratings yet

- Cover AssignmentDocument2 pagesCover AssignmentZati TyNo ratings yet

- AIS Development StrategiesDocument14 pagesAIS Development StrategiesHabtamu Hailemariam AsfawNo ratings yet

- Financial Accounting TheoryDocument10 pagesFinancial Accounting TheoryMrZiggyGreenNo ratings yet

- Case Historical CostDocument23 pagesCase Historical CostZati TyNo ratings yet

- 013255271X - PPT - 20 GEDocument18 pages013255271X - PPT - 20 GEZati TyNo ratings yet

- Maqasid Al Shariah in Wealth ManagementDocument15 pagesMaqasid Al Shariah in Wealth ManagementZati TyNo ratings yet

- Introduction To Systems Development and Systems AnalysisDocument16 pagesIntroduction To Systems Development and Systems AnalysisHabtamu Hailemariam AsfawNo ratings yet

- 013255271X - PPT - 03 GEDocument19 pages013255271X - PPT - 03 GEZati TyNo ratings yet

- Advance Audit NotesDocument152 pagesAdvance Audit NotesZati TyNo ratings yet

- LegalDocument21 pagesLegalZati TyNo ratings yet

- AnswerDocument4 pagesAnswerZati TyNo ratings yet

- AnswerDocument3 pagesAnswerZati TyNo ratings yet

- Audit in Computerised EnvironmentDocument8 pagesAudit in Computerised EnvironmentZati TyNo ratings yet

- Resident Status AnswerDocument8 pagesResident Status AnswerZati TyNo ratings yet

- Case Study - External Environment - NestleDocument2 pagesCase Study - External Environment - NestlebgbhattacharyaNo ratings yet

- Four Big Challenges Facing Internal AuditDocument6 pagesFour Big Challenges Facing Internal AuditZati TyNo ratings yet

- Profession and Its Challenge: AuditDocument1 pageProfession and Its Challenge: AuditZati TyNo ratings yet

- The Future of Audit: Reporting by The Accountants Today Editorial TeamDocument6 pagesThe Future of Audit: Reporting by The Accountants Today Editorial TeamZati TyNo ratings yet

- A Guide To UBS TaskDocument85 pagesA Guide To UBS TaskZati TyNo ratings yet

- 2016 Bank MuamalatDocument383 pages2016 Bank MuamalatZati TyNo ratings yet

- Appeal Tax Procedure (Malaysia)Document2 pagesAppeal Tax Procedure (Malaysia)Zati TyNo ratings yet

- A Guide To UBS Task - FlipHTML5 PDFDocument85 pagesA Guide To UBS Task - FlipHTML5 PDFZati TyNo ratings yet

- Self Assessment SystemDocument1 pageSelf Assessment SystemZati TyNo ratings yet

- Appeal Tax Procedure (Malaysia)Document2 pagesAppeal Tax Procedure (Malaysia)Zati TyNo ratings yet

- Why It Is Necessary To Have An Islamic Financial SystemDocument4 pagesWhy It Is Necessary To Have An Islamic Financial SystemZati TyNo ratings yet

- Credit Card Processing System UML Use Case DiagramDocument2 pagesCredit Card Processing System UML Use Case DiagramTushar TariNo ratings yet

- Equinox Products Inc. fiscal year transactionsDocument1 pageEquinox Products Inc. fiscal year transactionsVarun SharmaNo ratings yet

- Phil Guaranty Co vs CIR examines foreign reinsurance premiumsDocument10 pagesPhil Guaranty Co vs CIR examines foreign reinsurance premiumsGwen Alistaer CanaleNo ratings yet

- Firm Profile CompressedDocument9 pagesFirm Profile CompressedharshNo ratings yet

- CRM Services India Private Limited: Earnings DeductionsDocument1 pageCRM Services India Private Limited: Earnings DeductionsInnama SayedNo ratings yet

- CPA Firm TransactionsDocument4 pagesCPA Firm TransactionsBigAsianPapiNo ratings yet

- DATEV Account Chart: Standard Chart of Accounts SKR 04 Valid For 2015Document29 pagesDATEV Account Chart: Standard Chart of Accounts SKR 04 Valid For 2015Elizabeth Sánchez LeónNo ratings yet

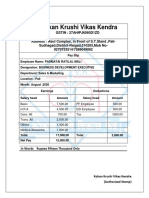

- Kokan Krushi Vikas Kendra pay slips August to October 2020Document3 pagesKokan Krushi Vikas Kendra pay slips August to October 2020DevenNo ratings yet

- 21-22 - P & L and BALANCE SHEETDocument2 pages21-22 - P & L and BALANCE SHEETSidvik InfotechNo ratings yet

- Tax Invoice: Billing Address Installation Address Invoice DetailsDocument1 pageTax Invoice: Billing Address Installation Address Invoice DetailsprofbhimashankarsNo ratings yet

- IDBI BANK ZOMATO OFFERDocument1 pageIDBI BANK ZOMATO OFFERVipin SachdevaNo ratings yet

- PAPA Session 5Document3 pagesPAPA Session 5Thomas KariukiNo ratings yet

- Enjoy Connection Globally.: Tax Invoice/ Tax Credit NoteDocument39 pagesEnjoy Connection Globally.: Tax Invoice/ Tax Credit NoteahsanukkakarNo ratings yet

- E TicketsDocument4 pagesE TicketsPayroll TeamNo ratings yet

- Earnings Per ShareDocument3 pagesEarnings Per ShareYeshua DeluxiusNo ratings yet

- Book e-ticket for travel from Chennai to BengaluruDocument1 pageBook e-ticket for travel from Chennai to BengaluruNitya TadinadaNo ratings yet

- Samrat PDFDocument2 pagesSamrat PDFCHIRAYU PHARMACEUTICALSNo ratings yet

- LNG Competitors Wages - Aug 2015Document11 pagesLNG Competitors Wages - Aug 2015OctavianNo ratings yet

- LT BILL 46429091009 Dec22Document2 pagesLT BILL 46429091009 Dec22Deepak JhaNo ratings yet

- Income Tax-100 QuestionsDocument5 pagesIncome Tax-100 QuestionsChez Nicole LimpinNo ratings yet

- Online Payment - Passport SevaDocument2 pagesOnline Payment - Passport SevaAbdul Hakeem Semar KamaluddinNo ratings yet

- Module10 Business Transactions and AnalysisDocument29 pagesModule10 Business Transactions and AnalysisAlyssa Nikki VersozaNo ratings yet

- POS Class Diagram PDFDocument1 pagePOS Class Diagram PDFSaad HassanNo ratings yet

- OpTransactionHistory21 01 2016Document3 pagesOpTransactionHistory21 01 2016venkatesanjsNo ratings yet

- T D S Certificate Last Updated On 09 Jun 2018, BPCL AAATW0620Q - Q4 - 2018 19Document2 pagesT D S Certificate Last Updated On 09 Jun 2018, BPCL AAATW0620Q - Q4 - 2018 19MinatiBindhaniNo ratings yet

- July292016 FINAL 4thedition KratzkeNOcover Lulu PDFDocument602 pagesJuly292016 FINAL 4thedition KratzkeNOcover Lulu PDFJohn Clifford EranaNo ratings yet

- Chapter 34Document10 pagesChapter 34Kaila Mae Tan DuNo ratings yet

- IDFCFIRSTBankstatement 10023948749Document8 pagesIDFCFIRSTBankstatement 10023948749Praveen SainiNo ratings yet

- Electricity BillDocument1 pageElectricity BillKaranKr67% (3)

- Purchase Unit 116 Tierra Verde TownhomeDocument2 pagesPurchase Unit 116 Tierra Verde Townhomeshrine obenietaNo ratings yet