You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5811)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Federal ReserveDocument315 pagesFederal Reservejuliusevola1100% (2)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- AccountingDocument62 pagesAccountingRashid W QureshiNo ratings yet

- Oracle ASCP Success StoriesDocument31 pagesOracle ASCP Success Storiesboddu2450% (2)

- DocxDocument15 pagesDocxmarieieiemNo ratings yet

- Full Assignment Tax RPGTDocument19 pagesFull Assignment Tax RPGTVasant SriudomNo ratings yet

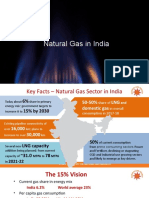

- Natural Gas in IndiaDocument19 pagesNatural Gas in IndiaAnkit PandeyNo ratings yet

- K Means 1 PDFDocument4 pagesK Means 1 PDFM A DiptoNo ratings yet

- Rao EHS SurveyDocument19 pagesRao EHS SurveyM A DiptoNo ratings yet

- A Dynamic Trust Model Based On Naive Bayes Classifier For Ubiquitous EnvironmentsDocument10 pagesA Dynamic Trust Model Based On Naive Bayes Classifier For Ubiquitous EnvironmentsM A DiptoNo ratings yet

- Machine Learning & Data MiningDocument108 pagesMachine Learning & Data MiningM A DiptoNo ratings yet

- Zenia 2016Document25 pagesZenia 2016M A DiptoNo ratings yet

- Physics QsDocument2 pagesPhysics QsM A DiptoNo ratings yet

- Hypothesis Text ExDocument11 pagesHypothesis Text ExM A DiptoNo ratings yet

- Subjective Logic: Audun JøsangDocument69 pagesSubjective Logic: Audun JøsangM A DiptoNo ratings yet

- 2 - SpineDocument1 page2 - SpineM A DiptoNo ratings yet

- LDPCDocument5 pagesLDPCM A DiptoNo ratings yet

- Django 1Document5 pagesDjango 1M A DiptoNo ratings yet

- 21 Ekim-11 KasımDocument32 pages21 Ekim-11 KasımElif KAVASNo ratings yet

- Sharol Isneidy Velasco: Logistics TechnologistDocument3 pagesSharol Isneidy Velasco: Logistics TechnologistSHAROL ISNEIDY VELASCO BAYONANo ratings yet

- Year Ahead Asia 2011Document92 pagesYear Ahead Asia 2011rezurektNo ratings yet

- EPIC Systems: Best Quality Smart Digital Door LockDocument16 pagesEPIC Systems: Best Quality Smart Digital Door LockHuong Quynh NguyenNo ratings yet

- Gmail - Your Air France Booking Is Pending Payment 2Document5 pagesGmail - Your Air France Booking Is Pending Payment 2shawn alexNo ratings yet

- The International Journal of Human Resource ManagementDocument25 pagesThe International Journal of Human Resource Managementkashif salmanNo ratings yet

- Project Report Shopper StopDocument62 pagesProject Report Shopper Stopjyot singh khannaNo ratings yet

- Section OneDocument5 pagesSection OneYemi Ade100% (1)

- A Study On Focussing Retaining The Employees in Big Bazaar Private LimitedDocument11 pagesA Study On Focussing Retaining The Employees in Big Bazaar Private LimitedGauthem RajNo ratings yet

- 2021 OFW GIS With Logo Orig 1Document2 pages2021 OFW GIS With Logo Orig 1Alexis OrganisNo ratings yet

- Class 12 Business Studies Chapter 12 MCQ'sDocument41 pagesClass 12 Business Studies Chapter 12 MCQ'sPUTTU GURU PRASAD SENGUNTHA MUDALIARNo ratings yet

- Credit Rating: Need, Process and LimitationsDocument24 pagesCredit Rating: Need, Process and LimitationsRupam Aryan BorahNo ratings yet

- Pharmaceutical MarketingDocument2 pagesPharmaceutical MarketingNandha KumarNo ratings yet

- Mutual Fund ProjectDocument45 pagesMutual Fund ProjectRaghavendra WaghmareNo ratings yet

- Section A-MCQ (15 Marks) : Good LuckDocument3 pagesSection A-MCQ (15 Marks) : Good Luckhuzaifa anwarNo ratings yet

- Statergic Human Resource ManagementDocument249 pagesStatergic Human Resource Managementnaveenkumar193100% (2)

- Variations and Change Orders On Construction Projects: ForumDocument8 pagesVariations and Change Orders On Construction Projects: ForumAizel JoannaNo ratings yet

- AFM Capital Structure Cp5Document61 pagesAFM Capital Structure Cp5drmsellan7No ratings yet

- A Study On Effectiveness of Training and Development Programs Adopted by KPCL, BangaloreDocument7 pagesA Study On Effectiveness of Training and Development Programs Adopted by KPCL, BangaloreShaheda ShariffNo ratings yet

- Nguyen-Ngoc-Quynh-Nhung - Apply For An AccountantDocument8 pagesNguyen-Ngoc-Quynh-Nhung - Apply For An AccountantNguyen RyanNo ratings yet

- Finstreet - Finance Committee, Kjsimsr: Where Knowledge & Learning Are Key To SuccessDocument7 pagesFinstreet - Finance Committee, Kjsimsr: Where Knowledge & Learning Are Key To SuccessShalu PurswaniNo ratings yet

- E-Business Unit 3Document5 pagesE-Business Unit 3Danny SathishNo ratings yet

- Leading and Managing ChangeDocument15 pagesLeading and Managing ChangeazmiikptNo ratings yet

- Detailed Training Program - HasibDocument10 pagesDetailed Training Program - HasibKaziRashidulAzamNo ratings yet