You might also like

- 214-Kotak Bank-Non Performing Assets at Kotak Mahindra BankDocument70 pages214-Kotak Bank-Non Performing Assets at Kotak Mahindra BankPeacock Live ProjectsNo ratings yet

- Posted: Sat Feb 03, 2007 1:58 PM Post Subject: Causes For Non-Performing Assets in Public Sector BanksDocument13 pagesPosted: Sat Feb 03, 2007 1:58 PM Post Subject: Causes For Non-Performing Assets in Public Sector BanksSimer KaurNo ratings yet

- Icici Bank ProjectDocument82 pagesIcici Bank ProjectiamdarshandNo ratings yet

- A Comparative Study of Non-Performing Assets of Canara Bank & Icici BankDocument42 pagesA Comparative Study of Non-Performing Assets of Canara Bank & Icici BankASWATHYNo ratings yet

- CERTIFICATEDocument31 pagesCERTIFICATEShanawaz ArifNo ratings yet

- Non Performing Assets 111111Document23 pagesNon Performing Assets 111111renika50% (2)

- A Case Study On Npa 2.o PDFDocument43 pagesA Case Study On Npa 2.o PDFAditya RoyNo ratings yet

- Research Paper On Npa in BanksDocument8 pagesResearch Paper On Npa in Banksz0pilazes0m3100% (1)

- Non Performing Assets (Npas) : A Study of Punjab National BankDocument11 pagesNon Performing Assets (Npas) : A Study of Punjab National BankKritiNo ratings yet

- Impact of Non-Performing Assets On Banking Industry: The Indian PerspectiveDocument8 pagesImpact of Non-Performing Assets On Banking Industry: The Indian Perspectiveshubham kumarNo ratings yet

- Impact of NonDocument30 pagesImpact of NonAmardeep SinghNo ratings yet

- Research Paper 2Document7 pagesResearch Paper 2Pooja AgarwalNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Shri Vaishnav Institute of Management, Indore (M.P.)Document14 pagesShri Vaishnav Institute of Management, Indore (M.P.)Vikas_2coolNo ratings yet

- Equity: Read More: Under Creative Commons LicenseDocument7 pagesEquity: Read More: Under Creative Commons Licenseyogallaly_jNo ratings yet

- Subject: Banking Law Non Performing Assets Management: Project TopicDocument36 pagesSubject: Banking Law Non Performing Assets Management: Project TopicAshutoshKumarNo ratings yet

- Non Performing Assets in Allahabad BankDocument69 pagesNon Performing Assets in Allahabad BankGotham RamNo ratings yet

- 121, Saurabh Bhosale, NPADocument67 pages121, Saurabh Bhosale, NPASaurabh BhosaleNo ratings yet

- Tabarsum NON PERFORMING ASSETS AXIS BANKDocument73 pagesTabarsum NON PERFORMING ASSETS AXIS BANKSagar Paul'g100% (4)

- Private Banks Rein in NPAsDocument8 pagesPrivate Banks Rein in NPAsanayatbakshNo ratings yet

- Uti BankDocument86 pagesUti BankMohit kolliNo ratings yet

- B 16 Corporate FinanceDocument17 pagesB 16 Corporate FinanceDhrumil ShahNo ratings yet

- Study of NPA in IndiaDocument43 pagesStudy of NPA in IndiaKartik UdayarNo ratings yet

- A Study On NPA of Public Sector Banks in India: AssignmentDocument10 pagesA Study On NPA of Public Sector Banks in India: AssignmentSurya BalaNo ratings yet

- Blackbook Project On Indian Banking Sector 2Document119 pagesBlackbook Project On Indian Banking Sector 2anilmourya5No ratings yet

- Black Book Fdocuments - in - Blackbook-Project-On-Indian-Banking-Sector-2Document119 pagesBlack Book Fdocuments - in - Blackbook-Project-On-Indian-Banking-Sector-2SamNo ratings yet

- 20q61e00c3 - Non Performing Assets - Icici BankDocument54 pages20q61e00c3 - Non Performing Assets - Icici BankRajesh BathulaNo ratings yet

- Tools and Techniques of NPADocument9 pagesTools and Techniques of NPAPruthviraj RathoreNo ratings yet

- Non Performing Assets and Profitability of Scheduled Commercial BanksDocument11 pagesNon Performing Assets and Profitability of Scheduled Commercial Banksadharav malikNo ratings yet

- Non Performing Assets and Profitability of Scheduled Commercial BanksDocument11 pagesNon Performing Assets and Profitability of Scheduled Commercial Banksneekuj malikNo ratings yet

- Ijrim Volume 2, Issue 11 (November 2012) (ISSN 2231-4334) Management of Non Performing Assets (Npas) in Public Sector BanksDocument9 pagesIjrim Volume 2, Issue 11 (November 2012) (ISSN 2231-4334) Management of Non Performing Assets (Npas) in Public Sector BanksmithiliNo ratings yet

- Literature Review On Non Performing AssetsDocument7 pagesLiterature Review On Non Performing Assetsibcaahsif100% (1)

- Recent Trend of NPL in Banking SectorDocument14 pagesRecent Trend of NPL in Banking SectorAbid HasanNo ratings yet

- Sapana H CDocument40 pagesSapana H CPraveen RathodNo ratings yet

- A STUDY ON LOAN MANAGEMENT OF NEPAL BANK LIMITED AND AGRICULTURAL DEVELOPMENT BANK LIMITED1stDocument7 pagesA STUDY ON LOAN MANAGEMENT OF NEPAL BANK LIMITED AND AGRICULTURAL DEVELOPMENT BANK LIMITED1stOmisha KhatiwadaNo ratings yet

- Banking Law ProjectDocument9 pagesBanking Law ProjectPrakhya ShahNo ratings yet

- Sip Report On SbiDocument46 pagesSip Report On SbiRashmi RanjanNo ratings yet

- Causes of NPADocument7 pagesCauses of NPAsggovardhan0% (1)

- A Study of Non Performing Asset Management of Bank of IndiaDocument54 pagesA Study of Non Performing Asset Management of Bank of IndiaMeenakshi Sharma67% (3)

- Non - Performing Assets - PublicationDocument12 pagesNon - Performing Assets - PublicationChandra SekarNo ratings yet

- Research Paper On Npa of BanksDocument4 pagesResearch Paper On Npa of Banksiqfjzqulg100% (1)

- NPA of Indian BanksDocument27 pagesNPA of Indian BanksShristi GuptaNo ratings yet

- Analysis of NPA ManagementDocument109 pagesAnalysis of NPA ManagementmithiliNo ratings yet

- May 2012 Govind SinghDocument18 pagesMay 2012 Govind SinghWilliam WrightNo ratings yet

- Non-Performing Assets of Commercial Banks in India: 1 AbsractDocument8 pagesNon-Performing Assets of Commercial Banks in India: 1 AbsractSanya AroraNo ratings yet

- 1 Background To The StudyDocument4 pages1 Background To The StudyNagabhushanaNo ratings yet

- Final Report On Study of Npa by Pankaj BohraDocument101 pagesFinal Report On Study of Npa by Pankaj Bohrapankaj bohraNo ratings yet

- SYNOPSIS NpaDocument9 pagesSYNOPSIS Npamonikaaroramca100% (1)

- Indian Banking SectorDocument7 pagesIndian Banking Sectordebaditya_mohantiNo ratings yet

- Non Performing AssetsDocument24 pagesNon Performing AssetsAmarjeet DhobiNo ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Public Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesFrom EverandPublic Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesNo ratings yet

- Emerging Issues in Finance Sector Inclusion, Deepening, and Development in the People's Republic of ChinaFrom EverandEmerging Issues in Finance Sector Inclusion, Deepening, and Development in the People's Republic of ChinaNo ratings yet

- EIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptFrom EverandEIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptNo ratings yet

- Draft of Noc To SocietyDocument2 pagesDraft of Noc To SocietyAmeya Bapat0% (1)

- Acknowledgement Receipt: Rendered, Rental Payments, Partial Payments or For Any Other Payment That Needs AcknowledgementDocument1 pageAcknowledgement Receipt: Rendered, Rental Payments, Partial Payments or For Any Other Payment That Needs AcknowledgementMarx AndreiOscar Villanueva YaunNo ratings yet

- Civil Suit Sneh LataDocument14 pagesCivil Suit Sneh LataAbhijit TripathiNo ratings yet

- Features of 80C:-: Note - 1 - Gross Qualifying Amount:-Aggregate of The FollowingDocument6 pagesFeatures of 80C:-: Note - 1 - Gross Qualifying Amount:-Aggregate of The FollowingJamsheer BslNo ratings yet

- The Sales of Goods Act, 1930Document76 pagesThe Sales of Goods Act, 1930goel76vishalNo ratings yet

- Developing Business Proposals For Aquaculture LoanDocument6 pagesDeveloping Business Proposals For Aquaculture Loang4nz0No ratings yet

- Project On Housing LoanDocument119 pagesProject On Housing Loanrajjinonu53% (19)

- Process Flow For Watani RefinanceDocument1 pageProcess Flow For Watani RefinancejosephNo ratings yet

- ARMANDO GEAGONIA v. COURT OF APPEALS Et Al.Document3 pagesARMANDO GEAGONIA v. COURT OF APPEALS Et Al.Karl CabarlesNo ratings yet

- Statutory Bank Audits Practical Aspect Prepared by - Bhargav NathwaniDocument20 pagesStatutory Bank Audits Practical Aspect Prepared by - Bhargav NathwaniAkash SingrodiaNo ratings yet

- Citigroup Open Bank Assistance Unredacted FDIC Minutes From 23 Nov 2008 (Lawsuit #2)Document16 pagesCitigroup Open Bank Assistance Unredacted FDIC Minutes From 23 Nov 2008 (Lawsuit #2)Vern McKinleyNo ratings yet

- CompDocument40 pagesCompArun KCNo ratings yet

- Rayo vs. Metropolitan Bank Inc.Document6 pagesRayo vs. Metropolitan Bank Inc.Daniel Dela CruzNo ratings yet

- Jet Airways Case StudyDocument5 pagesJet Airways Case StudyVaibhav golaniNo ratings yet

- Barayoga Vs APTDocument2 pagesBarayoga Vs APTNiki Dela CruzNo ratings yet

- Separation Agreement Checklist MASSDocument4 pagesSeparation Agreement Checklist MASSbanker135No ratings yet

- Letter of Guarantee by CorporateDocument6 pagesLetter of Guarantee by CorporateTira MagdNo ratings yet

- Promissory Note With Chattel MortgageDocument4 pagesPromissory Note With Chattel MortgageLien Patrick100% (1)

- The Chits Funds ActDocument40 pagesThe Chits Funds Actdesikudi9000No ratings yet

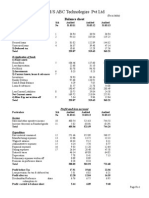

- Balance Sheet of M/S ABC Technologies PVT LTDDocument3 pagesBalance Sheet of M/S ABC Technologies PVT LTDSmitha RajNo ratings yet

- Torres V Court of Appeals (GR L-63046 June 21 1990)Document2 pagesTorres V Court of Appeals (GR L-63046 June 21 1990)Enma KozatoNo ratings yet

- Checklist of Requirements For Issuance of Poea LicenseDocument4 pagesChecklist of Requirements For Issuance of Poea Licensesbagsic100% (2)

- BUSANA1 Chapter 4: Sinking FundDocument17 pagesBUSANA1 Chapter 4: Sinking Fund7 bitNo ratings yet

- Schedule of Assets and DebtsDocument4 pagesSchedule of Assets and DebtsRenée ReimiNo ratings yet

- Essential Elements: The Essential Elements of A Lease Are As FollowsDocument8 pagesEssential Elements: The Essential Elements of A Lease Are As FollowssssNo ratings yet

- Introduction To Risk Management and MCQ L 1Document15 pagesIntroduction To Risk Management and MCQ L 1Ayaz MeerNo ratings yet

- Stamp Duty Circular-Ver 9Document12 pagesStamp Duty Circular-Ver 9Mrigesh KejriwalNo ratings yet

- Chap 3 Fixed Income SecuritiesDocument45 pagesChap 3 Fixed Income SecuritiesHABTAMU TULU0% (1)

- Final - SFM - Money Market PDFDocument37 pagesFinal - SFM - Money Market PDFMarikrishna Chandran CANo ratings yet