You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Truffle MarketDocument14 pagesTruffle MarketAnonymous zL3aOc9No ratings yet

- Advanced Accounting Baker Test Bank - Chap011Document67 pagesAdvanced Accounting Baker Test Bank - Chap011donkazotey100% (7)

- A Study On The Impact of Volatility in Exchange Rate of Indian Rupee Versus US Dollar On Indian Capital MarketDocument17 pagesA Study On The Impact of Volatility in Exchange Rate of Indian Rupee Versus US Dollar On Indian Capital MarketsaravanakrisNo ratings yet

- An Empirical Analysis of Foreign Institutional Investments in Equity & Debt Market in IndiaDocument12 pagesAn Empirical Analysis of Foreign Institutional Investments in Equity & Debt Market in IndiasaravanakrisNo ratings yet

- A Study of The Impact of FII On The Sectoral Market IndicesDocument6 pagesA Study of The Impact of FII On The Sectoral Market IndicessaravanakrisNo ratings yet

- Adaptive Market Hypothesis Evidence From Indian Bond MarketDocument14 pagesAdaptive Market Hypothesis Evidence From Indian Bond MarketsaravanakrisNo ratings yet

- A Study of Lead-Lag Relation Between FIIs Herding and Stock Market Returns in Emerging Economies Evidence From IndiaDocument15 pagesA Study of Lead-Lag Relation Between FIIs Herding and Stock Market Returns in Emerging Economies Evidence From IndiasaravanakrisNo ratings yet

- Ceramic Tiles - Official Gazette 27 (10234)Document16 pagesCeramic Tiles - Official Gazette 27 (10234)NajeebNo ratings yet

- 115 - Yam v. CA DigestDocument2 pages115 - Yam v. CA DigestStephieIgnacioNo ratings yet

- ASEAN Association of Southeast Asian NationsDocument3 pagesASEAN Association of Southeast Asian NationsnicolepekkNo ratings yet

- The Manufacturing Sector in Malaysia PDFDocument17 pagesThe Manufacturing Sector in Malaysia PDFNazirah Abdul RohmanNo ratings yet

- CET Analysis of SamsungDocument9 pagesCET Analysis of SamsungMj PayalNo ratings yet

- Africa World AirlinesDocument1 pageAfrica World AirlinesKwame YeboahNo ratings yet

- India Road Network The Second Largest Road NetworkDocument19 pagesIndia Road Network The Second Largest Road NetworkKushal rajNo ratings yet

- 2013b Blanchard Latvia CrisisDocument64 pages2013b Blanchard Latvia CrisisrajaytNo ratings yet

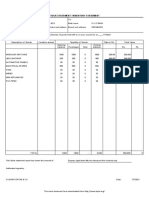

- Stock Statement Format For Bank LoanDocument1 pageStock Statement Format For Bank Loanpsycho Neha40% (5)

- List of The Top 10 Leather Manufacturers in BangladeshDocument4 pagesList of The Top 10 Leather Manufacturers in BangladeshNasim HasanNo ratings yet

- PHM PCH EnglishDocument9 pagesPHM PCH Englishlalit823187No ratings yet

- The Entry and Exit of Political Economy ArrangementsDocument13 pagesThe Entry and Exit of Political Economy ArrangementsMARIANNE JANE ZARANo ratings yet

- Effects of Labor Standard Law in Regularization of EmployeesDocument4 pagesEffects of Labor Standard Law in Regularization of EmployeesNicole Ann MagistradoNo ratings yet

- Wilson Go V. Estate of Late Felisa Tamio de Buenaventura GR No. 211972, Jul 22, 2015Document2 pagesWilson Go V. Estate of Late Felisa Tamio de Buenaventura GR No. 211972, Jul 22, 2015Alvin Ryan KipliNo ratings yet

- Astronacci Notes - 1 AnomaliesDocument2 pagesAstronacci Notes - 1 AnomaliesSatrio SuryadiNo ratings yet

- Invitation To Bid: Dvertisement ArticularsDocument2 pagesInvitation To Bid: Dvertisement ArticularsBDO3 3J SolutionsNo ratings yet

- Steeple AnalysisDocument2 pagesSteeple AnalysisSamrahNo ratings yet

- WEG India Staff Contact Numbers PDFDocument10 pagesWEG India Staff Contact Numbers PDFM.DINESH KUMARNo ratings yet

- Name: Elma P. Rejano Prof: Mr. Rene Boy BacayDocument5 pagesName: Elma P. Rejano Prof: Mr. Rene Boy BacayElma RejanoNo ratings yet

- Economy of BangladeshDocument22 pagesEconomy of BangladeshRobert DunnNo ratings yet

- SsDocument8 pagesSsAnonymous cPS4htyNo ratings yet

- Price and Output Determination Under Monopoly MarketDocument16 pagesPrice and Output Determination Under Monopoly MarketManak Ram SingariyaNo ratings yet

- GSTR1 Stupl 08ABFCS1229J1Z9 November 2021 BusyDocument92 pagesGSTR1 Stupl 08ABFCS1229J1Z9 November 2021 BusyYathesht JainNo ratings yet

- ICSB Mexico MSMEs Outlook Ricardo D. Alvarez v.2.Document4 pagesICSB Mexico MSMEs Outlook Ricardo D. Alvarez v.2.Ricardo ALvarezNo ratings yet

- Bbob Current AffairsDocument28 pagesBbob Current AffairsGangwar AnkitNo ratings yet

- Eurocontrol European Aviation Overview 20230602Document20 pagesEurocontrol European Aviation Overview 20230602Neo PilNo ratings yet

- The Rite-The Making of A Modern Exorcist - Matt BaglioDocument130 pagesThe Rite-The Making of A Modern Exorcist - Matt BaglioFrancisco J. Salinas B.No ratings yet

- Joint Stock CompanyDocument2 pagesJoint Stock CompanybijuNo ratings yet