You might also like

- ISO 9001:2008 CERTIFIED Public Notice Verification of Taxpayers' RecordsDocument2 pagesISO 9001:2008 CERTIFIED Public Notice Verification of Taxpayers' RecordsAnonymous FnM14a0No ratings yet

- NBR Tin Certificate 468107475375Document1 pageNBR Tin Certificate 468107475375Wonder CatNo ratings yet

- TIN Application - NBR TIN RegistrationDocument2 pagesTIN Application - NBR TIN RegistrationFerdous HasanNo ratings yet

- NBR Tin Certificate 367005151131 PDFDocument1 pageNBR Tin Certificate 367005151131 PDFTahsan AhmedNo ratings yet

- Sample Intl Bank StatementDocument1 pageSample Intl Bank Statementapi-3834921100% (1)

- NBR Tin Certificate 350467356871Document1 pageNBR Tin Certificate 350467356871Faisal Anwar100% (1)

- NBR Tin Certificate 178747888345Document1 pageNBR Tin Certificate 178747888345Habibur RahmanNo ratings yet

- TIN Certificate PDFDocument1 pageTIN Certificate PDFJust BangladeshNo ratings yet

- E-TinDocument1 pageE-TinRezaul Alam100% (1)

- NBR Tin Certificate 127597607663Document1 pageNBR Tin Certificate 127597607663MD. SaketNo ratings yet

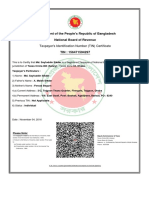

- Government of The People's Republic of Bangladesh National Board of RevenueDocument1 pageGovernment of The People's Republic of Bangladesh National Board of RevenuexgyhhbNo ratings yet

- NBR Tin Certificate 868740934640 PDFDocument1 pageNBR Tin Certificate 868740934640 PDFডাঃ রাজিব রোহানNo ratings yet

- NBR Tin Certificate 595255423005 PDFDocument1 pageNBR Tin Certificate 595255423005 PDFAlaul KarimNo ratings yet

- NBR Tin Certificate 763444639565 PDFDocument1 pageNBR Tin Certificate 763444639565 PDFGame army shakilNo ratings yet

- Brief Resume of Tofayel Hossain BasuniaDocument5 pagesBrief Resume of Tofayel Hossain BasuniaMorshedDenarAlamMannaNo ratings yet

- NBR Tin Certificate 370422673914Document1 pageNBR Tin Certificate 370422673914MorshedDenarAlamMannaNo ratings yet

- DBBL 7psDocument15 pagesDBBL 7psMohammad Zahurul Hoque0% (1)

- NBR Tin Certificate 214981417638Document1 pageNBR Tin Certificate 214981417638MD. Saket0% (1)

- NBR Tin Certificate 266950216893 PDFDocument1 pageNBR Tin Certificate 266950216893 PDFFaruk HossainNo ratings yet

- NBR Tin Certificate 680851799008Document1 pageNBR Tin Certificate 680851799008Khaza MahbubNo ratings yet

- NBR Tin Certificate 897754123434Document1 pageNBR Tin Certificate 897754123434Md MasumNo ratings yet

- NBR Tin Certificate 495693316003Document1 pageNBR Tin Certificate 495693316003Nousen Tara100% (1)

- FDA Certificate FileDocument3 pagesFDA Certificate FileBilgi KurumsalNo ratings yet

- NBR Tin Certificate 622197722607Document1 pageNBR Tin Certificate 622197722607Xahangir AlamNo ratings yet

- Bank Statement (Nisar Ahmad)Document1 pageBank Statement (Nisar Ahmad)hamid mahmoodNo ratings yet

- TIN SampleDocument2 pagesTIN SampleAnonymous P78WJo8LPBNo ratings yet

- TIN SayfDocument1 pageTIN SayfMd. Riazur RahmanNo ratings yet

- Application Form For MSB Licence - Eng - 22032013Document8 pagesApplication Form For MSB Licence - Eng - 22032013Shahrizan NoorNo ratings yet

- Petroleum Licence Application Form PDFDocument10 pagesPetroleum Licence Application Form PDFnicholas idungafaNo ratings yet

- NBR Tin Certificate 180261996183 PDFDocument1 pageNBR Tin Certificate 180261996183 PDFNewaz KabirNo ratings yet

- NBR Tin Certificate 312329690222Document1 pageNBR Tin Certificate 312329690222ashaduzzamanNo ratings yet

- Tax Code of BangladeshDocument5 pagesTax Code of Bangladeshsouravsam100% (2)

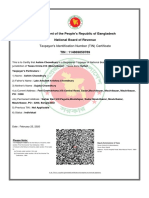

- Government of The People's Republic of Bangladesh National Board of RevenueDocument1 pageGovernment of The People's Republic of Bangladesh National Board of Revenuepddas13100% (1)

- Government of The People's Republic of Bangladesh National Board of RevenueDocument1 pageGovernment of The People's Republic of Bangladesh National Board of RevenueTasbi Ul Hasan Shaan100% (1)

- NBR Tin Certificate 114869859789 PDFDocument1 pageNBR Tin Certificate 114869859789 PDFDS PulakNo ratings yet

- Applicant - S Information Sheet (ActiveOne) PDFDocument4 pagesApplicant - S Information Sheet (ActiveOne) PDFmaris dinglasaNo ratings yet

- Whmcs Freenom Module Installation Howto Version110Document9 pagesWhmcs Freenom Module Installation Howto Version110Felix AdiNo ratings yet

- NBR Tin Certificate 591973763133Document1 pageNBR Tin Certificate 591973763133TinyPavelNo ratings yet

- NBR Tin Certificate 541484216851Document1 pageNBR Tin Certificate 541484216851Md. Jasim UddinNo ratings yet

- NBR Tin Certificate 842774824093 PDFDocument1 pageNBR Tin Certificate 842774824093 PDFMd. Saifullah MunirNo ratings yet

- NBR Tin Certificate 643541795237Document2 pagesNBR Tin Certificate 643541795237nihaldu0% (1)

- E TinDocument1 pageE TinJoynal KhanNo ratings yet

- BUSLIC Business Licence FormDocument10 pagesBUSLIC Business Licence Formcrew242No ratings yet

- Nit - 1 - 2 WCLDocument69 pagesNit - 1 - 2 WCLsaurabhbector100% (1)

- NBR Tin Certificate 676101345210 PDFDocument1 pageNBR Tin Certificate 676101345210 PDFAmrita SahaNo ratings yet

- Added Registration: The of National ofDocument1 pageAdded Registration: The of National ofMd. S H MarufNo ratings yet

- NBR Tin Certificate 535723564521Document1 pageNBR Tin Certificate 535723564521AN NURNo ratings yet

- EPOnlineSvcAccessApplnForm CompileDocument11 pagesEPOnlineSvcAccessApplnForm CompileRia ArguellesNo ratings yet

- Statement of Account: Date Transaction Type Amount NAV in INR (RS.) Price in INR (RS.) Number of Units Balance UnitDocument1 pageStatement of Account: Date Transaction Type Amount NAV in INR (RS.) Price in INR (RS.) Number of Units Balance Unitee206023No ratings yet

- Tutorial 6Document3 pagesTutorial 6Wan LinNo ratings yet

- Certificate of Creditable Tax Withheld at Source: (MM/DD/YYYY) (MM/DD/YYYY)Document52 pagesCertificate of Creditable Tax Withheld at Source: (MM/DD/YYYY) (MM/DD/YYYY)jeanieNo ratings yet

- GST STeps To File ReturnDocument22 pagesGST STeps To File ReturnAnnu KashyapNo ratings yet

- Go Green and Receive Your Income Tax Notices Electronically: WWW - Iras.gov - SG Mytax - Iras.gov - SGDocument2 pagesGo Green and Receive Your Income Tax Notices Electronically: WWW - Iras.gov - SG Mytax - Iras.gov - SGJinchi WeiNo ratings yet

- Form No. 16A: Certificate Under Section 203 of The Income-Tax Act, 1961 For Tax Deducted at SourceDocument2 pagesForm No. 16A: Certificate Under Section 203 of The Income-Tax Act, 1961 For Tax Deducted at SourceAnonymous glyBR9No ratings yet

- GNM-EXPORT LICENCE - Edit - 1626157788133Document1 pageGNM-EXPORT LICENCE - Edit - 1626157788133benard ayomahNo ratings yet

- GST User ManuelDocument195 pagesGST User Manuelsakthi raoNo ratings yet

- Vendor Creation FormDocument1 pageVendor Creation FormRahul RSNo ratings yet

- Iec Certificate NewDocument1 pageIec Certificate NewManish DaveNo ratings yet

- Print VAT Registration - GOV - UkDocument11 pagesPrint VAT Registration - GOV - Uksiva kumarNo ratings yet

- Kuwait TINDocument2 pagesKuwait TINAtif YadavNo ratings yet

- Cambridge English Vocab ListDocument42 pagesCambridge English Vocab ListseekusNo ratings yet

- Vocabulary List PDFDocument42 pagesVocabulary List PDFGatoneneNo ratings yet

- Vocabulary List PDFDocument42 pagesVocabulary List PDFGatoneneNo ratings yet

- Useful Phrases and Vocabulary For Writing Business LettersDocument4 pagesUseful Phrases and Vocabulary For Writing Business LettersRobert ScottNo ratings yet

- Vocabulary List PDFDocument42 pagesVocabulary List PDFGatoneneNo ratings yet

- Morsica - Marketing BasicsDocument28 pagesMorsica - Marketing BasicsseekusNo ratings yet

- QA Interview FAQDocument318 pagesQA Interview FAQPraveen Kumar GogulaNo ratings yet

- Short-Term Scheduling of Battery in A Grid-Connected PV-Battery SystemDocument9 pagesShort-Term Scheduling of Battery in A Grid-Connected PV-Battery SystemEric GalvánNo ratings yet

- History N Development ICEDocument5 pagesHistory N Development ICEAneesh KumarNo ratings yet

- GMC May 2019 June 2019: Title of Manual Title of SectionDocument16 pagesGMC May 2019 June 2019: Title of Manual Title of SectionRemz Prin Ting LaoagNo ratings yet

- Module 9 GCLP Good Documentation PracticeDocument11 pagesModule 9 GCLP Good Documentation PracticeKarishmaNo ratings yet

- FST-3112 Food Plant Layout and Sanitation Course OutlineDocument5 pagesFST-3112 Food Plant Layout and Sanitation Course OutlineSADIA ASLAMNo ratings yet

- Ad Js Injection - JsDocument2 pagesAd Js Injection - JsWalison SilvaNo ratings yet

- Using Boss Tone Studio For Me-25Document12 pagesUsing Boss Tone Studio For Me-25felipe herreraNo ratings yet

- Fire Protection Requirements For High Rise Building 15 M in Height or AboveDocument40 pagesFire Protection Requirements For High Rise Building 15 M in Height or AboveNishant Sharma100% (1)

- C# Interview Q - A BooDocument451 pagesC# Interview Q - A Boohrmohan86No ratings yet

- Outboard Model Code Reference ChartDocument2 pagesOutboard Model Code Reference Chartherbpatterson100% (1)

- Stainless Steel: Strong, Corrosion-ResistantDocument3 pagesStainless Steel: Strong, Corrosion-ResistantMahsaNo ratings yet

- Fireplan SymbolsDocument11 pagesFireplan SymbolsSeokhun KangNo ratings yet

- 00 LSPU Stage 2 Audit Report 2018 PDFDocument21 pages00 LSPU Stage 2 Audit Report 2018 PDFRolando Cruzada Jr.No ratings yet

- Solid Rocket Motor PropulsionDocument63 pagesSolid Rocket Motor Propulsionram narayanNo ratings yet

- New Microsoft Word DocumentDocument6 pagesNew Microsoft Word DocumentAnonymous EUNhdkrUNo ratings yet

- Yamaha Generalcatalog2005Document14 pagesYamaha Generalcatalog2005Vajda ZsoltNo ratings yet

- Subsea Pipeline StabilityDocument9 pagesSubsea Pipeline StabilityJhy MhaNo ratings yet

- Sub Queries - OracleDocument13 pagesSub Queries - OraclesxurdcNo ratings yet

- Timber Pole Cantilever Wall Worked Example 1Document9 pagesTimber Pole Cantilever Wall Worked Example 1Anonymous jbvNLNANLINo ratings yet

- Tuhin KanrarDocument2 pagesTuhin KanrarSmith JoannaNo ratings yet

- CW Radar2Document13 pagesCW Radar2sriram128No ratings yet

- MV Motor Publication Jan 2012Document16 pagesMV Motor Publication Jan 2012safinditNo ratings yet

- F 4400 Manual 02 16Document45 pagesF 4400 Manual 02 16Sodhi S SohalNo ratings yet

- CISCO CCNA Certifications - CCNA 3 - Module 2 PDFDocument6 pagesCISCO CCNA Certifications - CCNA 3 - Module 2 PDFAlina DraghiciNo ratings yet

- 4.4. High-Temperature ElectrolysisDocument3 pages4.4. High-Temperature ElectrolysisSaju ShajuNo ratings yet

- Welding FundamentalsDocument44 pagesWelding FundamentalsDhinasuga DhinakaranNo ratings yet

- Starbucks Business Case StudyDocument11 pagesStarbucks Business Case StudyJenzen TseNo ratings yet

- BMW SM CSDocument74 pagesBMW SM CSWei Xun Chin100% (4)

- CSA Direct Acting Valves 8.2017Document42 pagesCSA Direct Acting Valves 8.2017dalla nabilNo ratings yet