You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Page 4 BIR List of Top 20 Taxpayers Existing Non-Individual FP PDFDocument1 pagePage 4 BIR List of Top 20 Taxpayers Existing Non-Individual FP PDFPADAVELA DESIGNSNo ratings yet

- Page 8 BIR List of Top 20 Taxpayers Existing Non-Individual FPDocument1 pagePage 8 BIR List of Top 20 Taxpayers Existing Non-Individual FPPADAVELA DESIGNSNo ratings yet

- Page 8 BIR List of Top 20 Taxpayers Existing Non-Individual FPDocument1 pagePage 8 BIR List of Top 20 Taxpayers Existing Non-Individual FPPADAVELA DESIGNSNo ratings yet

- Page 7 BIR List of Top 20 Taxpayers Existing Non-Individual FPDocument1 pagePage 7 BIR List of Top 20 Taxpayers Existing Non-Individual FPPADAVELA DESIGNSNo ratings yet

- Pag-IBIG Fund Multi Purpose Loan Application SLF001 V03Document2 pagesPag-IBIG Fund Multi Purpose Loan Application SLF001 V03Jazz Adaza67% (3)

- Part 1 AccountingDocument3 pagesPart 1 AccountingAl-Hafeez Group of AcademiesNo ratings yet

- Oracle Financial TablesDocument9 pagesOracle Financial TablesShahzad945No ratings yet

- Effect of Cashless Payment Methods A Case Study Perspective AnalysisDocument4 pagesEffect of Cashless Payment Methods A Case Study Perspective AnalysisAaryan Singh100% (1)

- SKF Supply ChainDocument5 pagesSKF Supply ChainPrutha PatelNo ratings yet

- Nri Schedule of ChargesDocument4 pagesNri Schedule of ChargesRishiNo ratings yet

- Plastic Money: Presented By: Ramandeep Kaur & Mba 4 Sem. 90512234158Document30 pagesPlastic Money: Presented By: Ramandeep Kaur & Mba 4 Sem. 90512234158ramandeeprinkyNo ratings yet

- Special ExamDocument3 pagesSpecial ExamAdoree Ramos50% (2)

- Ae Teoa TGXWT de 42 XDocument3 pagesAe Teoa TGXWT de 42 Xbom diggaNo ratings yet

- J.K.Nayak: Logistics & SCMDocument10 pagesJ.K.Nayak: Logistics & SCMNitesh PanchNo ratings yet

- CPOLICYdoc 01050048194100210965 PDFDocument2 pagesCPOLICYdoc 01050048194100210965 PDFTanish MaanNo ratings yet

- Fee ReceiptDocument1 pageFee ReceiptAkashNo ratings yet

- JHi5sj8OaFqtsmjW8lRfm2Jj9pMkVK7iLNMmKoHy7gNC PDFDocument3 pagesJHi5sj8OaFqtsmjW8lRfm2Jj9pMkVK7iLNMmKoHy7gNC PDFSalman BoghaniNo ratings yet

- BOSCHDocument1 pageBOSCHKolkata Jyote MotorsNo ratings yet

- Aliu Dauda: Customer StatementDocument44 pagesAliu Dauda: Customer Statementaliudauda1982No ratings yet

- Shared Bus ProposalDocument6 pagesShared Bus ProposalErnest EsoNo ratings yet

- Air India LTC-80 Fare Wef 01 August 2017Document6 pagesAir India LTC-80 Fare Wef 01 August 2017Rajkumar MathurNo ratings yet

- VAT ExercisesDocument3 pagesVAT ExercisesMarie Tes LocsinNo ratings yet

- Important : Allama Iqbal Open University Islamabad Allama Iqbal Open University IslamabadDocument1 pageImportant : Allama Iqbal Open University Islamabad Allama Iqbal Open University IslamabadM Umar ChatthaNo ratings yet

- DTP1800793 HBL PDFDocument1 pageDTP1800793 HBL PDFvanii chuchuNo ratings yet

- Raju Bhai PDFDocument1 pageRaju Bhai PDFbsnlquotesNo ratings yet

- Transmittal 2019 PurokDocument2 pagesTransmittal 2019 Purokpulp23No ratings yet

- Pelzer Company Reconciled Its Bank and Book Statement Balances ofDocument2 pagesPelzer Company Reconciled Its Bank and Book Statement Balances ofAmit PandeyNo ratings yet

- Momo Statement ReportDocument9 pagesMomo Statement ReportPius AwuahNo ratings yet

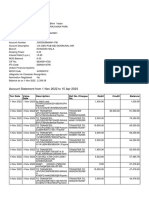

- Account Statement From 1 Nov 2022 To 15 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument15 pagesAccount Statement From 1 Nov 2022 To 15 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAyush yadavNo ratings yet

- DynDNS Invoice #12540511 LuduvicoDocument1 pageDynDNS Invoice #12540511 LuduvicoLuduvico ClaudioNo ratings yet

- Origin, History and Types of Banking SystemDocument44 pagesOrigin, History and Types of Banking Systemriajul islam jamiNo ratings yet

- Invoice BDocument1 pageInvoice BAzhar NurNo ratings yet

- 28D CTA 2D Pilipinas Kyohritsu Inc. v. CIR CTA Case No. 9557 January 28, 2020 PDFDocument33 pages28D CTA 2D Pilipinas Kyohritsu Inc. v. CIR CTA Case No. 9557 January 28, 2020 PDFLeulaDianneCantosNo ratings yet

- Source: 1. Sales JournalDocument3 pagesSource: 1. Sales JournalDonita SotolomboNo ratings yet

- Weekly Sales Report ExampleDocument2 pagesWeekly Sales Report ExampleIINNo ratings yet