You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Value Migration - MOSL - May 2018Document24 pagesValue Migration - MOSL - May 2018KCNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Ambit Strategy Update GoodClean 15 16nov2018Document36 pagesAmbit Strategy Update GoodClean 15 16nov2018tarun agrawalNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Ambit SmallCaps FindingMultibaggerswithinSmallcaps 02may2017Document16 pagesAmbit SmallCaps FindingMultibaggerswithinSmallcaps 02may2017tarun agrawalNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Ambit Healthcare Thematic Biosimilars Is It The Holy Grail 08feb2018Document12 pagesAmbit Healthcare Thematic Biosimilars Is It The Holy Grail 08feb2018tarun agrawalNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- India Road Sector: Lull To Recover inDocument45 pagesIndia Road Sector: Lull To Recover intarun agrawalNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- India Road Sector: Lull To Recover inDocument45 pagesIndia Road Sector: Lull To Recover intarun agrawalNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Media Detailed ReportDocument75 pagesMedia Detailed Reporttarun agrawalNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Avenue Supermarts GS 26-09-2017Document55 pagesAvenue Supermarts GS 26-09-2017tarun agrawalNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Impairment of AssetsDocument19 pagesImpairment of AssetsTareq SojolNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Hedging Strategies Using FuturesDocument31 pagesHedging Strategies Using Futuressanjana jainNo ratings yet

- Manappuram Kanaka Deepam (GOLD INVESTMENT SCHEME) - A Challenge To Gold ETFDocument2 pagesManappuram Kanaka Deepam (GOLD INVESTMENT SCHEME) - A Challenge To Gold ETFRaghu.GNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- ch-07 Dividend and DDTDocument57 pagesch-07 Dividend and DDTdean.socNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- CPALE CoverageDocument15 pagesCPALE CoverageMajariya Sahar SabladNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Company Module 1 SYBCOM Sem 4 - Corporate LawsDocument87 pagesCompany Module 1 SYBCOM Sem 4 - Corporate LawsHarsh GossainNo ratings yet

- Investment Banking Business ModelDocument35 pagesInvestment Banking Business ModelK RameshNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Finman 1-4 SummaryDocument8 pagesFinman 1-4 SummaryElieNo ratings yet

- Week 7 FABM 2Document9 pagesWeek 7 FABM 2WeighingSwing 35No ratings yet

- Financial Analysis VIP IndustriesDocument5 pagesFinancial Analysis VIP IndustriesAvinash KatochNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- PDF 20230412 193534 0000Document41 pagesPDF 20230412 193534 0000Razalo, Kimberly AnnNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

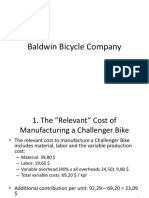

- Baldwin Bicycle Company EngDocument8 pagesBaldwin Bicycle Company EngChayan Kothari IDD,Biochem, IT-BHU, Varanasi (INDIA)No ratings yet

- Credit Risk Management LectureDocument80 pagesCredit Risk Management LectureAbhishek KarekarNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Nism Series V B - Mutual Fund Foundation ExamDocument29 pagesNism Series V B - Mutual Fund Foundation ExamRanganNo ratings yet

- Derivatives Security MarketDocument18 pagesDerivatives Security MarketYujinNo ratings yet

- 2 Crores in 4-5 Years in Unrealistic, But 140 Crores in 30-40 Years Is RealisticDocument2 pages2 Crores in 4-5 Years in Unrealistic, But 140 Crores in 30-40 Years Is RealisticAnonymous w6TIxI0G8lNo ratings yet

- CapbudgetingproblemsDocument3 pagesCapbudgetingproblemsVishal PaithankarNo ratings yet

- Midterm Exam Study GuideDocument7 pagesMidterm Exam Study GuideElena RuzoNo ratings yet

- 300 CubitsDocument2 pages300 CubitsTauseef AhmadNo ratings yet

- Pak Taufikur CH 11 Financial Management BrighamDocument69 pagesPak Taufikur CH 11 Financial Management BrighamRidhoVerianNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Adv Cost Assignment 2023Document6 pagesAdv Cost Assignment 2023GETAHUN ASSEFA ALEMUNo ratings yet

- Rosewood Hotels Resorts CLTV Sensitivity Analysis GRP 4Document24 pagesRosewood Hotels Resorts CLTV Sensitivity Analysis GRP 4t3ddyme123No ratings yet

- PERE - Private Equity Real EstateDocument1 pagePERE - Private Equity Real EstatePereNo ratings yet

- Ratio Analysis of "Square Textiles Limited"Document3 pagesRatio Analysis of "Square Textiles Limited"Bijoy SalahuddinNo ratings yet

- CPALE Review TrackerDocument19 pagesCPALE Review TrackerMica TolentinoNo ratings yet

- Harvard Case Study - Flash Inc - AllDocument40 pagesHarvard Case Study - Flash Inc - All竹本口木子100% (1)

- Answer: Using A Financial Calculator or Excel The YTM Is Determined To Be 10.68%Document3 pagesAnswer: Using A Financial Calculator or Excel The YTM Is Determined To Be 10.68%rifat AlamNo ratings yet

- Calmar Ratio of FundDocument2 pagesCalmar Ratio of FundBiljo JohnyNo ratings yet

- Unit 1 Vouching - 1 - FinalDocument12 pagesUnit 1 Vouching - 1 - Finalshoaib shaikhNo ratings yet

- Seatwork: Set BDocument4 pagesSeatwork: Set BRochelle Joyce CosmeNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)