You might also like

- Rockboro Machine Tools Corporation Case QuestionsDocument1 pageRockboro Machine Tools Corporation Case QuestionsMasumiNo ratings yet

- 551 KohlerDocument3 pages551 KohlerwesiytgiuweNo ratings yet

- JC Penney CaseDocument8 pagesJC Penney CaseSebastian MansillaNo ratings yet

- Harbor Co Negotiation CaseDocument2 pagesHarbor Co Negotiation Casesatherbd2133% (3)

- Investor Diary Expert Stock Analysis Excel (V-3) : How To Use This Spreadsheet?Document75 pagesInvestor Diary Expert Stock Analysis Excel (V-3) : How To Use This Spreadsheet?raghawindor0% (4)

- Krispy Donut Case AnalysisDocument7 pagesKrispy Donut Case Analysisfaraz_soleymani100% (1)

- Debt Policy at Ust Case SolutionDocument2 pagesDebt Policy at Ust Case Solutiontamur_ahan50% (2)

- GR-II-Team 11-2018Document4 pagesGR-II-Team 11-2018Gautam PatilNo ratings yet

- Fundamental Accounting Principles Volume 2 Canadian 15th Edition Larson Solutions ManualDocument10 pagesFundamental Accounting Principles Volume 2 Canadian 15th Edition Larson Solutions ManualDonald Cacioppo100% (38)

- Rocheholdingag 160318174415Document24 pagesRocheholdingag 160318174415iskandarbasiruddinNo ratings yet

- Case 5 Midland Energy Case ProjectDocument7 pagesCase 5 Midland Energy Case ProjectCourse HeroNo ratings yet

- AC Sample Paper 3 Unsolved-1Document10 pagesAC Sample Paper 3 Unsolved-1Appharnha Rs0% (1)

- Midland Energy Resources FinalDocument5 pagesMidland Energy Resources FinalpradeepNo ratings yet

- Midland CaseDocument8 pagesMidland CaseDevansh RaiNo ratings yet

- BBBY Case ExerciseDocument7 pagesBBBY Case ExerciseSue McGinnisNo ratings yet

- Ameritrade Case PDFDocument6 pagesAmeritrade Case PDFAnish Anish100% (1)

- Kohler CompanyDocument3 pagesKohler CompanyDuncan BakerNo ratings yet

- LoewenDocument3 pagesLoewenAmit SurveNo ratings yet

- Sure CutDocument1 pageSure Cutchch917No ratings yet

- Harvard Case: Sterling Household CompanyDocument10 pagesHarvard Case: Sterling Household Companymadeleine ReaNo ratings yet

- Innocents Abroad: Currencies and International Stock ReturnsDocument24 pagesInnocents Abroad: Currencies and International Stock ReturnsGragnor PrideNo ratings yet

- Assessing Earnings Quality at NuwareDocument7 pagesAssessing Earnings Quality at Nuwaremyhellonearth0% (1)

- NuWare 1 PagerDocument1 pageNuWare 1 Pagervelusn100% (1)

- Ameritrade Case SolutionDocument31 pagesAmeritrade Case Solutionsanz0840% (5)

- Write UpDocument3 pagesWrite UpDoritosxuNo ratings yet

- Nu WareDocument22 pagesNu WaresslbsNo ratings yet

- Ameritrade Case ConsolidatedDocument5 pagesAmeritrade Case Consolidatedyvasisht3100% (1)

- AQR CaseDocument3 pagesAQR CaseIni EjideleNo ratings yet

- Mergers & AcquisitionsDocument2 pagesMergers & AcquisitionsRashleen AroraNo ratings yet

- Buckeye Bank CaseDocument7 pagesBuckeye Bank CasePulkit Mathur0% (2)

- WrigleyDocument14 pagesWrigleysotki4100% (1)

- Adecco QuestionsDocument1 pageAdecco Questionsptan123No ratings yet

- Soapbox Whirlpool VFINALDocument15 pagesSoapbox Whirlpool VFINALAnonymous Ecd8rCNo ratings yet

- 3.2. Finance 1 Quiz On Horizontal VerticalDocument3 pages3.2. Finance 1 Quiz On Horizontal VerticalZham JavierNo ratings yet

- Midland Energy Resources Case Study: FINS3625-Applied Corporate FinanceDocument11 pagesMidland Energy Resources Case Study: FINS3625-Applied Corporate FinanceCourse Hero100% (1)

- HBS Ameritrade Corporate Finance Case Study SolutionDocument6 pagesHBS Ameritrade Corporate Finance Case Study SolutionEugene Nikolaychuk100% (5)

- MidlandDocument4 pagesMidlandsophieNo ratings yet

- WrigleyDocument28 pagesWrigleyKaran Rana100% (1)

- FRAV Individual Assignment - Pranjali Silimkar - 2016PGP278Document12 pagesFRAV Individual Assignment - Pranjali Silimkar - 2016PGP278pranjaligNo ratings yet

- AmeriTrade Case StudyDocument3 pagesAmeriTrade Case StudyTracy PhanNo ratings yet

- Case Study - Linear Tech - Christopher Taylor - SampleDocument9 pagesCase Study - Linear Tech - Christopher Taylor - Sampleakshay87kumar8193No ratings yet

- Case Discussion PointsDocument3 pagesCase Discussion PointsMeena100% (1)

- M&a Assignment - Syndicate C FINALDocument8 pagesM&a Assignment - Syndicate C FINALNikhil ReddyNo ratings yet

- Case 5Document15 pagesCase 5Qiao LengNo ratings yet

- Ethodology AND Ssumptions: B B × D EDocument7 pagesEthodology AND Ssumptions: B B × D ECami MorenoNo ratings yet

- Assignment ON Case Analysis of Harnischfeger Corporation: Submitted To Submitted by Dr. Shikha Bhatia Shreya PGFB1144Document3 pagesAssignment ON Case Analysis of Harnischfeger Corporation: Submitted To Submitted by Dr. Shikha Bhatia Shreya PGFB1144simplyshreya99No ratings yet

- CasoDocument20 pagesCasoasmaNo ratings yet

- UST IncDocument16 pagesUST IncNur 'AtiqahNo ratings yet

- LinearDocument6 pagesLinearjackedup211No ratings yet

- Landmark Facility Solutions - QuestionsDocument1 pageLandmark Facility Solutions - QuestionsFaig0% (1)

- Landmark SolutionsDocument4 pagesLandmark SolutionsmansNo ratings yet

- Jetblue Airways Ipo ValuationDocument6 pagesJetblue Airways Ipo ValuationXing Liang HuangNo ratings yet

- Midland FinalDocument8 pagesMidland Finalkasboo6No ratings yet

- Marriott Solutions WACC LodgingDocument3 pagesMarriott Solutions WACC LodgingPabloCaicedoArellanoNo ratings yet

- Carter LBODocument1 pageCarter LBOEddie KruleNo ratings yet

- Pro Forma ActivityDocument3 pagesPro Forma ActivityPring PringNo ratings yet

- Reporting and Analyzing Revenues and Receivables: Learning Objectives - Coverage by QuestionDocument34 pagesReporting and Analyzing Revenues and Receivables: Learning Objectives - Coverage by QuestionpoollookNo ratings yet

- Afm CS2 Pes1202202920 PDFDocument2 pagesAfm CS2 Pes1202202920 PDFmohammed yaseenNo ratings yet

- Dmp3e Ch06 Solutions 01.26.10 FinalDocument39 pagesDmp3e Ch06 Solutions 01.26.10 Finalmichaelkwok1No ratings yet

- Finacc PolymediaDocument5 pagesFinacc PolymediaFrancisco MarvinNo ratings yet

- APLK - Earnings Quality - Arsyan AdimasDocument6 pagesAPLK - Earnings Quality - Arsyan AdimasAdimas Hanindika100% (1)

- P7int 2013 Jun A PDFDocument17 pagesP7int 2013 Jun A PDFhiruspoonNo ratings yet

- Window DressingDocument3 pagesWindow Dressingkriti_a100% (2)

- Importance of Financial StatementsDocument10 pagesImportance of Financial StatementsAmrit TejaniNo ratings yet

- Capital BudgetingDocument45 pagesCapital BudgetingLumumba KuyelaNo ratings yet

- Pricing The IPODocument14 pagesPricing The IPOsatherbd2133% (3)

- Midland Energy Resources (Final)Document4 pagesMidland Energy Resources (Final)satherbd21100% (3)

- Coke Case MemoDocument5 pagesCoke Case Memosatherbd21No ratings yet

- Pert 1 & 2 - Derivative-CompleteDocument42 pagesPert 1 & 2 - Derivative-CompletekristjuNo ratings yet

- Project Report: M/S Siva Sai Seeds Prop: Mrs. MAMATHA, W/O Sri ChandrasekharDocument41 pagesProject Report: M/S Siva Sai Seeds Prop: Mrs. MAMATHA, W/O Sri ChandrasekharRamakrishna NaiduNo ratings yet

- BUD 2242 Budgeting Small SchoolsDocument73 pagesBUD 2242 Budgeting Small SchoolsMaria Faye MarianoNo ratings yet

- DocumentDocument2 pagesDocumentVikas ENo ratings yet

- Commerce Accounts QuestionsDocument18 pagesCommerce Accounts QuestionsNirmal K PradhanNo ratings yet

- Lab Task 1-Ms WordDocument3 pagesLab Task 1-Ms WordSiti Sarah0% (1)

- Keown8 ch17Document30 pagesKeown8 ch17samir249No ratings yet

- As10-Ca CS Hub PDFDocument6 pagesAs10-Ca CS Hub PDFULTIMATE FACTS HINDINo ratings yet

- Basic Accounting Concept The Income StatementDocument66 pagesBasic Accounting Concept The Income StatementSatish Ranjan PradhanNo ratings yet

- Audit of Books of AccountsDocument14 pagesAudit of Books of Accountsdeepti sharmaNo ratings yet

- Financial Analysis - Ayala LandDocument23 pagesFinancial Analysis - Ayala LandMr. CopernicusNo ratings yet

- Cover Page - Shares Shares in Thousands Entity Information (Line Items)Document101 pagesCover Page - Shares Shares in Thousands Entity Information (Line Items)leeeeNo ratings yet

- Managerial-Finance-Project Orascom Report FinalDocument63 pagesManagerial-Finance-Project Orascom Report FinalAmira OkashaNo ratings yet

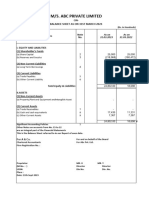

- PVT LTD Comp Balance-Sheet - FY - 22-23Document4 pagesPVT LTD Comp Balance-Sheet - FY - 22-23yogeshbhagat451No ratings yet

- CH 08Document91 pagesCH 08dsfsdfNo ratings yet

- Financial PerformanceDocument6 pagesFinancial PerformanceRammee AnuwerNo ratings yet

- Finance For ProcurementDocument3 pagesFinance For ProcurementAlex MuhweziNo ratings yet

- Financial Report of Shivam Cement by SampurnaDocument24 pagesFinancial Report of Shivam Cement by SampurnaSampurna PoudelNo ratings yet

- AE 191 M-TEST 2 With AnswersDocument7 pagesAE 191 M-TEST 2 With AnswersVenus PalmencoNo ratings yet

- Riginal Ronouncements: Statement of Financial Accounting Standards No. 141Document73 pagesRiginal Ronouncements: Statement of Financial Accounting Standards No. 141ctaggart878No ratings yet

- IAE C117 06000 EN - EuroplastDocument9 pagesIAE C117 06000 EN - EuroplastAlan DonosoNo ratings yet

- Chapter 03 - AnswerDocument10 pagesChapter 03 - AnswerGeomari D. BigalbalNo ratings yet

- Financial Analysis of Tata Steel and Jindal Steel and Power Ltd.Document34 pagesFinancial Analysis of Tata Steel and Jindal Steel and Power Ltd.O.p. SharmaNo ratings yet

- CF Final Report Group 7 MWG - CompressDocument22 pagesCF Final Report Group 7 MWG - CompressThư NguyễnNo ratings yet

- MS7SL800 - Assignment - 1 - Reckitt Benciser GroupDocument15 pagesMS7SL800 - Assignment - 1 - Reckitt Benciser GroupDaniel AjanthanNo ratings yet

- Cost Terminology and Cost Behaviors: Learning ObjectivesDocument17 pagesCost Terminology and Cost Behaviors: Learning ObjectivesRichard John EcalneNo ratings yet