You might also like

- Presentation in Linear ProgrammingDocument34 pagesPresentation in Linear Programmingotok jacildoNo ratings yet

- Example 1 - Over and Under Provision of Current TaxDocument14 pagesExample 1 - Over and Under Provision of Current TaxPui YanNo ratings yet

- Capital Budgeting Lesson NewDocument44 pagesCapital Budgeting Lesson NewLea MachadoNo ratings yet

- Types of LeasesDocument4 pagesTypes of LeasesPui YanNo ratings yet

- Activity - Capital Investment AnalysisDocument5 pagesActivity - Capital Investment AnalysisKATHRYN CLAUDETTE RESENTENo ratings yet

- Construction Accounting and Financial ManagementDocument25 pagesConstruction Accounting and Financial ManagementWajdiNo ratings yet

- Quality - MCK Core BeliefsDocument13 pagesQuality - MCK Core Beliefsramcbey100% (2)

- Business Law - Chapter 1 PDFDocument3 pagesBusiness Law - Chapter 1 PDFJOBY LACC88100% (1)

- Client's Acceptance and Continuance FormDocument9 pagesClient's Acceptance and Continuance FormJeane Mae BooNo ratings yet

- Credit Monitoring.1997 2003Document24 pagesCredit Monitoring.1997 2003MdramjanaliNo ratings yet

- GG ToysDocument3 pagesGG ToysSomu Das79% (14)

- Capital BudgetingDocument71 pagesCapital BudgetingJun Guerzon PaneloNo ratings yet

- Short Term Decision Making 2Document8 pagesShort Term Decision Making 2Pui YanNo ratings yet

- CASEDocument18 pagesCASEJay SabioNo ratings yet

- FINMNN1 Chapter 4 Short Term Financial PlanningDocument16 pagesFINMNN1 Chapter 4 Short Term Financial Planningkissmoon732No ratings yet

- MODULE 8 Capital BudgetingDocument9 pagesMODULE 8 Capital BudgetingLumingNo ratings yet

- Introduction To Credit ManagementDocument48 pagesIntroduction To Credit ManagementHakdog KaNo ratings yet

- Project Report On Non-Woven BagsDocument13 pagesProject Report On Non-Woven Bagsashokadupa100% (2)

- Estate Under Administration-Tax2Document15 pagesEstate Under Administration-Tax2onet88No ratings yet

- Cash Budget Format and Its Explanation With Solved ExampleDocument8 pagesCash Budget Format and Its Explanation With Solved ExamplePui YanNo ratings yet

- AAUI - General Overview IFRS 17Document117 pagesAAUI - General Overview IFRS 17Tyan Retsa PutriNo ratings yet

- Payback Period Method For Capital Budgeting DecisionsDocument5 pagesPayback Period Method For Capital Budgeting DecisionsAmit Kainth100% (1)

- Capital Budgeting Report FinalDocument15 pagesCapital Budgeting Report FinalCezar SabladNo ratings yet

- 1 SamsungDocument32 pages1 SamsungNishant PareNo ratings yet

- Forecasting: Questions and Answers Q6.1 Q6.1 AnswerDocument28 pagesForecasting: Questions and Answers Q6.1 Q6.1 AnswerjyottsnaNo ratings yet

- Sajid. PEPSICODocument61 pagesSajid. PEPSICOSajid HussainNo ratings yet

- Ignorantia Juris Non ExcusatDocument3 pagesIgnorantia Juris Non ExcusatXymon Bassig0% (1)

- Tax EvasionDocument5 pagesTax Evasiongfreak0100% (1)

- 1.6 Organisational Structure For ZPC Kariba South Power Station.......... 9Document27 pages1.6 Organisational Structure For ZPC Kariba South Power Station.......... 9Praise chari100% (1)

- Baf2104 Financial Management CatDocument4 pagesBaf2104 Financial Management Catcyrus100% (1)

- Pecking Order TheoryDocument4 pagesPecking Order TheoryThunder CatNo ratings yet

- Problems Solved Pay Back PeriodDocument7 pagesProblems Solved Pay Back PeriodAfthab MuhammedNo ratings yet

- New Trends in Financing Working Capital by BanksDocument9 pagesNew Trends in Financing Working Capital by BanksAparna Karuvallil100% (1)

- Purchase Consideration NumericalsDocument8 pagesPurchase Consideration NumericalsIsfh 67No ratings yet

- B220 MI02 Circular FlowDocument5 pagesB220 MI02 Circular FloweerashahNo ratings yet

- Share CapitalDocument4 pagesShare CapitalSobanNo ratings yet

- 4 Time Value of MoneyDocument15 pages4 Time Value of MoneyOmar Faruk 2235292660No ratings yet

- Panasonic, Sony and Hitachi Are Some Companies That Follow Ethnocentric ApproachDocument3 pagesPanasonic, Sony and Hitachi Are Some Companies That Follow Ethnocentric ApproachMohit3107No ratings yet

- Chapter 06Document5 pagesChapter 06Md. Saidul IslamNo ratings yet

- Project Appraisal-1 PDFDocument23 pagesProject Appraisal-1 PDFFareha RiazNo ratings yet

- Project Appraisal 1Document23 pagesProject Appraisal 1Fareha RiazNo ratings yet

- Tutorial 2 - Principles of Capital BudgetingDocument3 pagesTutorial 2 - Principles of Capital Budgetingbrahim.safa2018No ratings yet

- 2-4 2004 Jun QDocument11 pages2-4 2004 Jun QAjay TakiarNo ratings yet

- AE24 Lesson 6: Analysis of Capital Investment DecisionsDocument17 pagesAE24 Lesson 6: Analysis of Capital Investment DecisionsMajoy BantocNo ratings yet

- Seminar 06 enDocument1 pageSeminar 06 enTausif AhmedNo ratings yet

- Capital BudgetingDocument18 pagesCapital BudgetingYash ChaurasiaNo ratings yet

- Capital Budgeting Using A Linear Programming ModelDocument16 pagesCapital Budgeting Using A Linear Programming ModelLucas Matheus Da Silva RibeiroNo ratings yet

- 254 Chapter 10Document23 pages254 Chapter 10Zidan ZaifNo ratings yet

- 5, 6 & 7 Capital BudgetingDocument42 pages5, 6 & 7 Capital BudgetingNaman AgarwalNo ratings yet

- CH 08Document12 pagesCH 08AlJabir KpNo ratings yet

- Capital Budgeting - Adv IssuesDocument21 pagesCapital Budgeting - Adv IssuesdixitBhavak DixitNo ratings yet

- Project Appraisal and Selection: Time Preference For MoneyDocument16 pagesProject Appraisal and Selection: Time Preference For MoneynathnaelNo ratings yet

- FM 3Document12 pagesFM 3Rohini rs nairNo ratings yet

- Capital Budgeting Practice Set 2015Document2 pagesCapital Budgeting Practice Set 2015Arushi AggarwalNo ratings yet

- Vanraj Smart Task 2Document4 pagesVanraj Smart Task 2Vanraj MakwanaNo ratings yet

- Capital BudgetingDocument24 pagesCapital BudgetingHassaan NasirNo ratings yet

- Topic 3 FINANCIAL MANAGEMENT - INVESTMENT DECISION, LIRA UNIVERSITYDocument33 pagesTopic 3 FINANCIAL MANAGEMENT - INVESTMENT DECISION, LIRA UNIVERSITYPule JackobNo ratings yet

- Question f8 Audit RiskDocument4 pagesQuestion f8 Audit RiskTashfeenNo ratings yet

- 4852 - CID - Sessions 1-2-3Document25 pages4852 - CID - Sessions 1-2-3Sidharth RayNo ratings yet

- Investment Appraisal 1Document13 pagesInvestment Appraisal 1Arslan ArifNo ratings yet

- CA 51014 - Strategic Cost Management Capital BudgetingDocument9 pagesCA 51014 - Strategic Cost Management Capital BudgetingMark FloresNo ratings yet

- 1 Project AppraisalDocument53 pages1 Project AppraisalZara FaryalNo ratings yet

- Investment Appraisal Report (Individual Report)Document10 pagesInvestment Appraisal Report (Individual Report)Eric AwinoNo ratings yet

- Capital BudgetingDocument47 pagesCapital BudgetingShaheer AliNo ratings yet

- CH 2 Capital Budgeting FinalDocument21 pagesCH 2 Capital Budgeting FinalSureshArigelaNo ratings yet

- Chapter 5Document20 pagesChapter 5Gunda AvinashNo ratings yet

- Module 6 CanvasDocument9 pagesModule 6 CanvasMon RamNo ratings yet

- Advanced Financial Management: Tuesday 3 June 2014Document13 pagesAdvanced Financial Management: Tuesday 3 June 2014SajidZiaNo ratings yet

- Finance Midterm QuestionsDocument3 pagesFinance Midterm QuestionsAnonymous x4LL5ecNCRNo ratings yet

- 05 Exercises On Capital BudgetingDocument4 pages05 Exercises On Capital BudgetingAnshuman AggarwalNo ratings yet

- MN20501 Lecture 9 Review ExerciseDocument3 pagesMN20501 Lecture 9 Review Exercisesamvrab1919No ratings yet

- China Dolls - IcsDocument4 pagesChina Dolls - IcsPui YanNo ratings yet

- AccaDocument5 pagesAccaPui YanNo ratings yet

- Ics Case 6Document24 pagesIcs Case 6Pui YanNo ratings yet

- Management Accounting II: Assignment PresentationDocument6 pagesManagement Accounting II: Assignment PresentationPui YanNo ratings yet

- Isc - Case 2 Androids Under Attack PresentationDocument7 pagesIsc - Case 2 Androids Under Attack PresentationPui Yan100% (1)

- China Dolls - IcsDocument4 pagesChina Dolls - IcsPui YanNo ratings yet

- Explain Apple's Success Over The Last Decade. Think About Which Industries It Has Disrupted and How. Also Look at Apple's Main CompetitorsDocument5 pagesExplain Apple's Success Over The Last Decade. Think About Which Industries It Has Disrupted and How. Also Look at Apple's Main CompetitorsPui YanNo ratings yet

- Introduction of Toshiba CorporationDocument24 pagesIntroduction of Toshiba CorporationPui YanNo ratings yet

- VRIO Analysis ofDocument3 pagesVRIO Analysis ofPui YanNo ratings yet

- Ics A Delima - PresentationDocument9 pagesIcs A Delima - PresentationPui YanNo ratings yet

- Ics Part ADocument6 pagesIcs Part APui YanNo ratings yet

- Weak Tone Set by The Top ManagementDocument2 pagesWeak Tone Set by The Top ManagementPui YanNo ratings yet

- British American Tobacco PDFDocument121 pagesBritish American Tobacco PDFPui YanNo ratings yet

- 7 StandardCostingPractices PDFDocument8 pages7 StandardCostingPractices PDFPui YanNo ratings yet

- 7.0 Other Countries Experiences in Accrual AccountingDocument14 pages7.0 Other Countries Experiences in Accrual AccountingPui YanNo ratings yet

- The Balanced Scorecard Uses Financial Performance MeasuresDocument17 pagesThe Balanced Scorecard Uses Financial Performance MeasuresPui YanNo ratings yet

- Bac 3110 - Accounting Information System 2 Z: Name: Phoon Pui Yan Matric Number: QIUP-201604-000791Document16 pagesBac 3110 - Accounting Information System 2 Z: Name: Phoon Pui Yan Matric Number: QIUP-201604-000791Pui YanNo ratings yet

- 7.0 Other Countries Experiences in Accrual AccountingDocument4 pages7.0 Other Countries Experiences in Accrual AccountingPui YanNo ratings yet

- MA PresentationDocument4 pagesMA PresentationPui YanNo ratings yet

- In Tsy M 2015 Alba Ttat 20151Document11 pagesIn Tsy M 2015 Alba Ttat 20151Pui YanNo ratings yet

- Practice Problem: Chapter 16, Just-in-Time Systems Problem 1Document3 pagesPractice Problem: Chapter 16, Just-in-Time Systems Problem 1mtry658893No ratings yet

- Evolution of Management AccountingDocument20 pagesEvolution of Management AccountingPui YanNo ratings yet

- VRIO Analysis of Vintage CoffeeDocument3 pagesVRIO Analysis of Vintage CoffeePui YanNo ratings yet

- Bac3201 Taxation 3Document12 pagesBac3201 Taxation 3Pui YanNo ratings yet

- Tour of Vehicle Workshop To Identify Potential RisksDocument1 pageTour of Vehicle Workshop To Identify Potential RisksPui YanNo ratings yet

- Process Costing-WIPDocument3 pagesProcess Costing-WIPSigei LeonardNo ratings yet

- RmycDocument7 pagesRmyclalala010899No ratings yet

- Managers: Managerial Accounting ForDocument28 pagesManagers: Managerial Accounting ForRiazboniNo ratings yet

- T456633691Document2 pagesT456633691निपुण कुमारNo ratings yet

- AP.3408 Audit of EquityDocument4 pagesAP.3408 Audit of EquityMonica GarciaNo ratings yet

- 3-8 Doc1Document66 pages3-8 Doc1Ayalew TayeNo ratings yet

- Deloitte Au Fs Cultivating Risk Intelligent Culture 1012Document12 pagesDeloitte Au Fs Cultivating Risk Intelligent Culture 1012nomsanyandowe371No ratings yet

- EFSA Guidelines On Outsourcing Requirements For Supervised EntitiesDocument17 pagesEFSA Guidelines On Outsourcing Requirements For Supervised EntitiesarvoboxNo ratings yet

- A Project Report ON: Working Capital Management at VodafoneDocument12 pagesA Project Report ON: Working Capital Management at VodafonebhagathnagarNo ratings yet

- Jet Airways Audit Report PDFDocument12 pagesJet Airways Audit Report PDFsatish100% (1)

- Introduction To Internal Control SystemDocument35 pagesIntroduction To Internal Control SystemStoryKingNo ratings yet

- 15) Pear International - Controls and TOC QuestionDocument2 pages15) Pear International - Controls and TOC QuestionkasimranjhaNo ratings yet

- Topic 1 - Overview: Licensing Exam Paper 1 Topic 1Document18 pagesTopic 1 - Overview: Licensing Exam Paper 1 Topic 1anonlukeNo ratings yet

- ADB Annual Report 1998Document305 pagesADB Annual Report 1998Asian Development BankNo ratings yet

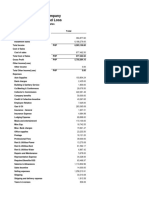

- XYZ Company Profit and Loss: All DatesDocument2 pagesXYZ Company Profit and Loss: All DatesMatt Kelvin ParaisoNo ratings yet

- COA Rules of ProcedureDocument20 pagesCOA Rules of ProcedureGerald MesinaNo ratings yet

- 04 BLGUMabuslo 2022 AAR Independent Auditor's ReportDocument3 pages04 BLGUMabuslo 2022 AAR Independent Auditor's ReportGilbert D. AfallaNo ratings yet

- Applied Auditing Chapter08 - AnswerDocument27 pagesApplied Auditing Chapter08 - AnswerGraceNo ratings yet

- Nagaland University Act, 1989Document34 pagesNagaland University Act, 1989Latest Laws TeamNo ratings yet

- The Three Key Elements of Professional Skepticism PDFDocument6 pagesThe Three Key Elements of Professional Skepticism PDFSahar FayyazNo ratings yet

- Petty Cash BookDocument6 pagesPetty Cash BookBuhle BenkosiNo ratings yet

- PROJECT REPORT Prepared By: : Executive SummaryDocument18 pagesPROJECT REPORT Prepared By: : Executive SummaryGiYan SalvadorNo ratings yet

- Las Vegas Convention Center Expansion Proposal To SNTIC From April 28th 2016Document155 pagesLas Vegas Convention Center Expansion Proposal To SNTIC From April 28th 2016Zennie AbrahamNo ratings yet